For Applicable Large Employers (ALEs), the stakes are real. Failing to offer minimum essential coverage can trigger per-employee penalties exceeding $2,000 annually per uncovered worker. With the IRS having eliminated good-faith relief for reporting errors, even honest mistakes on Form 1095-C now carry the same penalty exposure as willful non-compliance.

This guide is written for employers with 50 or more full-time equivalent employees — and for businesses approaching that threshold who want to get ahead of the requirements. We cover what ACA compliance actually demands from HR teams year-round, the most common failure points, and how outsourcing through a PEO can absorb much of this burden.

Key Takeaways

- ALEs must offer minimum essential coverage to at least 95% of full-time employees or face steep per-employee penalties

- The 2026 ACA affordability threshold of 9.96% of household income sets the ceiling — exceed it and coverage fails the affordability test

- ACA compliance is a year-round obligation — not just an annual filing exercise

- Variable-hour and seasonal workers create disproportionate compliance risk

- PEOs provide compliance infrastructure and large-group health plan access that makes meeting affordability requirements more manageable

- HRO Advisors offers a free side-by-side comparison of up to 8 PEO providers — no cost to the client

What Is ACA Compliance and Who Does It Apply To?

The Affordable Care Act, signed into law on March 23, 2010, created ongoing obligations for certain employers to provide qualifying health coverage or face shared responsibility payments. Compliance isn't a once-a-year filing. It requires tracking employee hours, managing eligibility, and maintaining accurate records every single month.

The ALE Threshold

Whether these rules apply to your business starts with one question: are you an Applicable Large Employer?

An organization qualifies as an ALE if it employed an average of 50 or more full-time equivalent employees during the prior calendar year. This determination must be made annually using prior-year data, per IRS guidance on ALE determination.

FTE calculations catch many employers off guard. Part-time employees' hours are aggregated and divided by 120 to convert them into FTEs. A business with 35 full-time employees and 20 part-timers each working 60 hours per month could still qualify as an ALE, even with fewer than 50 actual full-time workers.

Who Counts as Full-Time Under the ACA?

Any employee averaging 30 or more hours per week (or 130+ hours per month) is considered full-time and must be offered coverage. For tracking purposes, employers can choose between two measurement methods:

- Monthly measurement method — Assesses each employee's hours month by month

- Look-back measurement method — Tracks hours over a defined measurement period to determine eligibility during a future stability period

The look-back method allows measurement periods of 3–12 months for ongoing employees. If an employee is full-time during the measurement period, the stability period must be at least 6 months and no shorter than the measurement period.

Variable-hour and seasonal employees present the highest risk. Their hours are difficult to predict, and misclassification — treating someone as part-time when aggregated hours cross the 30-hour threshold — can result in a missed coverage offer and a penalty assessment.

Core ACA Employer Obligations

Coverage and Affordability Requirements

ALEs must meet two coverage standards:

- Minimum Essential Coverage (MEC) must be offered to at least 95% of full-time employees and their dependents

- Minimum Value (MV) requires the plan to cover at least 60% of total allowed benefit costs

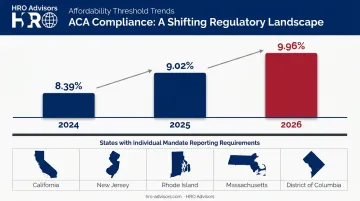

The affordability requirement adds a third layer: the employee's share of the self-only premium cannot exceed a set percentage of their household income. For plan years beginning in 2026, that percentage is 9.96%, up from 9.02% in 2025.

Since employers rarely have access to employees' actual household income data, the IRS provides three affordability safe harbors:

| Safe Harbor | Basis |

|---|---|

| W-2 Safe Harbor | Uses the employee's Box 1 W-2 wages |

| Rate-of-Pay Safe Harbor | Uses hourly rate × 130 hours (or monthly salary) |

| Federal Poverty Line Safe Harbor | Uses the FPL for a single individual, divided monthly |

Using a safe harbor protects the employer from affordability penalties even if an employee receives a marketplace subsidy — as long as the safe harbor calculation is applied correctly.

