Yet many nonprofit leaders assume their 501(c)(3) status reduces their payroll responsibilities. It doesn't. Tax-exempt status protects the organization's income — not its payroll obligations.

This guide covers the four types of workers nonprofits typically employ, the full scope of payroll tax requirements, the challenges unique to the sector, and concrete best practices for staying compliant without drowning in administrative work.

Key Takeaways

- Nonprofits must withhold and remit FICA taxes for all paid employees — 501(c)(3) status does not eliminate payroll tax obligations

- Four worker types require distinct payroll treatment: full-time employees, part-time employees, independent contractors, and volunteers

- Worker misclassification is a primary IRS audit risk for nonprofits

- Grant-funded salaries must be backed by labor distribution reports — a hard requirement under 2 CFR 200.430 for federal audit compliance

- A PEO partnership can cut HR overhead and give nonprofit staff access to benefits that would otherwise be out of reach

Types of Workers in a Nonprofit: What You Need to Know for Payroll

Nonprofits rarely operate with a simple, uniform workforce. Most organizations combine paid staff, independent contractors, and volunteers — each carrying distinct payroll, tax, and legal obligations. The IRS ranks worker misclassification among its top enforcement priorities for exempt organizations, meaning errors here carry real financial and legal risk.

Full-Time and Part-Time Employees

Both full-time and part-time employees are W-2 workers. That means the nonprofit must:

- Withhold federal income tax based on each employee's Form W-4

- Withhold and match FICA taxes (6.2% Social Security + 1.45% Medicare per side)

- Pay at least federal minimum wage under the Fair Labor Standards Act

- Follow all applicable state income tax withholding requirements

Part-time status doesn't reduce these obligations — the same withholding processes apply regardless of hours worked.

On the benefits side, 403(b) retirement plans are available to 501(c)(3) employees. The IRS's universal availability rule requires that if one employee can defer salary, all employees must have the opportunity — with limited exceptions for those working fewer than 20 hours per week.

In a sector where compensation is often constrained, offering retirement benefits is one of the most effective retention tools available.

Independent Contractors

Independent contractors (1099 workers) are not subject to payroll tax withholding. They pay their own self-employment taxes, and the nonprofit has no employer match obligation.

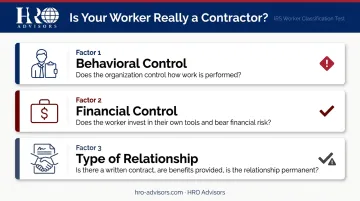

The critical question is whether a worker actually qualifies as a contractor. The IRS uses a three-factor test based on:

- Behavioral control — Does the organization control how the work is done, not just the result?

- Financial control — Does the worker have unrestricted business opportunities, invest in their own tools, and bear financial risk?

- Type of relationship — Is there a written contract? Are benefits provided? Is the relationship permanent?

Nonprofits sometimes classify workers as contractors to reduce costs. That's a significant risk. Under IRS Section 3509, when a worker treated as a nonemployee is reclassified, the organization faces back taxes, interest, and potential penalties — and the IRS actively pursues these cases.

Volunteers and Interns

True volunteers — those who freely give time for charitable purposes with no expectation of compensation — are not employees and carry no payroll obligations. The line blurs quickly, though, and a few rules define where it falls:

- Paying a volunteer any stipend may reclassify them as an employee, triggering withholding requirements

- The DOL allows "nominal fees" for volunteers, but fees that function as compensation substitutes don't qualify

- Paid employees cannot volunteer to perform the same type of work they're employed to do for the same organization

Interns occupy their own gray area. The DOL's primary beneficiary test evaluates whether an unpaid intern is receiving genuine educational benefit or simply replacing paid staff. Key distinctions:

- Unpaid internships are permissible when the intern receives clear educational benefit and has no expectation of pay

- Paid interns are employees — standard withholding, FICA, and minimum wage rules apply without exception

Document every volunteer and intern arrangement in writing.

