The challenge isn't simply offering coverage — it's the gap between offering a plan and offering a competitive one. That gap is determined by contribution levels, plan variety, network quality, and how well your benefits strategy actually fits your workforce. Get those wrong, and you've spent significant money on a benefit that doesn't move the needle on hiring or retention.

This guide walks through exactly how to build, structure, and maintain a group health plan that employees value — and that your business can sustain.

Key Takeaways

- Employer contribution levels — not just premium cost — determine whether your plan is actually competitive

- Offering at least two plan types dramatically improves employee satisfaction across different life stages

- Self-funded plans, PEO partnerships, and HDHP/HSA combinations are the main cost-control levers for most employers

- ACA, COBRA, and HIPAA obligations require year-round management, not just attention at open enrollment

- Annual benchmarking prevents gradual cost creep and keeps your plan aligned with market expectations

Steps to Offer a Competitive Group Health Plan

Step 1: Assess Your Workforce's Healthcare Needs

Plan competitiveness is workforce-specific. A 30-person company where most employees are young and single has very different healthcare priorities than a 200-person operation with a mix of families, older workers, and employees managing chronic conditions.

Before talking to a single carrier, take inventory of your workforce:

- Age distribution — younger workforces often prioritize lower premiums; older ones value lower out-of-pocket costs and specialist access

- Family status — a high proportion of employees with dependents signals that family premium contributions matter significantly

- Income levels — lower-wage employees are more price-sensitive; KFF data shows take-up drops to 65% at firms with many lower-wage workers versus 77% at others

- Healthcare utilization — if your workforce skews toward employees with ongoing prescriptions or specialist needs, network depth and drug coverage become priorities

Beyond demographics, ask directly. A short employee survey before your next renewal — asking about prescription coverage, mental health access, telehealth preferences, and specialist needs — gives you real data rather than assumptions. That input should drive your carrier conversations, not follow them.

Step 2: Choose the Right Plan Type(s) for Your Group

The four plan structures most commonly offered by employers each carry different cost and flexibility trade-offs:

| Plan Type | 2025 Avg. Single Premium | Key Trade-Off |

|---|---|---|

| PPO | $9,818/year | Most provider flexibility; highest premiums |

| HDHP/HSA | $8,620/year | Lower premiums; higher deductibles; pairs with HSA |

| HMO | Lower than PPO | Requires PCP referrals; narrower network |

| POS | Varies | Hybrid of HMO and PPO features |

PPOs remain the most common choice — 46% of covered workers are enrolled in one — but HDHPs have grown steadily and now cover 33% of workers, largely because of their pairing with tax-advantaged HSAs.

The stronger strategy isn't picking one and imposing it on everyone. Offer at least two tiers. A lower-cost HDHP option alongside a mid-tier PPO accommodates employees at different life stages and income levels without forcing anyone into a plan that doesn't fit. Note that carrier availability and plan types vary by state and employee count, so your options will depend on where your workforce is located.

Step 3: Determine Your Employer Contribution Strategy

Your contribution percentage often determines whether a plan is actually competitive. An excellent plan employees can't afford to use does nothing for retention or recruitment.

The 2025 national benchmarks, per KFF:

- Single coverage: Employers contribute ~84% of the average $9,325 annual premium; employees pay ~$1,440

- Family coverage: Employers contribute ~75% of the average $26,993 annual premium; employees pay ~$6,850

These figures are your competitive baseline. Falling meaningfully below them — particularly on single coverage — puts you at a disadvantage in markets where candidates are comparing offers side-by-side.

Two decisions carry the most strategic weight:

- Employee-only vs. dependent contributions — Many employers cover a strong share of the employee premium but contribute little or nothing toward dependent coverage. Family premiums averaging nearly $27,000/year mean that even a modest employer contribution toward dependents significantly changes the plan's perceived value.

- Consistent contribution floors — Setting contribution levels too low at launch creates a compounding problem at renewal. With premium increases of 5% for single and 6% for family coverage in 2025 alone, a thin starting baseline erodes faster than most employers anticipate.

Step 4: Set Up Enrollment and Ongoing Administration

Administering the plan correctly after launch is where many employers run into trouble. Coverage gaps and compliance penalties typically trace back to process failures, not plan design.

Core administrative responsibilities include:

- Select a carrier or benefits administration platform before your coverage start date

- Set open enrollment windows and new-hire enrollment periods in writing

- Manage payroll deductions accurately and reconcile them monthly

- Track eligibility changes as they happen — new hires, terminations, life events, and dependent status updates

Ongoing compliance obligations that must be managed year-round:

- ACA reporting — Applicable Large Employers (50+ full-time equivalents) must file Forms 1094-C and 1095-C; for 2025 coverage, the furnish deadline was March 2, 2026, with electronic filing required for 10+ returns

- COBRA — Applies to employers with 20+ employees; qualifying events trigger 18–36 months of continuation coverage rights; former employees may be charged up to 102% of plan cost

- HIPAA — The Privacy Rule applies to employer-sponsored group health plans; data handling protocols must be in place

- State continuation laws — Several states have continuation coverage requirements that go beyond federal COBRA

What Makes a Group Health Plan Truly Competitive

A group health plan is competitive when it holds up against what peer employers in your industry and region are actually offering — not just what feels adequate from the inside.

