The result? Many employees at smaller companies go without meaningful retirement savings options, putting their employers at a disadvantage in a competitive labor market.

A PEO 401(k) changes that equation. By pooling multiple businesses into a single retirement plan, Professional Employer Organizations give smaller employers access to institutional-quality benefits at a fraction of the standalone cost — with most of the administrative and compliance burden shifted away from the employer.

This guide covers what PEO 401(k) plans are, how payroll integration works, the compliance advantages, and how to find the right PEO partner.

Key Takeaways

- PEO 401(k) plans pool multiple employers into one Multiple Employer Plan, reducing costs and administrative complexity

- 83% of workers say retirement benefits are a major factor in job decisions

- The 2026 employee 401(k) contribution limit is $24,500, far exceeding IRA limits

- Automated payroll integration eliminates manual data entry and prevents costly late-remittance penalties

- PEOs assume fiduciary responsibility, shifting legal liability away from the employer

What Is a PEO 401(k) Plan?

A PEO 401(k) is built on the co-employment model — where a Professional Employer Organization shares responsibility for payroll, HR administration, benefits, and compliance with a client business. The employer keeps full control over day-to-day operations and hiring; the PEO handles the infrastructure that makes retirement benefits possible.

Within this model, a PEO 401(k) is structured as a Multiple Employer Plan (MEP) or Pooled Employer Plan (PEP). Multiple unrelated businesses participate in a single, larger retirement plan — creating collective buying power that no individual small business could replicate on its own.

How This Differs From a Standalone Plan

When a business sets up its own 401(k), it becomes the plan sponsor. That means:

- Selecting and monitoring investment options

- Filing Form 5500 annually

- Conducting nondiscrimination testing

- Assuming full fiduciary liability for the plan

Under a PEO arrangement, the business does not sponsor its own plan. The PEO serves as plan sponsor and takes on these obligations, which changes the employer's risk exposure and administrative workload.

The DOL notes that PEPs were specifically designed to make 401(k)-type coverage more accessible to smaller employers that find traditional plan expenses and duties burdensome.

Key Benefits of PEO 401(k) Plans for Employers

Cost Savings Through Scale

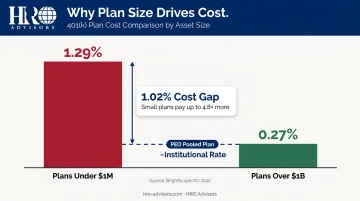

Small plans are expensive to run on a per-dollar basis. According to BrightScope/ICI 2022 data, plans with less than $1M in assets averaged 1.29% of assets in total plan costs, compared to 0.27% for plans exceeding $1 billion. That spread reflects the fixed-cost nature of plan administration, which falls hardest on smaller plans with fewer assets to absorb it.

Pooled plans address this directly. When a PEO aggregates dozens of client companies into one plan, those fixed costs spread across a much larger asset base, and the PEO gains negotiating leverage for institutional-class investment funds with lower expense ratios.

Reduced Administrative Burden

The PEO handles the tasks that require specialized expertise:

- Enrollment processing and employee communications

- Per-pay-cycle contribution calculations

- Annual nondiscrimination testing (ADP/ACP tests)

- Form 5500 filings

- IRS and DOL regulatory monitoring

For most small business owners, these aren't just time-consuming — they're genuinely complex. Handing them off to a PEO means less exposure to compliance risk and fewer internal resources tied up in plan management.

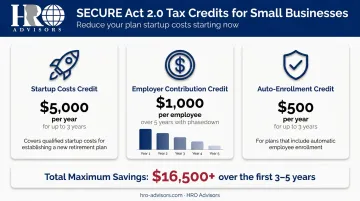

SECURE Act 2.0 Tax Credits

Eligible small businesses starting a new retirement plan can claim substantial tax credits. For employers with 1–50 employees:

- Startup costs credit: 100% of qualified startup costs, up to $5,000 annually, for the first three years

- Employer contribution credit: Up to $1,000 per employee for five years (100% in years 1–2, phasing down to 25% in year 5)

- Auto-enrollment credit: $500 per year for three years

Employers with 51–100 employees qualify for reduced versions of these credits. These incentives meaningfully offset the cost of launching a new plan through a PEO.