Nonprofit Payroll Tax Obligations

Tax-exempt status does not mean payroll-exempt. All nonprofits with paid staff are required to withhold, match, and remit employment taxes the same way any for-profit employer would.

Federal Payroll Tax Requirements

For 2026, the key federal rates are:

| Tax | Employee Rate | Employer Rate | Wage Cap |

|---|---|---|---|

| Social Security | 6.2% | 6.2% | $184,500 |

| Medicare | 1.45% | 1.45% | No cap |

| Additional Medicare | 0.9% | Not matched | Over $200,000 |

One meaningful exception: 501(c)(3) organizations are exempt from FUTA — the Federal Unemployment Tax — and this exemption cannot be waived. For most nonprofits, this saves 6% on the first $7,000 of each employee's wages annually.

The personal liability risk here is real. Under the IRS Trust Fund Recovery Penalty, board members, officers, and anyone with authority over payroll can be held personally liable for unpaid withheld taxes. The IRS pursues individuals directly — not just the organization — when employment taxes go unremitted.

State and Local Tax Considerations

State obligations vary, but most nonprofits must address:

- State income tax withholding (in states with income tax)

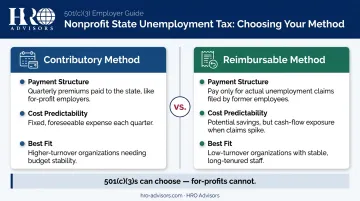

- State Unemployment Tax (SUTA) — with an important option for 501(c)(3)s

For SUTA, nonprofits can typically choose between two methods:

- Taxable (contributory) method — Pay quarterly premiums like a for-profit employer

- Reimbursable method — Pay the state only for actual unemployment claims filed by former employees

The reimbursable method can be more cost-effective for organizations with low turnover, but it creates cash-flow exposure when claims are filed. Organizations with stable, long-tenured staff often save money reimbursing directly; those with higher turnover typically fare better with the contributory method.

Form 990 and Compensation Reporting

Nonprofits must file IRS Form 990 annually, and the version depends on organizational size:

| Form | Gross Receipts | Total Assets |

|---|---|---|

| 990-N (e-Postcard) | $50,000 or less | — |

| 990-EZ | Under $200,000 | Under $500,000 |

| Full 990 | At or above those thresholds | — |

| 990-PF | Private foundations (all sizes) | — |

Form 990 discloses executive compensation publicly. All compensation must be "reasonable and not excessive" under IRS standards — excessive pay can trigger excise taxes under Section 4958 intermediate sanctions. Setting executive pay too high is a compliance risk; setting it too low is a retention risk. Benchmarking against compensation surveys for comparable organizations is the most defensible way to land in the right range.

Common Payroll Challenges Unique to Nonprofits

Nonprofits deal with all the standard employer headaches, plus several that are specific to how they're funded and staffed.

Worker misclassification is one of the more persistent risks. Nonprofits regularly work with contractors and volunteers alongside paid staff, and the IRS and DOL test worker status based on actual working conditions — not titles, intent, or what the volunteer agreement says. A program coordinator who shows up every week, follows internal procedures, and uses organization-owned equipment is probably an employee, regardless of what the paperwork calls them.

Grant-funded payroll tracking is a challenge most for-profit employers never face. When a salary is partially or fully funded by a grant, 2 CFR 200.430 requires that charges to federal awards be based on records that accurately reflect the work performed. Employees working across multiple grants need documented labor distribution records. Generic payroll systems that can't tag costs to specific funding sources create serious audit exposure.

Tight budgets create a third problem: compensation pressure. According to the 2023 National Council of Nonprofits Workforce Survey, 74.6% of nonprofits reported job vacancies, and 72.2% said salary competition directly affected their ability to recruit and retain staff. That turnover hits hardest in mission-critical roles where institutional knowledge is hard to replace.

The organizations most affected by turnover are also the ones least equipped to handle multi-state compliance. Each state has its own SUTA rules, income tax withholding requirements, and workers' compensation obligations — and nonprofits operating across state lines face layered requirements that even experienced HR staff can struggle to track. Smaller organizations often don't have dedicated HR staff at all, which makes this exposure particularly acute.