Network and Coverage Depth

A plan's network quality shapes how employees experience their coverage daily. Narrow networks cost less but create friction when workers discover their doctor isn't included or a preferred hospital is out-of-network. Restricting access to specialists, mental health providers, or major local health systems will feel subpar regardless of how competitive the premium looks on paper.

On coverage content, the baseline expectation has risen significantly. Employees now expect:

- Prescription drug benefits (large-employer drug spending rose 9.4% in 2025)

- Mental health and substance use disorder benefits at parity with medical/surgical coverage

- Preventive care with no cost-sharing

- Telehealth access — 30% of firms with 50+ employees now have virtual primary care contracts, rising to 45% among firms with 1,000+ workers

Plans missing any of these don't read as lean — they read as behind.

Savings Tools That Add Tangible Value

HSAs, FSAs, and HRAs extend a plan's value by reducing employees' out-of-pocket burden:

- 61% of employers offered an HSA in 2025; average employer HSA contributions were ~$1,059 for individuals and $1,735 for families

- 60% of employers offered a medical FSA

- 14% offered an HRA

Even a modest employer HSA seed contribution — say, $500 toward a $1,500 individual deductible — materially changes how employees perceive an HDHP. It's not just a lower-premium option; it becomes a plan with real employer backing.

Ancillary Benefits Round Out the Package

Savings tools strengthen the core plan, but ancillary benefits determine the full picture employees see. Dental, vision, life insurance, short- and long-term disability, and voluntary options are what separate a true benefits package from a single line-item health plan. Employees evaluate total compensation, and a strong core health plan paired with a well-rounded ancillary suite signals genuine investment in their wellbeing — not just the compliance minimum.

What You Need Before Getting Started

Three things should be in place before you approach a carrier or PEO.

Minimum Group Requirements

- Most carriers require at least two enrolled employees to issue a group plan

- Participation thresholds — typically 50%–75% of eligible employees — apply in many states, with exact percentages varying by carrier

- Part-time and contractor classifications can affect your eligible employee count, so confirm headcount definitions before shopping

Budget Baseline

- Determine what percentage of premiums your business can realistically sustain — not just at launch, but through annual renewals

- Family premiums have risen 26% since 2020; setting too tight a contribution floor early puts you in a weaker position at each renewal

Compliance Readiness

- Confirm whether your business qualifies as an Applicable Large Employer (50+ full-time equivalents triggers mandatory ACA coverage obligations)

- Check state-specific insurance mandates in every state where you operate

- Resolve workforce classification questions — part-time and contractor status determines who must be offered coverage under the ACA

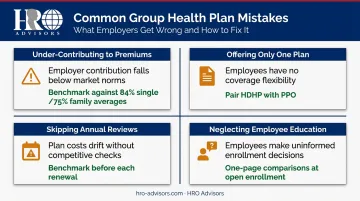

Common Mistakes When Offering Group Health Plans

Under-contributing to premiums. 48% of workers say greater employer financial contributions would most improve their benefits — and a plan employees avoid because cost-sharing is too high delivers almost no retention value, even if it technically exists.

Offering only one plan. A 22-year-old with no dependents and a 45-year-old parent of three need different coverage. Yet 66% of offering firms provide just one plan type, while 63% of large firms offer multiple plan types — and employees at those firms report higher satisfaction with their benefits. Pairing a value HDHP with a mid-tier PPO covers the most common divergence in employee needs without a major jump in administrative complexity.

Skipping annual reviews. Premiums are rising 5–6% per year in 2025, and auto-renewing without benchmarking means absorbing those increases without knowing whether better options exist. A plan competitive two years ago may no longer align with market rates or your workforce's actual utilization. Comparing current costs against new carrier options before each renewal is the only reliable way to catch that drift.

Neglecting employee education. A good plan still underperforms if employees don't understand it. Workers who can't explain the difference between their deductible and out-of-pocket maximum — or don't know their HDHP pairs with a tax-free HSA — aren't capturing the value you're paying for. One-page plan comparisons and short explainer sessions at open enrollment directly improve how employees rate their benefits.

