What makes this especially costly is that most payroll tax filing errors aren't random. They trace back to predictable, preventable causes — disconnected systems, manual data entry, inconsistent compliance practices, and multi-jurisdictional complexity that outpaces what most internal teams can track manually.

This article examines where those errors actually originate, what drives their cost over time, and the specific automation strategies — process, technology, and structural — that companies use to prevent them.

Key Takeaways

- The IRS assessed nearly $1.15 billion in employment-tax penalties in FY2025 — noncompliance has a measurable price tag.

- Most filing errors originate upstream in disconnected systems and manual data entry, not in the final tax calculation.

- Automation enforces tax rules in real time, catches data errors before submission, and preserves audit-ready records.

- Partnering with a PEO transfers filing responsibility to a co-employer with dedicated compliance infrastructure already in place.

- Lasting compliance requires integrated technology, clear process controls, and the right organizational structure working together.

How Payroll Tax Filing Errors Build Up Over Time

Payroll tax errors don't arrive as a single catastrophic event. They start small — a missed jurisdictional rate update, an unreviewed withholding change, a termination processed a week late — and compound across pay cycles into a material liability.

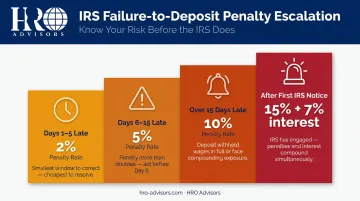

The penalty structure makes the cost escalation swift:

- 1–5 days late on a deposit: 2% penalty

- 6–15 days late: 5% penalty

- More than 15 days late: 10% penalty

- Unpaid after the first IRS notice: 15% penalty, with underpayment interest (currently 7% for Q3 2026) running simultaneously

A single Form 941 underreporting error also triggers Form 941-X, which IRS estimates require 26 hours and 38 minutes to complete per correction — most of that in recordkeeping and documentation. That's rework time that compounds with each affected pay period.

Why the Gap Between Error and Discovery Is Costly

For businesses running payroll manually or across disconnected tools, there's often no real-time signal when something goes wrong. An error surfaces one pay cycle, goes undetected through several more, and only appears when an IRS notice arrives or year-end reconciliation exposes the gap.

By then, penalties and interest have already accumulated across multiple quarters. What makes this worse: IRS employment-tax examiners may expand audits to prior and subsequent years when errors are material or recurring — meaning one discovered mistake can pull multiple periods into scope.

Key Cost Drivers for Payroll Tax Filing Errors

Disconnected Systems and Manual Data Entry

The most fundamental driver is the absence of a single source of truth. When HR, time-and-attendance, and payroll systems operate independently, the same employee data must be re-entered across platforms with each pay cycle — and each transfer creates an opportunity for inconsistency.

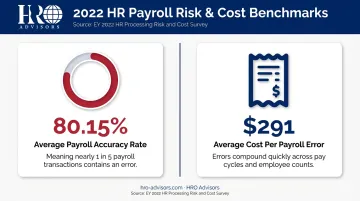

EY's 2022 HR Processing Risk and Cost Survey puts the average U.S. payroll accuracy rate at 80.15%, implying a nearly 20% error rate, with an average cost of $291 per payroll error. While that covers broader payroll processing errors, the mechanism applies directly to tax filing: bad input data produces inaccurate withholdings and deposits.

Multi-Jurisdictional Complexity

The Tax Foundation counts 5,055 local income-tax jurisdictions across 16 states. Each carries its own rate, filing frequency, and deadline structure. For businesses with remote workers or employees across state lines, the risk of applying outdated or incorrect tax configurations grows with every jurisdiction added.

Two common examples illustrate how quickly obligations stack up:

- Pennsylvania employers must withhold both Earned Income Tax and Local Services Tax

- Ohio requires withholding for school district income tax where applicable

These are standard obligations — not edge cases — and they change regularly.

Workforce Events as a High-Risk Trigger

New hires, terminations, pay-rate changes, benefit elections, and reclassifications all affect withholding accuracy. When teams process these events manually or with delays, the downstream effect on tax filings can cascade across multiple pay periods.

Worker misclassification is a specific, high-cost version of this problem. A GAO report found that 15% of employers historically misclassified workers, and IRS Section 3509 rules can impose back withholding and FICA liability — plus penalties and interest — when an employee is incorrectly treated as an independent contractor.

Limited Internal Compliance Expertise

Automated systems also fail when tax tables, classification rules, or jurisdiction setups fall out of date. Without dedicated compliance expertise, regulatory changes accumulate unnoticed — until a filing reflects a rate or rule that's no longer valid.

How Automation Reduces Payroll Tax Filing Errors

Automation reduces errors through three distinct mechanisms: changing the decisions made before payroll runs, improving how the process is managed during each cycle, and altering the organizational structure around payroll. Each lever operates at a different stage — and together, they address most of the conditions that allow filing errors to occur.

Strategies That Change Decisions at the Source

These are structural choices that reduce error risk before any payroll cycle begins:

- Consolidate HR, time-and-attendance, and payroll into one integrated platform. When pay-rate updates, benefit elections, or new hires flow automatically into tax calculations, manual reentry — and the errors it introduces — is eliminated.

- Select payroll software with automatically updated tax tables. The system should pull current federal, state, and local rates without manual intervention, so outdated rates never reach a filing.

- Enforce classification rules within the system itself. Worker type, exempt/non-exempt status, and associated tax treatment should be applied by rule, not manual review.

- Define data governance policies for each payroll cycle. Establish who can change withholding, when changes take effect, and how new hires and terminations are confirmed before they reach the filing stage.

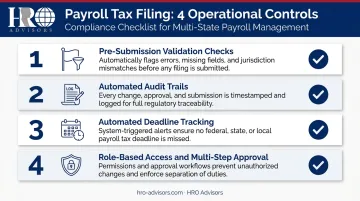

Strategies That Improve How Filing Is Managed

These operational controls catch errors before funds move and filings are submitted:

- Implement pre-submission validation checks. Automated flags for missing tax setups, unusual gross-to-net variances, negative net pay, or unreviewed withholding changes turn exception management into a routine pre-run step.

- Maintain automated audit trails. Every pay-impacting change — who made it, when, and what was modified — should be logged automatically. This documentation is essential when responding to IRS correspondence or internal audits.

- Automate deadline tracking. System-driven reminders and workflows reduce the risk of missed deposits or filings, particularly for businesses managing multiple state and local tax authorities with differing frequencies.

- Enforce role-based access and multi-step approval. Sensitive fields — tax withholding, direct deposit, employee classification — should require documented review before any change takes effect.

Strategies That Change the Organizational Context

Some errors persist not because of bad processes, but because the environment around payroll creates conditions where mistakes are hard to prevent. These structural changes address that:

- Partner with a Professional Employer Organization (PEO). A PEO assumes co-employer responsibility for payroll tax filings, operates dedicated compliance infrastructure, and files taxes under its own EIN — shifting the filing burden to an organization built for it. Businesses comparing PEO providers can use HRO Advisors to run free side-by-side comparisons of up to 8 providers from a network of 500+.

- Assign dedicated payroll compliance ownership. Designate a specific role — internal or outsourced — responsible for monitoring regulatory changes, validating filings, and maintaining jurisdiction-specific rule sets. Distributed accountability is a common source of missed updates.

- Build centralized payroll governance for multi-state operations. Standardize approval workflows and reporting requirements across all locations, while allowing jurisdiction-specific inputs where local rules require them.

- Implement ongoing compliance monitoring. Whether through software or a managed service, proactive regulatory tracking across all relevant jurisdictions prevents filing errors caused by undetected rule changes.

Conclusion

Reducing payroll tax filing errors starts with identifying where they actually originate — in disconnected systems, manual data entry, delayed workforce event processing, or organizational structures that weren't designed for compliance at scale. Adding more manual review at the end of the cycle doesn't fix root causes. It only adds another step that can itself introduce error.

The businesses that consistently avoid costly IRS penalties and correction cycles are those that align the right technology, operating controls, and partner structure. For many small to mid-sized companies, that partner structure means working with a PEO or managed payroll provider — one selected specifically for their industry, workforce complexity, and multi-state exposure. Getting that match right is often where the compliance picture changes most quickly.

Frequently Asked Questions

How can companies reduce payroll tax filing errors with automation?

Automation reduces errors by centralizing payroll data across HR, time-tracking, and payroll systems, enforcing current tax rules in real time, and running pre-submission validation checks that flag discrepancies before any filing is submitted. The result: errors are caught before submission, not discovered after the fact.

What are the benefits of payroll automation?

The primary benefits are fewer manual calculation errors, faster processing cycles, and built-in compliance with changing tax laws across multiple jurisdictions. Automated systems also generate audit-ready documentation as a standard output, with no additional administrative effort required from your team.

What are the most common payroll tax filing errors companies make?

The most frequent mistakes include incorrect withholding amounts, missed deposit deadlines, misclassified workers, and outdated tax rates applied due to manual or delayed system updates. Multi-state businesses face compounded risk as each jurisdiction adds its own rate and filing schedule.

How does a PEO help with payroll tax filing compliance?

A PEO assumes co-employer responsibility for payroll tax filings, typically filing under its own EIN using dedicated automated compliance systems. This transfers day-to-day filing execution to an organization built to stay current across all jurisdictions, reducing the compliance burden on the client business.

What should businesses look for in an automated payroll tax solution?

Key criteria include automatic tax table updates, multi-jurisdiction support, pre-submission validation, integration with HR and time-tracking systems, complete audit trail capabilities, and role-based access controls. Scalability and real-time regulatory monitoring round out the checklist.

Can small businesses benefit from payroll tax automation?

Small businesses are often the highest-risk group — the IRS estimates employers with 1–5 employees spend nearly 16 hours per employee annually on Form 941 compliance alone. Payroll automation, or partnering with a PEO, delivers the same compliance safeguards at a proportional cost and without requiring a dedicated internal HR team.