Introduction

Hiring a remote employee in another state feels simple — until payroll runs. That first paycheck triggers a chain of obligations most companies didn't anticipate: new state registrations, separate unemployment insurance accounts, workers' compensation coverage, and often local tax filings. Miss any of them, and the penalties start accumulating immediately.

According to the Bureau of Labor Statistics, 35.5 million US workers — nearly 23% of the entire workforce — teleworked or worked from home for pay in Q1 2024. For HR managers, business owners, and operations leaders managing distributed teams, multi-state payroll compliance is no longer an edge case. It's a standard operational challenge.

This guide covers what remote payroll compliance actually requires, how state-by-state rules vary, and when outsourcing to a Professional Employer Organization (PEO) makes more sense than managing it in-house.

Key Takeaways

- A single remote employee working from another state creates tax nexus for the employer there, regardless of where the company is headquartered

- Employers must register with each new state's tax agencies before issuing the first paycheck

- Multi-state withholding rules, reciprocal agreements, and "convenience of the employer" tests vary by state and can trigger double-taxation

- Missing registrations or filing deadlines can trigger IRS penalties of 2%–15%, plus additional state penalties

- Once compliance spans three or more states, partnering with a PEO is often the most practical path forward

What Is Remote Employee Payroll Compliance?

Remote employee payroll compliance is the set of employer obligations — tax registration, withholding, filing, and reporting — that apply in every state where an employee physically performs their work, not just where the company is incorporated or headquartered.

The goal is straightforward: ensure the correct federal, state, and local taxes are withheld from each paycheck and remitted to the right agencies on time, across every applicable jurisdiction.

That's fundamentally different from single-state payroll. In a traditional office setup, compliance concentrates in one location. With a distributed workforce, each employee's home state independently triggers its own compliance footprint — including:

- State tax registration and employer accounts

- Separate withholding and filing requirements

- State-specific rate structures and deadlines

Ten remote employees in eight states means up to eight distinct compliance obligations running simultaneously.

Why Remote Work Creates New Employer Tax Obligations

The Nexus Trigger

When an employee performs work from a state — even from their home — they create a legal connection (nexus) between their employer and that state. That connection gives the state the right to impose registration and withholding obligations on the employer, regardless of whether the company has an office or any other physical presence there.

The Telebright Corp. v. Director, Division of Taxation (N.J. App. Div. 2012) case established a clear precedent: a single full-time employee telecommuting from New Jersey was sufficient to subject a Delaware corporation to New Jersey's Corporation Business Tax. Since that ruling, states have only grown more assertive about enforcing nexus based on remote employees.

What Nexus Triggers for Employers

Once nexus is established, the employer must:

- Register with the state's Department of Revenue to handle income tax withholding

- Register with the state's Department of Labor or Workforce Commission for unemployment insurance (SUI/SUTA)

- Obtain workers' compensation coverage extending to the employee's work state (note: Texas is a notable exception — private employers there are generally not required to carry workers' comp coverage)

- Check for local tax obligations in cities or counties where the employee is based

Worker Classification Comes First

Employers must first confirm whether the worker is a W-2 employee or a 1099 independent contractor. Misclassifying an employee as a contractor to sidestep multi-state obligations carries severe penalties — states apply their own classification tests and enforce them aggressively.

The "Convenience of the Employer" Complication

States including New York, Delaware, Nebraska, and Pennsylvania may tax a remote worker's wages as if they worked at the employer's office — not from the employee's home state — unless the employer required the remote arrangement for a legitimate business reason.

The result: an employee working entirely from Ohio for a New York-based employer might still owe New York income tax, and Ohio taxes the same wages too. According to the Tax Foundation, as of 2025, eight states have some form of convenience-type rules, including Connecticut and New Jersey (retaliatory rules) and Alabama (based on an administrative tribunal position).

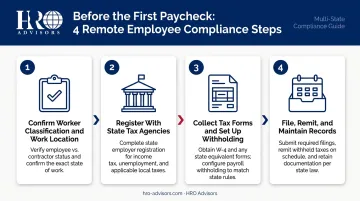

How Remote Payroll Compliance Works: A Step-by-Step Breakdown

Compliance for each remote employee in a new state follows a predictable sequence. Every step below must be completed before the first paycheck is issued.