ACA Reporting Requirements and Deadlines

ALEs must file two IRS forms annually:

- Form 1095-C — Furnished to each full-time employee; details the coverage offered, the employee's share of the premium, and months of coverage

- Form 1094-C — A transmittal summary sent to the IRS with all 1095-C forms attached

2026 filing deadlines for tax year 2025:

- Furnish 1095-C to employees: March 2, 2026

- Electronic filing with IRS: March 31, 2026

Employers filing 10 or more information returns must file electronically. Paper filing is due March 2, 2026 — the same date as employee furnishing.

Miss those deadlines and the costs add up fast. The IRS eliminated good-faith transition relief after 2020, so honest mistakes carry the same weight as deliberate ones. Per-return penalties for returns due in 2026 are:

- $60 if filed up to 30 days late

- $130 if filed more than 30 days late through August 1

- $340 if filed after August 1 or not at all

- $680 for intentional disregard (no annual maximum)

These apply separately for failing to file with the IRS (IRC 6721) and failing to furnish correct statements to employees (IRC 6722). For large employers, annual maximums reach $4,098,500 for willful violations.

Common ACA Compliance Challenges for HR Teams

Managing ACA compliance in-house is genuinely hard. Three challenges account for most compliance failures.

Data Fragmentation

When payroll, timekeeping, benefits enrollment, and HRIS systems operate independently, accurate FTE calculations and eligibility tracking become nearly impossible. ADP reports that ACA IRS transmissions can trigger more than 130 potential form and file errors, with employee name and Social Security number mismatches among the most common — all of which stem from disconnected systems.

Variable Workforce Complexity

The scale of the part-time workforce makes this a widespread issue. BLS data from May 2025 shows 28.7 million people employed part-time in the US. For employers in retail, hospitality, healthcare, and similar sectors, a large portion of their workforce may require careful hour-by-hour tracking to determine ACA eligibility accurately.

Escalating Regulatory Burden

The compliance landscape shifts every year:

- Affordability percentages adjust annually (from 8.39% in 2024, to 9.02% in 2025, to 9.96% in 2026)

- Per-form penalty amounts increase

- Multiple states — including California, New Jersey, Rhode Island, Massachusetts, and DC — have their own individual health insurance mandates requiring separate employer reporting

For lean HR teams already managing hiring, payroll, and employee relations, this volume of regulatory change is difficult to track consistently.

The Case for Outsourcing ACA Compliance

Time and Bandwidth

ACA compliance isn't limited to the year-end filing sprint. Month by month, HR teams must track hours, run eligibility checks, verify affordability calculations, and audit benefit enrollment data. The year-end form preparation and IRS filing adds an intensive layer on top of that ongoing workload.

Outsourcing recaptures that time for higher-value work: building teams, planning compensation, and developing the programs that drive retention.

Penalty Risk Reduction

Disconnected systems feeding inaccurate data into 1095-C forms remain the primary driver of penalty exposure. Outsourced compliance partners consolidate and audit data continuously, catching errors before they become IRS inquiries.

When a Letter 226J does arrive, an experienced partner can respond on the employer's behalf. That capability matters more now: the 2024 Employer Reporting Improvement Act extended the response window to 90 days for assessments in taxable years beginning after December 23, 2024.

State Mandate Coverage

At least five jurisdictions have standalone health coverage reporting requirements:

- California — MEC providers report to the FTB

- New Jersey — Employers file NJ-1095 or federal equivalent forms

- Rhode Island — Uses 1095-B/C for mandate reporting

- Massachusetts — Employers with 6+ employees file the HIRD form by December 15

- District of Columbia — Applicable entities file health care information returns

Most in-house HR teams can manage federal ACA requirements adequately at scale. Managing federal plus multiple state mandates simultaneously is where gaps emerge. Specialized outsourcing partners handle both layers without additional complexity for the employer.

Year-Round Audit Readiness

Outsourcing partners maintain continuous records of coverage offers, affordability calculations, and employee status changes. If the IRS issues an inquiry, the documentation already exists — no scramble to rebuild records from disconnected spreadsheets or outdated files.

The practical result: employers enter any audit or IRS review with a complete, organized paper trail rather than a reactive records search.

How PEOs Simplify ACA Compliance

A Professional Employer Organization operates under a co-employment model: the PEO becomes the co-employer of record and assumes significant HR and compliance responsibilities alongside the client business.

