Integrating workers' comp into an HR outsourcing arrangement changes this equation. Instead of managing coverage, claims, and compliance in silos, everything flows through one provider relationship.

This guide covers how that integration works mechanically, the financial and operational benefits, what responsibilities remain with the employer, and how to evaluate the right outsourcing partner.

One important clarification upfront: the Professional Employer Organization (PEO) model is the arrangement that most commonly includes workers' comp as part of a bundled HR package. Not all HR outsourcing providers offer the same depth of support. That distinction matters — and it shapes the entire evaluation process.

Key Takeaways

- PEOs use master workers' comp policies to pool risk across clients, often delivering $66 in annual savings per employee on workers' comp alone

- Pay-as-you-go billing ties premiums to actual payroll, eliminating surprise audit bills

- OSHA violations can cost up to $16,550 per serious violation — PEO compliance support directly reduces this exposure

- Construction, manufacturing, and senior living see the greatest workers' comp cost benefits through PEO group purchasing power

- Employers retain responsibility for physical workplace safety; PEOs handle the administration, not the safety culture itself

What Workers' Comp Integration with HR Outsourcing Actually Means

Rather than purchasing a standalone policy directly from an insurer, a business outsources workers' comp administration to an HR outsourcing provider — typically a PEO — which manages coverage, claims, and compliance as part of a bundled HR relationship.

The key is understanding the difference between two common HR outsourcing models:

| Model | Workers' Comp Structure | Employer Retains Own Policy? |

|---|---|---|

| PEO (Co-Employment) | Employees placed under PEO's master workers' comp policy | No — covered under PEO's policy |

| ASO / À la Carte HR Outsourcer | Claims management assistance only | Yes — employer carries its own policy |

Under co-employment, the PEO becomes a shared employer of record. That co-employment structure is what makes integrated workers' comp possible — the PEO can cover your employees under its own master policy, rather than requiring you to manage a separate one.

In practice, "integration" means everything flows through one provider:

- Workers' comp premiums tied directly to payroll data

- Claims handled without separate insurer coordination

- Payroll classifications and OSHA recordkeeping managed in one system

- No back-and-forth between your broker, insurer, and HR platform

How PEOs Manage Workers' Compensation: The Mechanics

The Master Policy and Cost Savings

Under co-employment, a PEO places client employees on its own master workers' comp policy. This pools risk across the PEO's entire client base — which is substantial. According to NAPEO, the PEO industry supports over 4.5 million jobs across 230,000+ clients and generates $414 billion in annual revenue. That scale gives PEOs real purchasing leverage.

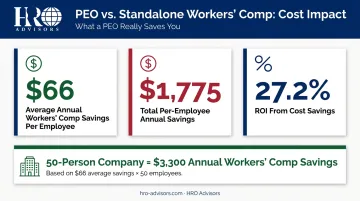

The financial impact is documented. A NAPEO/McBassi ROI study found $66 in average annual workers' comp savings per employee when using a PEO, contributing to a total of $1,775 in annual per-employee savings and a 27.2% ROI from cost savings alone. For a 50-person company, that's $3,300 in workers' comp savings annually — with no policy administration required on your end.

Pay-As-You-Go Billing

Traditional workers' comp policies estimate your payroll at the start of the year and charge premiums based on that estimate. At year-end, an audit compares estimated versus actual payroll — and if your workforce grew, you owe the difference. The California Department of Insurance notes that refusing to cooperate with a premium audit can result in a premium equal to three times the estimated policy premium.

PEOs solve this with pay-as-you-go billing: premiums are calculated based on actual payroll each pay period. There's no upfront deposit, no year-end true-up, and cash flow stays predictable throughout the year.

Experience Modification Rate (EMR) Implications

Your experience modification rate (EMR or "mod") reflects your claims history relative to others in your industry. NCCI, which manages experience rating in most states, uses three years of payroll and loss data to calculate the mod — and it directly affects your premium, up or down.

Under co-employment, your claims history may be tied to the PEO's master mod rather than your individual history. This can be advantageous if your own claims history is poor, but it works the other way if the PEO's portfolio has worse experience than your business. Ask any prospective PEO specifically how their experience rating is structured and how client claims affect that calculation.

Claims Management and OSHA Recordkeeping

How a PEO handles claims directly shapes your EMR over time. When an injury occurs, a PEO's dedicated team manages the full process — steps that typically fall through the cracks at small businesses without dedicated HR:

- Files the first report of injury with the insurer

- Liaises with the claims adjuster throughout the process

- Monitors medical treatment timelines to avoid unnecessary delays

- Coordinates return-to-work programs to reduce lost-time costs

On the compliance side, PEOs typically manage OSHA 300/A log maintenance, incident reporting, and safety program documentation. This matters financially. OSHA's current maximum penalties reach $16,550 per serious, other-than-serious, or posting violation, and $165,514 per willful or repeated violation. A single missed recordkeeping obligation can trigger a citation.