Step 1: Confirm Worker Classification and Work Location

Determine W-2 or 1099 status first — this drives every obligation that follows. Then confirm exactly which state — and sometimes which city or county — the employee works from.

Employees who split time between states require tracking by days worked in each jurisdiction. Wages must be apportioned accurately to avoid under-withholding in one state and over-withholding in another.

Step 2: Register With State Tax Agencies

Once nexus is confirmed, the employer must:

- Register with the new state's Department of Revenue for income tax withholding

- Register with the Department of Labor or Workforce Commission for SUI

- Obtain workers' compensation coverage for that state

- Check for applicable local or city payroll tax requirements

Registration timelines vary by state. Texas, for example, requires employers to register with the Texas Workforce Commission within 10 days of becoming liable under the state's Unemployment Compensation Act.

Step 3: Collect Tax Forms and Set Up Withholding

Key forms at hire:

- Federal W-4 (and the state-equivalent withholding form for the employee's work state)

- W-9 for independent contractors

At year-end:

- W-2 for employees

- 1099-NEC for contractors paid $600 or more

Multi-state withholding is allocated based on where the employee physically worked. That said, some state pairs have reciprocal agreements that allow withholding only in the employee's home state — a meaningful simplification for workers who cross state lines.

Active reciprocal pairs include:

- Maryland–Virginia

- Illinois–Wisconsin

- Indiana–Kentucky

- New Jersey–Pennsylvania

- Ohio–Indiana

State pairs without agreements may require withholding in both states.

Step 4: File, Remit, and Maintain Records

Ongoing obligations include:

- Quarterly payroll tax returns filed with each state agency

- Timely remittances to each state on their individual schedules

- Year-end W-2 issuance to every employee

- Record retention: The IRS requires at least four years; New York and New Jersey both require six years under state wage rules

State rates, wage bases, and reciprocal agreement terms change year to year — a configuration that was compliant in January may not be by December. Treat this as an ongoing process, not a one-time setup.

Key Compliance Variables That Differ by State

Income Tax Rates

States like Texas, Florida, Nevada, Washington, Wyoming, South Dakota, and Alaska have no individual income tax, eliminating the state income tax withholding obligation for employees there. States like California and New York have graduated structures with rates that can exceed 10%. The employer must apply the correct rate for each employee's specific work state.

SUI/SUTA Rates and Wage Bases

Variation here is dramatic. A few examples for 2026:

- Florida: $7,000 taxable wage base; new employer rate of 2.7%

- Washington: $78,200 taxable wage base; new employers pay 115% of the average rate for their industry

- New York: 4.1% new employer rate (including the Re-employment Services Fund surcharge)

No-income-tax states don't eliminate SUI obligations. Employers still register and pay reemployment or unemployment taxes in every state where they have employees.

Local Payroll Taxes

Certain jurisdictions add another layer:

- New York City: separate withholding tables; MCTMT applies to employers with more than $312,500 in covered quarterly payroll in the Metropolitan Commuter Transportation District

- Philadelphia: Wage Tax of 3.75% for residents and 3.44% for nonresidents as of July 1, 2024

- Ohio municipalities: individual rates vary by city, with lookup available through Ohio's Finder tool

Multi-State Employees

Local taxes add complexity — but multi-state workers take it further. When an employee works across two or more states in a single year, wages must be apportioned by days worked in each jurisdiction. Payroll systems must track and split this accurately; getting it wrong creates simultaneous under-withholding and over-withholding across different states.

Common Remote Payroll Mistakes — and What They Cost

The Three Most Common Failures

- Failing to register before the first paycheck — the employer is non-compliant from day one, with penalties accruing retroactively

- Applying home-state withholding rules to out-of-state employees — withholding for the wrong state and missing the obligation in the employee's actual work state

- Not tracking employee relocations in real time — payroll records lag behind the employee's actual location, creating underpayment in the new state

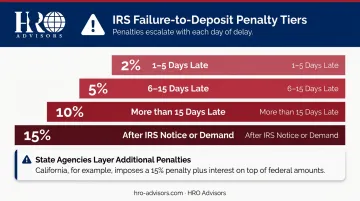

Penalty Exposure

The IRS applies failure-to-deposit penalties on a sliding scale:

| Days Late | Penalty Rate |

|---|---|

| 1–5 days | 2% |

| 6–15 days | 5% |

| More than 15 days | 10% |

| After IRS notice or demand | 15% |

Failure-to-file penalties add another 5% of tax due per month, up to 25%.