Talent Attraction and Retention

Retirement benefits have moved from "nice to have" to a genuine hiring factor. A 2024 Transamerica survey of 5,493 workers found that 83% said retirement benefits are a major factor in their final job decision. The same study found 82% of employers agree a 401(k) is critical for competing on talent.

For businesses competing with larger employers — particularly in financial services, technology, and manufacturing — offering a quality 401(k) through a PEO puts comparable retirement benefits within reach, without the administrative overhead of running a standalone plan.

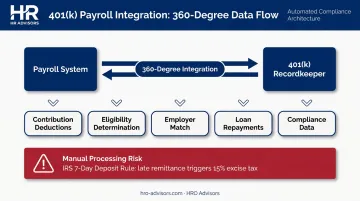

How PEO 401(k) Payroll Integration Works

What Integration Actually Means

401(k) payroll integration is the automated connection between a company's payroll system and its 401(k) recordkeeper. Instead of HR staff manually exporting spreadsheets after each pay run, an integrated system syncs contribution amounts, eligibility status, and loan repayment data automatically.

180-Degree vs. 360-Degree Integration

Not all integrations are equal:

| Integration Type | Data Flow | Limitation |

|---|---|---|

| 180-degree | Payroll → Recordkeeper (one-way) | Employee-initiated changes require manual updates |

| 360-degree | Bidirectional | Changes in either system sync automatically |

With 360-degree integration, when an employee updates their deferral rate through the recordkeeper's portal, that change flows directly back into payroll — no manual re-entry required. Most reputable PEOs offer 360-degree integration as their baseline, making it a key factor to evaluate when comparing providers.

What Gets Automated

A fully integrated system handles:

- Contribution deductions each pay cycle

- Eligibility determination based on hire date and hours worked

- Employer match calculations

- Loan repayment deductions

- Data collection for year-end compliance testing

Why Errors Are Costly

That automation matters because manual contribution processing carries real financial risk. The IRS requires small plans (under 100 participants) to deposit employee deferrals within 7 business days of withholding. Missing that window triggers a prohibited transaction — with an initial excise tax of 15% of the amount involved, escalating to 100% if uncorrected.

Integrated systems create timestamped audit trails and eliminate the data re-entry errors that trigger these penalties. For employees, real-time account visibility translates directly into higher plan participation — a measurable win for both staff and the business.

Compliance and Fiduciary Responsibilities in PEO 401(k) Plans

Running a standalone 401(k) plan puts real legal exposure on the business owner. A plan fiduciary must act in participants' best interests, select and monitor investments prudently, and maintain accurate records — and with a standalone plan, that liability falls entirely on the owner or a designated employee.

How the PEO Model Shifts the Burden

In a PEO MEP structure, the PEO typically serves as:

- 3(16) plan administrator — handles plan documentation, recordkeeping, and regulatory filings on behalf of the plan

- 3(38) investment manager — independently selects, monitors, and replaces investment options, removing that burden from the employer

This means the PEO — not the client business — is legally accountable for investment monitoring, Form 5500 filings, and nondiscrimination testing. For most small businesses, this transfer of liability represents one of the most significant advantages of the PEO model.

What the PEO Handles

- Annual ADP/ACP nondiscrimination testing

- Form 5500 preparation and filing

- Audit coordination for larger plans

- Ongoing monitoring for regulatory changes, including SECURE Act 2.0 updates

What the Employer Retains

The shift isn't total. Client employers remain responsible for:

- Ensuring their specific employee data is accurate and timely

- Communicating plan information and eligibility to their workforce

- Maintaining their own eligibility policies

A PEO arrangement significantly reduces fiduciary exposure — but employers who provide inaccurate data or fail to communicate plan details to employees still carry consequences for those gaps.