Understanding these challenges is the first step toward building a payroll structure that can actually hold up under them.

Best Practices for Nonprofit Payroll Management

Getting nonprofit payroll right comes down to consistent process and proper documentation. These three practices reduce audit risk and protect the organization when classifications or fund usage are questioned.

- Document every worker classification. Apply the IRS three-factor test before onboarding employees, contractors, or volunteers. Keep classification records indefinitely — if a decision is ever challenged, that paper trail is your primary defense.

- Tag salaries to grants at the point of entry. Payroll software with grant-tracking capability assigns labor costs to specific funding sources automatically, producing accurate distribution reports for auditors and grantors without manual reconciliation at year-end. Most platforms also support Form 990 compensation reporting.

- Keep payroll and program funds in separate accounts. A dedicated payroll bank account prevents grant-restricted dollars from commingling with general operating funds, speeds up audits, and demonstrates fiduciary responsibility to donors and grantors.

Should Your Nonprofit Partner with a PEO?

A Professional Employer Organization enters into a co-employment arrangement with your nonprofit, taking on payroll processing, tax filing, benefits administration, and HR compliance. Your organization retains full control over day-to-day operations, hiring decisions, and mission direction. The PEO handles the back-office operations underneath.

For nonprofits without dedicated HR staff, this matters in practice: instead of one person tracking SUTA elections, managing 990 compensation disclosures, and processing payroll across multiple states, those functions move to specialists.

The tangible benefits for nonprofits include:

- Access to health plans from carriers like Aetna, Blue Cross Blue Shield, and UnitedHealthcare — the same networks that cover Fortune 500 employees — through the PEO's group purchasing pool

- 403(b) retirement plan administration that would otherwise require a standalone plan with its own compliance burden

- Payroll tax compliance across all states where the nonprofit operates

- Worker classification guidance before problems arise

According to NAPEO, PEO clients see an average 27% ROI from cost savings alone — a meaningful figure for organizations where every dollar is accountable to donors and grant requirements.

That value depends entirely on finding the right match.

What works for a tech startup won't fit a community nonprofit with grant-funded staff and a volunteer program. HRO Advisors offers a free PEO matching service that compares up to 8 providers side-by-side, covering costs, compliance features, and benefits offerings.

The process takes under two weeks and costs nothing to the organization. HRO Advisors is compensated by the provider ultimately selected, with no markup to the client.

To start a comparison, contact HRO Advisors at 866-755-0288 or info@hro-advisors.com.

Frequently Asked Questions

Can a nonprofit have employees on payroll?

Yes. Nonprofits can and do employ paid staff. Tax-exempt status applies to the organization's income, not its employment obligations — nonprofits must withhold and remit payroll taxes just like any other employer.

What are the different positions in a nonprofit organization?

Common paid roles include executive directors, program managers, development and fundraising staff, administrative coordinators, and finance staff. Role structure varies by organization size, mission focus, and funding sources.

What are the 4 types of payroll systems?

The four main types are in-house manual processing, payroll software, outsourced payroll services, and PEO-managed payroll. For most nonprofits, outsourced or PEO-managed systems offer the best balance of compliance support and cost efficiency.

Do nonprofits have to pay FICA and other payroll taxes?

Yes. Nonprofits must withhold and match FICA taxes (Social Security and Medicare) for all employees. The one meaningful exception is FUTA — 501(c)(3) organizations are exempt from the Federal Unemployment Tax, which is not available to for-profit employers.

How are volunteers treated differently from employees for payroll purposes?

Genuine volunteers who work without any expectation of compensation are not employees and fall outside payroll requirements. Paying a stipend — even a small one — may trigger reclassification as an employee, creating withholding and tax obligations.

What is the most effective way for nonprofits to manage payroll compliance?

A combination of clear worker classification policies, payroll software with grant-tracking capability, and professional payroll or PEO support. Compliance errors carry both financial penalties and direct risk to the organization's tax-exempt status.