Federal penalties are only part of the exposure. State agencies pile on separately — California's EDD, for example, charges a 15% penalty plus interest on late payroll tax payments.

The Compounding Problem

Each state adds a separate compliance footprint. A company with remote employees in eight states that misses registrations in three of them isn't facing one problem — it's facing three concurrent compliance failures, each with its own penalty clock and interest rate. That means three separate deadlines to miss, three penalty schedules accruing interest, and three state agencies that won't coordinate on your behalf.

When Managing Remote Payroll In-House No Longer Makes Sense

The Inflection Point

For companies with employees in one or two states, capable payroll software and a knowledgeable HR team can handle multi-state compliance. But as the state count grows, the administrative load compounds quickly: maintaining separate registrations, tracking regulatory changes, managing local tax jurisdictions, and monitoring SUI accounts across multiple states becomes a significant operational drain.

At that point, most businesses need outside support — the real decision is which type fits best.

How a PEO Addresses This

Under a co-employment arrangement, a PEO becomes the employer of record for payroll and compliance purposes, handling:

- Multi-state registrations and tax account setup

- Withholding calculation and remittance in each jurisdiction

- SUI account management across states

- Workers' compensation coverage

- Year-end W-2 filings

The client company retains full control over day-to-day employee management — job assignments, compensation decisions, performance direction. The PEO absorbs the compliance infrastructure.

According to NAPEO, businesses using PEOs grow twice as fast, experience 12% lower employee turnover, and are 50% less likely to go out of business than comparable non-client firms. The PEO industry currently serves more than 230,000 client companies and 4.5 million employees.

PEO clients also gain access to Fortune 500-level health plans through the PEO's pooled purchasing power — coverage that most small and mid-sized businesses couldn't negotiate independently.

Finding the Right PEO

Not every PEO is the right fit. State footprint, industry, workforce size, and specific compliance requirements all shape which provider will deliver the most value — and the differences between providers aren't always obvious from their marketing.

HRO Advisors works as a PEO broker, analyzing costs and compliance coverage across more than 500 providers to build a focused, side-by-side comparison of 3 to 8 options matched to your industry, state footprint, and workforce structure. The process carries no cost to your business; HRO Advisors is compensated by the provider you select, and that arrangement doesn't affect your pricing.

Clear Signals It's Time to Explore a PEO

- Employees in more than three or four states

- HR staff spending significant time on payroll registrations rather than strategic work

- A penalty notice or payroll audit from any state agency

- Rapid growth with new remote hires regularly added in new states

Frequently Asked Questions

Does having one remote employee in another state create a tax obligation for my company?

Yes. A single remote employee working from a state where you have no prior presence creates tax nexus there, triggering registration, withholding, SUI, and workers' compensation obligations even if you have no office or other footprint in that state.

What is the "convenience of the employer" rule and how does it affect payroll withholding?

States like New York, Delaware, Nebraska, and Pennsylvania tax remote wages as if the employee worked at your office location, unless the remote arrangement was required for genuine business necessity. That means you may owe withholding in your state even when the employee works entirely from home in another state.

Which states have no individual income tax, and does that simplify payroll?

Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming have no state individual income tax, eliminating the state income tax withholding obligation. However, you still need to register for SUI and comply with workers' compensation requirements in those states (with Texas being a notable exception on workers' comp for private employers).

What forms are required when hiring a remote employee in a new state?

At hire: federal W-4 and any state-equivalent withholding form. At year-end: W-2. For independent contractors: W-9 at engagement and 1099-NEC if paid $600 or more during the year.

What are the penalties for missing payroll tax filings or deposits?

The IRS applies failure-to-deposit penalties ranging from 2% to 15% depending on how late the deposit is, plus failure-to-file penalties of 5% per month up to 25%. States layer on their own penalties on top of that; California alone charges 15% plus interest on late deposits.

How can a PEO help manage payroll compliance for a distributed remote workforce?

A PEO takes on co-employer status and manages multi-state registrations, withholding, SUI accounts, workers' comp, and ongoing compliance across every state where your remote employees work. HRO Advisors helps you compare up to 8 PEO providers side-by-side at no cost. Call 866-755-0288 or email info@hro-advisors.com to get started.