PEO 401(k) vs. Standalone 401(k): Key Differences

Choosing between the two models comes down to cost, control, and capacity.

| Factor | PEO 401(k) | Standalone 401(k) |

|---|---|---|

| Plan costs | Distributed across all participating employers | Borne entirely by the employer |

| Asset-based fees | Institutional rates via pooled scale | Higher rates for small plan balances (avg. 1.29% for plans under $1M) |

| Administrative work | PEO manages testing, filings, vendors | Employer manages all vendor relationships and filings |

| Fiduciary liability | PEO holds primary fiduciary responsibility | Employer assumes full fiduciary liability |

| Plan customization | Employer configures match, vesting, eligibility within PEO's master plan | Full employer control over all plan design elements |

That customization column often gives employers pause — but the trade-off is frequently overstated. Reputable PEOs still allow employers to configure matching formulas, vesting schedules, and eligibility requirements. What they don't allow is selecting entirely different investment platforms or third-party administrators; the employer works within the PEO's established plan framework.

For businesses with fewer than 100 employees — where plan balances rarely exceed $1M — the fee savings from pooled institutional pricing alone can more than offset any reduction in plan design flexibility.

How to Choose a PEO with the Right 401(k) Services

Evaluation Criteria

When assessing a PEO's 401(k) offering, focus on:

- Payroll integration depth — confirm 360-degree (bidirectional) integration, not just one-way file transfers

- Fee transparency — ask for all-in costs including investment fund expense ratios, not just administrative fees

- Fiduciary coverage — clarify whether the PEO holds 3(16) and 3(38) fiduciary responsibility in writing

- Investment menu quality — look for diversified options including index funds and target-date funds

- Verify that employee enrollment tools include self-service access, financial wellness resources, and multilingual materials — these directly drive participation rates

- Confirm the plan structure can scale with your headcount without requiring a full plan migration

Red Flags to Watch For

- Hidden fees not disclosed upfront (administration charges buried in fund expense ratios)

- Vague fiduciary language — if it's not clearly documented, assume the liability stays with you

- No true payroll integration, requiring manual file uploads each pay period

- A thin investment menu that doesn't serve employees across different income levels and risk tolerances

Where HRO Advisors Fits In

HRO Advisors operates as a free PEO broker that runs this evaluation for you — comparing up to 8 providers side-by-side on cost structures, payroll integration capabilities, and retirement plan options.

Here's how the process works:

- Free consultation — no obligation; HRO Advisors collects details on your workforce, budget, and compliance needs

- Market analysis — advisors analyze coverage across 500+ PEO providers and narrow to 3–8 best-fit options

- Side-by-side comparison — delivered in under two weeks, covering costs, benefits, and service capabilities

- Advisors then negotiate directly with providers on your behalf, leveraging broker relationships that individual businesses typically can't access independently

The provider you select pays HRO Advisors — your business pays nothing, and there's no incentive to favor one provider over another. If 401(k)-specific features like employer matching structures or vesting schedules matter to you, flag those in the initial consultation so they're weighted in the comparison.

To get started, call 866-755-0288 or email info@hro-advisors.com.

Frequently Asked Questions

What is 401(k) payroll integration?

Payroll integration is the automated connection between your payroll system and your 401(k) recordkeeper, syncing contribution amounts, eligibility data, and plan changes in real time. This eliminates manual data entry, reduces errors, and ensures contributions are deposited on time to avoid IRS penalties.

What are Professional Employer Organization services?

A PEO enters a co-employment relationship with your business, taking on shared responsibility for payroll, benefits, compliance, and HR administration. You retain control over daily operations while the PEO handles the administrative infrastructure, giving small businesses access to enterprise-level HR resources.

How does a PEO 401(k) differ from a standalone plan?

A PEO 401(k) pools multiple employers into a single Multiple Employer Plan, which lowers costs and shifts administrative and fiduciary responsibilities to the PEO. A standalone plan requires the employer to manage setup, compliance, filings, and vendor relationships.

Can small businesses access quality 401(k) plans through a PEO?

Yes — this is one of the primary advantages. PEOs provide access to institutional-quality retirement plans with lower expense ratios and broader investment options that would typically only be available to large corporations with substantial plan assets.

Who is responsible for 401(k) compliance when using a PEO?

The PEO typically holds primary fiduciary and compliance responsibility, including Form 5500 filings and nondiscrimination testing. The client employer remains responsible for providing accurate employee data and communicating plan details to their workforce.