How to Reduce Costs Without Compromising Plan Quality

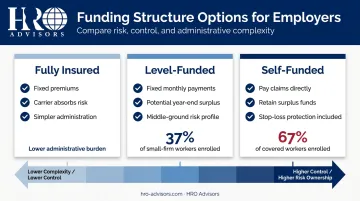

Self-Funded and Level-Funded Structures

Self-funded plans allow employers to pay claims directly rather than fixed premiums, keeping surplus funds when claims run below projections. 67% of covered workers are in self-funded plans nationally, though adoption skews heavily by size: 80% at large firms versus 27% at small firms.

Stop-loss insurance makes self-funding workable for smaller organizations — it caps the employer's claims exposure per individual (commonly at thresholds between $250,000–$1,000,000) and limits aggregate annual claims (often at 125% of expected costs). Level-funded plans — where 37% of covered workers at small firms are enrolled — offer a middle ground: fixed monthly payments with the potential to recover surplus at year-end.

HDHP + HSA: Lower Premiums Without Gutting the Plan

Pairing an HDHP with employer-seeded HSA contributions is one of the most effective cost-control strategies available. Each party benefits in a distinct way:

- Employer pays lower monthly premiums, reducing fixed benefit spend

- Employee receives a tax-advantaged account they own and carry forward year to year

- HSA seed contribution — even a modest one — offsets deductible exposure without the commitment of higher monthly premiums

The total cost picture is often more favorable than it looks when you're only comparing premium lines.

PEO Partnerships for Small and Mid-Sized Employers

For small and mid-sized businesses, the most direct path to large-group plan quality is joining a Professional Employer Organization. NAPEO data shows the PEO industry serves 230,000+ clients — businesses that collectively access group pricing, compliance infrastructure, and carrier relationships they couldn't secure independently.

HRO Advisors specializes in connecting businesses with the right PEO match. Their free comparison service evaluates 3–8 PEO providers side-by-side — drawing from a network of 500+ providers — analyzing health plan quality, carrier partnerships (including Aetna, Blue Cross Blue Shield, and UnitedHealthcare), compliance capabilities, and cost structures. The comparison is tailored to your specific workforce and industry, not a generic overview, and the process is typically completed in under two weeks. HRO Advisors is compensated by the selected provider, so there's no cost to you as the employer.

Annual Carrier Benchmarking

PEO partnerships and carrier benchmarking work together — one expands your access, the other keeps you from overpaying once you're enrolled. Auto-renewal costs employers more than they realize. Shopping the market before each renewal — whether through a broker, PEO advisor, or direct carrier comparison — keeps your plan competitively priced and maintains negotiation leverage. Engage an advisor before renewal, not after you've signed. That timing is the only way to capture the window.

Frequently Asked Questions

Who may be covered under a group health plan?

Group health plans typically cover eligible employees as defined by the employer and the plan. Employees may also add spouses, domestic partners, and dependent children — up to age 26 under ACA rules — for an additional premium. COBRA allows former employees to continue coverage temporarily after qualifying events such as job loss, reduced hours, or loss of dependent status.

What is a competitive benefits package?

A competitive benefits package compares favorably to what peer employers in the same industry and region offer. It's built around comprehensive health insurance but also includes retirement plans, paid time off, and ancillary benefits like dental and vision that make the total compensation package attractive to both candidates and current employees.

How much should an employer contribute to group health insurance premiums?

There's no universal federal minimum contribution percentage, but KFF's 2025 benchmarks show employers covering roughly 84% of single premiums and 75% of family premiums on average. Employers who contribute meaningfully to both employee-only and family coverage are consistently viewed as more competitive in the talent market.

How many employees do you need to offer group health insurance?

Most carriers require a minimum of two enrolled employees to issue a group health plan. Participation thresholds — requiring 50%–75% of eligible workers to enroll — also apply in many states, though requirements vary by carrier and state.

Can small businesses offer competitive group health plans without breaking the budget?

Yes — by joining a PEO, small businesses gain access to large-group insurance pools and enterprise-grade plan options at rates unavailable to standalone employers. HRO Advisors helps small and mid-sized businesses compare PEO options at no cost to identify the best health plan access and pricing for their specific workforce.

What is the difference between an HMO and a PPO in a group health plan?

HMOs require employees to choose a primary care physician and get referrals for specialists, typically at lower premiums and out-of-pocket costs. PPOs offer more provider flexibility with no referral requirement but come with higher premiums. The right choice depends on your workforce's preferences and your budget constraints.

Offering a competitive group health plan comes down to three things: how much you contribute, how well the plan fits your workforce, and whether you review it seriously each year. Employers who treat benefits as a recurring strategic decision — rather than a one-time setup — consistently outperform those who don't on both retention and recruitment.

Businesses of any size can access competitive group health coverage today — through self-funded structures, HDHP/HSA combinations, or PEO partnerships that unlock large-group pricing. HRO Advisors offers free, no-obligation comparisons across leading PEOs so you can identify the right fit for your workforce and budget without the guesswork.