For ACA compliance, PEOs bring dedicated compliance teams that manage hour tracking, eligibility determination, affordability calculations, and form preparation as part of their core service. The client business retains operational control while the PEO absorbs the administrative and regulatory burden. Under IRS rules, each ALE member must still file Forms 1094-C and 1095-C under their own EIN, but a PEO can manage the preparation and submission process with the ALE member's identity on the filings.

On the benefits side, PEOs pool employees across hundreds of client businesses to access large-group health plans — the same coverage available to Fortune 500 companies. For smaller ALEs that would otherwise struggle to offer plans meeting ACA minimum value and affordability standards at competitive rates, this pooled purchasing power is a genuine structural advantage.

The PEO market has grown considerably: NAPEO research from 2025 reports more than 230,000 US businesses now partner with a PEO, representing about 15% of employers with 10–499 employees. Penetration is highest — at 15% — among businesses with 50–99 employees, exactly the ALE threshold range where compliance complexity peaks.

Finding the right PEO for a specific workforce structure isn't straightforward, though. HRO Advisors offers a free PEO comparison service that matches businesses with up to 8 PEO providers side-by-side, covering costs, compliance features, and service scope. HRO Advisors is compensated by the selected provider, so there's no cost to the client.

What to Look for in an HR Outsourcing Partner for ACA Compliance

ACA compliance failures — missed deadlines, inaccurate 1095-C filings, IRS Letter 226J responses — often come down to choosing the wrong outsourcing partner. Before you commit, vet candidates against these three criteria:

ACA-Specific Experience

- Ask whether the vendor has experience responding to IRS Letter 226J notices on behalf of clients

- Request references from businesses with similar workforce complexity — variable-hour workers, multiple locations, or seasonal staff

- Confirm the vendor has handled affordability safe harbor calculations, not just basic form filing

Data Integration Capabilities

A strong partner pulls data directly from your existing payroll, timekeeping, HRIS, and benefits enrollment systems — disconnected data is the leading cause of 1095-C errors. Ask vendors specifically:

- How do they ingest data from your current systems (API, flat file, manual export)?

- What happens when data conflicts between systems — who resolves it and how fast?

- Do they flag discrepancies before filing, or only after an IRS notice arrives?

Scope and Cost Transparency

Before committing, clarify:

- Does the partner cover state individual mandate reporting for every state where you have employees, or only federal ACA requirements?

- Is pricing per-employee, flat fee, or modular — and what's excluded from the base quote (state filings, penalty response, amendments)?

- What security protocols protect SSNs and health enrollment data during transfer, storage, and filing?

Frequently Asked Questions

What is ACA compliance and why does it matter for HR?

ACA compliance refers to an employer's obligations under the Affordable Care Act — primarily offering affordable minimum essential health coverage to full-time employees and filing annual IRS reports. HR teams bear primary responsibility for tracking eligibility, managing benefits, and avoiding penalties that can reach millions of dollars annually.

Do small businesses need to comply with the ACA?

The ACA employer mandate applies only to Applicable Large Employers with 50 or more FTE employees. Businesses below that threshold are exempt — but companies approaching 50 FTEs should start planning now, since ALE status is based on prior-year headcount.

What forms do employers need to file for ACA compliance?

ALEs must file Form 1095-C (furnished to each full-time employee by March 2) and Form 1094-C (transmittal summary filed electronically with the IRS by March 31). Employers with 10 or more information returns must file electronically.

What are the penalties for ACA non-compliance?

Two separate penalty tracks apply: reporting penalties (ranging from $60 to $680 per return in 2026, with no annual cap for intentional disregard) and employer shared responsibility payments assessed per employee for failing to offer coverage. Both can compound quickly across a large workforce.

How does a PEO help with ACA compliance?

PEOs assume co-employer status and take on ACA tracking and reporting responsibilities through dedicated compliance teams. They also provide access to large-group health plans that more easily meet ACA affordability and minimum value standards, and maintain year-round documentation to support IRS audit responses.

What is the ACA affordability threshold for 2026?

The 2026 affordability percentage is 9.96%, per IRS Rev. Proc. 2025-25. An employee's required contribution for self-only coverage cannot exceed that share of household income to qualify as affordable under IRS safe harbor tests.