Introduction

Group health insurance has become genuinely difficult for small businesses to sustain. According to the 2025 KFF Employer Health Benefits Survey, average annual premiums hit $9,325 for single coverage and $26,993 for family coverage — with family premiums rising 6% in a single year. Among small firms that don't offer benefits at all, 41% cite cost as the primary barrier.

Participation minimums add another layer of friction. SHOP marketplace rules require 70% employee enrollment to keep a group plan in force — a threshold that becomes nearly impossible to hit with part-time, seasonal, or geographically distributed staff.

Individual Coverage Health Reimbursement Arrangements (ICHRAs) cut through both problems. Employers set a fixed monthly allowance, employees purchase their own qualifying individual health plans, and reimbursements flow tax-free — with no renewal surprises, no participation floors, and no single plan forced on a diverse workforce.

This guide covers how ICHRA works in 2026, why it fits small businesses particularly well, the real trade-offs, how it compares to group plans and QSEHRA, and the steps to get started.

Key Takeaways

- ICHRA caps your health benefits spend at whatever allowance you set — unused funds stay with you

- No minimum participation requirements, unlike group plans requiring 70%+ enrollment

- Employees get a 60-day special enrollment period when you launch, making mid-year starts feasible

- Reimbursements are tax-deductible for employers and tax-free for employees

- Small employers under 50 employees face no ACA mandate, though affordability rules still affect employee subsidy access

What Is ICHRA and How Does It Work?

ICHRA is an employer-funded benefit that reimburses employees tax-free for individual health insurance premiums and qualified medical expenses. Instead of the employer purchasing a group plan, each employee buys their own coverage in the individual market and submits reimbursement requests.

Here's how the process works in practice:

- Employer sets a monthly allowance — by employee class, age, and family size

- Employee enrolls in a qualifying individual health plan — on or off the Marketplace

- Employee submits proof of coverage and expense receipts

- Employer reimburses up to the allowance amount, tax-free

This structure was created by the June 2019 federal final rule (84 Fed. Reg. 28888), making ICHRAs available to employers starting January 1, 2020.

What Counts as a Qualifying Health Plan

Plans that qualify for ICHRA reimbursement:

- ACA-compliant individual and family market plans (on- or off-exchange)

- Medicare Parts A+B or Part C

- Catastrophic plans (for those under 30 or with a qualifying hardship/exemption)

- Student health insurance coverage

Plans that do NOT qualify:

- Short-term limited-duration insurance

- Health care sharing ministries

- A spouse's employer group health plan

- Fixed indemnity plans (considered excepted benefits)

Three Reimbursement Options Employers Can Choose

Employers pick one of three structures when designing their ICHRA:

- Premiums only — reimburse individual health plan premiums exclusively

- Premiums plus qualified medical expenses — premiums plus out-of-pocket costs defined under IRS Publication 502

- Qualified medical expenses only — no premium reimbursement, expenses only

Most small businesses choose option 1 or 2. Option 3 works best when employees already have coverage through a spouse and only need help with out-of-pocket costs.

When you offer an ICHRA, employees receive a 60-day special enrollment period to purchase a qualifying plan outside of standard open enrollment windows — so mid-year launches work without waiting for the next enrollment cycle.

Why ICHRA Is a Smart Benefits Strategy for Small Businesses in 2026

Predictable, Fixed Healthcare Costs

With traditional group insurance, a bad claims year flows directly into your next renewal. Premiums rise unpredictably, and there's little you can do about it. Aon projects employer-sponsored health care costs increased roughly 9% in 2025, surpassing $16,000 per employee on average.

ICHRA flips that model. Your monthly allowance is your maximum spend — if an employee doesn't use it, you keep the difference. That eliminates:

- Surprise renewals driven by claims history

- Mid-year premium adjustments

- Actuarial uncertainty baked into your annual budget

No Minimum Participation Requirements

SHOP marketplace plans require at least 70% of eligible employees to enroll for the plan to remain in force. For businesses with part-time staff, seasonal workers, or employees who already have coverage through a spouse, hitting that threshold is a constant pressure point.

ICHRA has zero participation requirements. Each employee independently decides whether to enroll. One employee opting out has no effect on anyone else's coverage or the plan's viability.

Purpose-Built for Distributed and Mixed Workforces

ICHRA is particularly effective for businesses with employees across multiple states. Each employee shops for a plan in their local market — which means better network fit and typically lower premiums than a nationwide group plan requires.

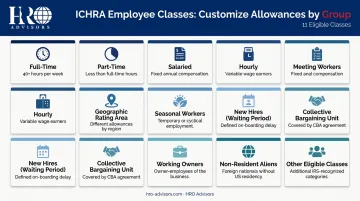

The employee class structure adds another layer of flexibility. Employers can differentiate allowances across up to 11 distinct employee classes, including:

- Full-time vs. part-time

- Salaried vs. hourly

- Employees by geographic rating area

- Seasonal workers

- New hires (during waiting periods)

This makes ICHRA well-suited for businesses mixing employment types — a structural flexibility no group plan can match. The tax treatment reinforces that advantage on both sides of the transaction.

Meaningful Tax Advantages for Both Sides

- Employers: Reimbursements are 100% tax-deductible as a business expense and exempt from FICA payroll taxes

- Employees: Reimbursements are excluded from gross income — no federal income tax, no employment tax

At the state level, Indiana has enacted an HRA/ICHRA tax credit for employers with fewer than 50 employees — up to $400 per covered employee in year one and $200 in year two, subject to a statewide cap. Mississippi and Ohio have introduced similar legislation, though their enacted status should be confirmed before factoring them into planning.

Allowance amounts can also vary by age (up to a 3:1 ratio from youngest to oldest) and by number of dependents. That flexibility helps employers ensure older workers receive adequate coverage without pushing total costs out of range.

Pros and Cons of ICHRA for Small Business Owners

The Real Advantages

Three outcomes stand out for small businesses:

- Total cost predictability — your allowance is a ceiling, not a floor. No renewal spikes, no actuarial surprises

- No participation floor — hire part-time or seasonal staff without worrying about dropping below enrollment minimums

- Employee plan ownership — employees choose their own insurer, network, and provider relationships rather than inheriting whatever the employer selected

The Honest Trade-Offs

ICHRA isn't the right fit for every situation. The three most common limitations:

- Network type — individual market plans lean heavily toward HMO and EPO structures. Employees with established specialist relationships may find out-of-network care limited compared to the PPOs typical in group plans

- