According to SHRM's 2025 Employee Benefits Survey, 88% of employers rated health-related benefits as extremely or very important for recruitment and retention. That's not just an HR issue — it's a business strategy issue.

This guide covers everything employers need to know: the types of benefits available, the administration process from start to finish, key compliance laws, best practices, and when to consider outsourcing.

Key Takeaways

- Health benefits are a top recruitment and retention lever: 88% of employers rank them as critical to their workforce strategy

- Effective benefits administration is a year-round process, not an annual event

- ACA, ERISA, COBRA, and HIPAA create significant compliance obligations for most employers

- Multi-state workforces face layered, jurisdiction-specific compliance requirements

- Small and mid-sized businesses can access Fortune 500-level health plans and group rates by partnering with a PEO

What Is HR Benefits Management?

HR benefits management is the full process of selecting, designing, implementing, and administering employee benefits programs. That includes health insurance, retirement plans, paid leave, life insurance, and increasingly, wellness and mental health programs.

The responsibilities involved are broad:

- Managing open enrollment windows

- Tracking employee eligibility changes (hires, terminations, life events)

- Coordinating with insurance carriers and third-party vendors

- Ensuring payroll deductions are accurate and timely

- Keeping the organization legally compliant with federal and state law

The administrative side is just half the picture. Benefits are also a direct talent lever — research consistently shows that health coverage ranks among the top factors candidates weigh before accepting a job offer, and employees who feel underserved by their benefits are quicker to leave. For employers, that makes benefits management both an operational necessity and a retention strategy.

Types of Employee Benefits Employers Should Know

Legally Required Benefits

Some benefits aren't optional. Federal law mandates them regardless of company size or preference:

- Social Security and Medicare (FICA): Employers contribute 6.2% for Social Security (up to a $184,500 wage base in 2026) and 1.45% for Medicare, matched dollar-for-dollar by employees

- Federal unemployment insurance (FUTA): 6.0% on the first $7,000 of each employee's wages, often reduced to 0.6% after state tax credits

- Workers' compensation: Required in virtually all states; rates and rules vary by jurisdiction

- FMLA protections: Employers with 50+ employees must provide up to 12 weeks of unpaid, job-protected leave to eligible employees who have worked at least 12 months and 1,250 hours

Common Voluntary Benefits

Beyond legal minimums, most employers offer a core set of voluntary benefits that candidates now expect as standard:

- Employer-sponsored health, dental, and vision insurance

- Life and disability insurance

- 401(k) or other retirement savings plans, typically with employer match

- Paid time off (vacation, sick leave, company holidays)

Emerging and Competitive Benefits

Employers looking to attract and retain strong candidates are expanding beyond the basics. SHRM's 2025 data shows 68% of employers rated flexible working benefits as highly important, with 60% offering hybrid arrangements. Other growing offerings include:

- Employee assistance programs (EAPs) and mental health support

- Tuition reimbursement and student loan assistance

- Childcare stipends and family-building benefits

- Remote work stipends and commuter benefits

- Wellness programs (though onsite stress management program availability dropped from 26% to 17% between 2021 and 2025)

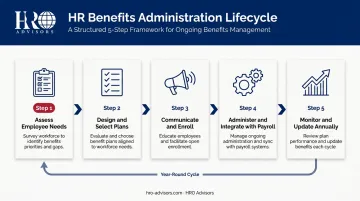

The HR Benefits Administration Process: Step by Step

Effective benefits administration isn't a one-time setup — it's an ongoing lifecycle that runs year-round. Here's how it works in practice.

Step 1: Assess Employee Needs

Before selecting any plans, gather real data from your workforce. Employee surveys should cover:

- Benefit preferences by type (health, dental, retirement, flexible work)

- Dependent status and family coverage needs

- Utilization of current offerings

- Gaps where employees feel underserved

This matters more than most employers realize. Research from EBRI found that 50% of health plan enrollees spent less than one hour choosing a health plan. Without employer guidance grounded in actual employee needs, your benefits spend may not land where it should.

Step 2: Design and Select Benefit Plans

Translate employee feedback into a concrete package. This involves:

- Soliciting proposals from multiple carriers and vendors

- Comparing cost vs. coverage value across options

- Deciding on contribution structures (what the employer covers vs. what employees pay)

- Aligning selections with company budget and workforce strategy

Don't optimize purely on price. A plan that's cheap to administer but confusing to employees generates its own hidden costs in HR time and underutilization.

Step 3: Communicate Benefits and Manage Enrollment

Poor communication is the most preventable benefits failure. A 2021 Voya survey found 35% of employed individuals did not fully understand any benefits they selected during their last open enrollment. That's a communication problem, not an employee problem.

Effective enrollment communication means:

- Starting 4–6 weeks before open enrollment opens

- Using multiple channels: email, intranet, video walkthroughs, live Q&A sessions

- Explaining cost impact clearly — what changes on their paycheck

- Clarifying the difference between locked (election-required) and flexible benefits

- Communicating how qualifying life events (marriage, birth, loss of coverage) open a special enrollment window outside the standard period

Step 4: Administer and Integrate with Payroll

Once enrollment closes, accurate data handoff to carriers and payroll is where manual processes introduce the most risk. Ongoing administration involves:

- Transmitting enrollment data accurately to each carrier

- Ensuring payroll deductions reflect current elections and eligibility status

- Processing changes for new hires, terminations, and mid-year life events

- Maintaining audit-ready records

Benefits administration software or an integrated HRIS platform reduces error rates and catches deduction mismatches before they reach employees. The more manual your process, the greater your exposure to missed coverage notices and compliance gaps.

Step 5: Monitor, Measure, and Update Annually

Benefits programs require continuous evaluation. Key metrics to track throughout the year:

| Metric | What It Tells You |

|---|---|

| Enrollment rate by plan | Which offerings resonate vs. go unused |

| Claims costs and loss ratios | Whether plan pricing will hold at renewal |

| Employee satisfaction scores | Whether benefits are meeting needs |

| Cost per employee | Year-over-year trend to benchmark against peers |

Review these metrics at least 90 days before renewal — early enough to renegotiate carrier terms, adjust plan design, or shift contributions before employee elections open.

Benefits Compliance: Key Laws Employers Must Know

Non-compliance with benefits regulations creates financial penalties, legal exposure, and employee distrust. These four federal frameworks are mandatory for most employers.

The Affordable Care Act (ACA)

Applicable Large Employers (ALEs) — those averaging 50+ full-time equivalent employees — must offer affordable, minimum-value health coverage to full-time employees or face shared responsibility payments. For 2026, the IRS has set the 4980H(a) penalty at $3,340 and the 4980H(b) penalty at $5,010 per employee (annualized).

ALEs must also file Forms 1094-C and 1095-C annually. For the 2025 tax year, the paper filing deadline is March 2, 2026, and electronic filing is due by March 31, 2026.

ERISA, COBRA, and HIPAA

Three additional federal laws govern most employer-sponsored benefit plans:

- ERISA: Requires fiduciary responsibilities, plan documentation, and delivery of a Summary Plan Description (SPD) to participants within 90 days of coverage becoming effective

- COBRA: Employers must notify the plan administrator within 30 days of a qualifying event (termination, reduced hours, etc.). The plan administrator then has 14 days to send an election notice. Qualified beneficiaries get at least 60 days to elect continuation coverage

- HIPAA: Group health plans are covered entities under HIPAA. Any vendor handling protected health information (PHI) on the plan's behalf must provide written assurances of data safeguards — especially relevant when using digital benefits platforms

State Mandates and Multi-State Complexity

Multi-state employers face layered obligations that go beyond federal law. As of 2025, NCSL reports that 13 states and DC have enacted mandatory paid family and medical leave laws, with benefits already operational in 10 jurisdictions and beginning in four more states in 2026.

State-level obligations extend further than paid leave. Additional mandates vary by jurisdiction but commonly include:

- Temporary disability insurance — required in California, New Jersey, New York, Rhode Island, and Hawaii

- Individual health coverage mandates — enforced in five states and DC, with penalties for non-compliance

For employers with remote or hybrid workforces, the employee's work location determines which state laws apply — not the employer's headquarters. That means HR must track every jurisdiction where employees work and update plan documents accordingly.

Building a Compliance Calendar

A year-round compliance calendar keeps deadlines visible and prevents costly oversights. Build a year-round calendar that includes:

- ACA reporting deadlines (paper and electronic)

- COBRA notification windows (30-day employer notice, 14-day administrator window, 60-day election period)

- Open enrollment start and close dates

- State-specific paid leave and mandate deadlines

- Annual plan review and SPD update checkpoints

Assign a dedicated point person and set calendar reminders for each window — missing a single COBRA deadline can trigger penalties and litigation.

Best Practices for Effective HR Benefits Management

Communicate Early, Often, and Clearly

Start enrollment communications 4–6 weeks before open enrollment, using:

- Email campaigns with plan comparison summaries

- Video walkthroughs of each plan option

- Live or recorded Q&A sessions

- Intranet resources employees can revisit

Explain exactly what changes on an employee's paycheck for each plan option. When the cost impact is clear, participation improves. Voya's research found 66% of working Americans wanted their employer to provide year-round education on benefits — not just during open enrollment.

Leverage Technology to Reduce Administrative Burden

Benefits administration software eliminates the most error-prone manual work. When evaluating platforms, look for:

- Self-service employee portals for enrollment and mid-year changes

- Compliance alerts for ACA, COBRA, and ERISA deadlines

- Payroll integration that syncs deductions automatically

- Reporting dashboards for enrollment rates, costs, and utilization

For small and mid-sized businesses that lack dedicated benefits technology, partnering with a PEO through a broker like HRO Advisors provides access to enterprise-grade platforms alongside the benefits themselves — without building or buying the infrastructure independently.

Benchmark and Act on Employee Feedback

Once your technology foundation is in place, the next question is whether your benefits package is actually competitive. Benchmark annually against peers in your industry and company size. Gallagher's benefits benchmarks draw on data from over 4,000 organizations, giving you a clear read on whether your package is keeping pace or falling behind.

That context matters for budgeting, too. Mercer projects a 6.7% increase in health benefit costs for 2026 — the highest in 15 years — so knowing where you stand against peers helps you make defensible decisions about what to absorb, share, or restructure.

Pair benchmarking data with employee feedback. Pre-enrollment surveys and post-enrollment pulse checks are your most actionable data source. When employees see their input reflected in plan changes, it builds trust and makes your company easier to recruit from.

When to Outsource Benefits Administration

Signs In-House Administration Has Become Unmanageable

Most employers reach a breaking point before they consider outsourcing. Common warning signs:

- HR staff spending the majority of their time on administrative tasks, not strategic work

- Compliance errors or near-misses with ACA, COBRA, or ERISA requirements

- Benefits packages that can't compete with what larger employers offer

- High administrative cost per employee relative to the value being delivered

- A current PEO or vendor whose service quality has declined while costs have risen

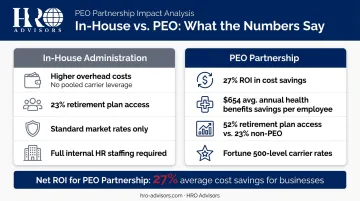

The PEO Model: Better Benefits at Lower Cost

A Professional Employer Organization operates under a co-employment model, pooling employees across many client companies to access group pricing unavailable to smaller organizations independently. Through HRO Advisors, small and mid-sized businesses gain access to health plans from carriers like Aetna, Blue Cross Blue Shield, and UnitedHealthcare at rates typically reserved for large employers.

The financial case is documented. According to NAPEO research, employers using PEOs see a 27% ROI in cost savings alone, with an average of $654 in annual health benefits savings per employee. Among businesses with 10–49 employees, 52% of PEO users had a retirement plan, compared to just 23% of non-users.

HRO Advisors compares up to 8 PEO providers side by side for each client at no cost — their fee is paid by the selected provider, not the employer. The comparison covers cost structure, benefits quality, compliance capabilities, and service levels, giving employers a clear picture without the legwork of evaluating providers independently.

What to Look for in a Benefits Administration Partner

When evaluating outsourcing options, assess:

- Offers comprehensive health, dental, vision, and retirement options

- Manages ACA, COBRA, ERISA, and state-specific obligations proactively

- Provides an employee self-service portal with compliance alerts and payroll integration

- Discloses all fees clearly with no hidden costs

- Has direct experience with employers in your sector and jurisdiction

Evaluating providers against each of these criteria takes significant time — time most HR teams don't have. Working with a PEO broker removes that burden entirely. HRO Advisors handles everything from the initial consultation through provider negotiation, typically getting businesses from problem to solution in under two weeks.

Frequently Asked Questions

What does an HR benefits manager do?

An HR benefits manager designs, administers, and manages the company's employee benefits programs. Responsibilities span plan selection, enrollment oversight, vendor coordination, employee education, and compliance with ACA, ERISA, COBRA, and HIPAA.

Do I contact HR about benefits?

Yes — HR or your designated benefits administrator is the primary contact for all benefits questions. This includes enrolling in plans, making changes after a qualifying life event, understanding plan details, or resolving coverage disputes with a carrier.

What is the difference between open enrollment and a qualifying life event?

Open enrollment is the scheduled annual window when employees elect or change benefits. A qualifying life event — such as marriage, birth of a child, or loss of other coverage — allows changes outside that window, typically within 30–60 days of the event.

What federal laws govern employee benefits in the US?

The four primary federal laws are: the ACA (health coverage mandates for large employers), ERISA (plan fiduciary duties and disclosure requirements), COBRA (continuation coverage rights after loss of eligibility), and HIPAA (health data privacy). State laws vary, so multi-state employers should verify local requirements as well.

Can small businesses offer competitive benefits without a large HR team?

Yes. By partnering with a PEO, small businesses gain access to group pricing, enterprise-level plan options, and built-in compliance and administration support — no large in-house HR team required. HRO Advisors matches businesses with the right PEO at no cost — call 866-755-0288 or visit hro-advisors.com to get started.