Key Benefits of Integrating Workers' Comp Through HR Outsourcing

Lower Rates Through Group Purchasing Power

Smaller businesses can't negotiate workers' comp rates the way a Fortune 500 company can. A PEO can — because it brings its entire client portfolio to the table. The $66 per-employee annual savings figure from NAPEO's research reflects real pricing power that individual SMBs simply don't have access to on their own.

For businesses in higher-risk industries, the gap is even more pronounced. New York's 2025 loss cost benchmarks illustrate the stakes: concrete construction carries a loss cost of $19.40 per $100 of payroll, while skilled nursing facilities sit at $2.88. Access to group rates in these classifications can translate to real premium reductions.

Elimination of Audit Surprises

Traditional workers' comp policies audit annually. If your payroll grew — you hired people, added overtime, brought on seasonal workers — you receive a bill for the difference. Pay-as-you-go billing under a PEO eliminates this by aligning premiums to real payroll data in real time.

Reduced Administrative Burden

One-third of companies spend at least 11 hours per week on HR administration according to U.S. Chamber of Commerce data. Workers' comp is a meaningful slice of that: policy management, certificate of insurance requests, renewal negotiations, injury reporting, OSHA documentation. Under a PEO arrangement, these tasks transfer to the provider.

That's not a small thing for a company with one HR generalist or a COO who doubles as the HR department.

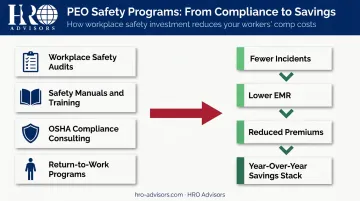

Proactive Safety Programs

The better PEOs don't just process claims — they work to reduce them. Safety program support typically includes:

- Workplace safety audits and hazard assessments

- Industry-specific safety manuals and training materials

- OSHA compliance consultants

- Return-to-work programs that reduce lost-time costs

Fewer incidents mean lower long-term premiums, better EMR, less downtime, and fewer OSHA recordables. Each point improvement in your EMR directly lowers your workers' comp premium at renewal — the savings stack year over year.

Multi-State Compliance Coverage

Workers' comp is regulated at the state level. Benefits structures, coverage requirements, dispute resolution processes, and penalty frameworks differ by jurisdiction. Ohio, North Dakota, Washington, and Wyoming operate state-fund monopolies — private carriers aren't permitted.

A PEO with multi-state experience handles these complexities on the employer's behalf, removing the need for separate policy management in each state where employees work.

Non-compliance carries serious financial consequences. New York can assess $2,000 per 10-day period without coverage. Florida's penalty equals twice the manual premium owed for the preceding 12 or 24 months. California penalties can reach $100,000. These aren't theoretical risks — they're line items that a PEO relationship is specifically designed to prevent.

What Workers' Comp Outsourcing Covers (and What It Doesn't)

What a PEO Typically Handles

- Policy procurement and renewals

- Certificate of insurance issuance

- First report of injury coordination

- Claims management and adjuster liaison

- OSHA 300/A log maintenance and recordkeeping

- Return-to-work program support

- Safety training programs and resources

- Payroll-based premium calculations (pay-as-you-go)

What Remains the Employer's Responsibility

- Maintaining a physically safe work environment

- Reporting injuries to the PEO promptly

- Cooperating with injury investigation processes

- Making operational decisions that affect safety (equipment, staffing, facility layout)

- Bearing responsibility for willful safety violations

Safety culture cannot be outsourced. A PEO manages the administrative and compliance infrastructure around workers' comp, but the physical work environment remains your responsibility.

That distinction also shapes how much your coverage scope matters — which varies significantly depending on the PEO you choose.

Coverage Scope Varies by PEO

Some PEOs own their workers' comp carrier directly, which means tighter control over claims handling, faster response times, and often better pricing. Others access coverage through third-party insurers, which can deliver competitive rates but generally involves more intermediaries in the claims process.

Always ask prospective PEO partners:

- Do you own your workers' comp carrier, or access coverage through a third party?

- Does your master policy cover my industry's class codes without exclusions?

- Which services are included in the base arrangement versus billed as add-ons?

Industry-Specific Considerations for Workers' Comp Outsourcing

High-Risk Industries: Where the Math Is Most Compelling

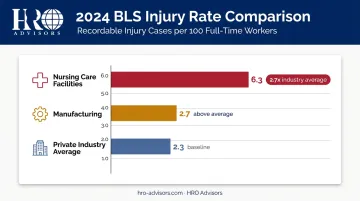

Construction, manufacturing, healthcare, and senior living face the highest workers' comp class codes, incident rates, and premium exposure. BLS 2024 data shows nursing care facilities at 6.3 total recordable cases per 100 full-time workers — nearly three times the private-industry average of 2.3. Manufacturing sits at 2.7.

These industries gain the most from PEO group purchasing power and dedicated safety programs. PEOs with genuine experience in high-risk sectors (like those HRO Advisors works with in construction, manufacturing, and senior living) carry better carrier relationships for difficult class codes and offer tailored safety resources that generic providers don't.

Lower-Risk Industries: Compliance and Documentation Drive Value

Technology, consulting, financial services, and professional services firms see fewer workplace injuries, so the premium savings argument is less dramatic. The value proposition shifts to:

- Administrative simplicity — eliminating policy management from an already lean HR function

- Compliance assurance — ensuring coverage meets state requirements as headcount grows or employees move across states

- Clean documentation — contracts with enterprise clients or government entities often require certificates of insurance; a PEO handles this automatically

For a 30-person SaaS company, workers' comp integration isn't about dramatic rate reductions. It's about coverage that runs cleanly in the background, without demanding management attention.

Multi-State Employers

Workers' comp complexity scales with geography. Every state where you employ workers adds a new regulatory layer:

- Different benefits structures and payment schedules

- Separate filing requirements and dispute resolution processes

- Mandatory state-fund coverage in four states (Ohio, North Dakota, Washington, Wyoming)

A PEO with genuine multi-state experience removes this complexity, managing compliance across all jurisdictions through a single provider relationship.

How to Choose the Right HR Outsourcing Partner for Workers' Comp Coverage

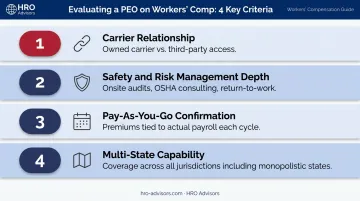

Evaluating PEOs on workers' comp terms is harder than comparing price sheets. Here's what actually matters:

1. Carrier relationship Find out whether the PEO owns its carrier or accesses coverage through third parties. Owned carriers generally mean faster claims handling and more pricing control. Also confirm your industry's class codes are covered without exclusions.

2. Safety and risk management depth Look beyond claims processing. Ask specifically about onsite safety audits, industry-specific safety manuals, OSHA consultation services, and return-to-work program support. A PEO's investment in loss prevention directly affects your long-term premium trajectory.

3. Pay-as-you-go confirmation Verify that premiums are calculated based on actual payroll each pay cycle. Confirm how year-end adjustments work and whether clients have historically received surprise audit bills.

4. Multi-state capability If you have employees in multiple states, confirm the PEO has demonstrated experience managing workers' comp compliance across those specific jurisdictions — including any monopolistic states.

Comparing multiple PEOs side-by-side on these dimensions is difficult to do independently. HRO Advisors runs that comparison for you — evaluating up to 8 PEOs side-by-side on their workers' comp programs, carrier relationships, and pricing. The process starts with a 15-minute call at no cost to your business; HRO Advisors is compensated by the selected provider, not the client.

For construction, manufacturing, senior living, and multi-state businesses, matching to a PEO with the right carrier relationship for your specific class codes can meaningfully reduce both your base rate and your audit exposure.

Frequently Asked Questions

Do HR outsourcing providers handle workers' comp claims?

PEOs typically manage the full claims process — first report of injury, adjuster coordination, and return-to-work support. Non-PEO HR outsourcers (ASOs and à la carte providers) generally offer administrative assistance only, leaving the employer to manage the substantive claims relationship directly.

What is the average cost of HR outsourcing services?

PEO pricing is typically structured as a per-employee per-month fee or a percentage of payroll. NAPEO's research cites an average annual PEO cost of approximately $1,395 per employee, against average savings of $1,775 per employee. Workers' comp premiums are generally calculated separately on a pay-as-you-go basis. Request quotes from multiple providers to understand total cost of ownership — the components vary meaningfully across PEOs.

Which HR functions should not be outsourced?

Final employment decisions (hiring, termination, discipline), company culture development, direct employee relations, and physical workplace safety management remain the employer's responsibility regardless of outsourcing arrangement. Administrative and compliance-heavy functions transfer well to a PEO — but leadership decisions and organizational culture stay with you.

Can small businesses get better workers' comp rates through a PEO?

Yes. PEOs pool risk across their entire client base under a master workers' comp policy, which typically provides access to lower rates than small businesses can negotiate independently. The savings are most significant for businesses in higher-risk industries, though even lower-risk employers benefit from the elimination of audit exposure and administrative overhead.

What is the difference between a PEO's workers' comp coverage and a standalone policy?

A standalone policy requires an upfront premium deposit and annual payroll audits. A PEO's coverage operates under a master policy with pay-as-you-go billing and includes integrated claims management, OSHA recordkeeping support, and safety programs — all bundled into the HR outsourcing relationship rather than managed as separate vendor contracts.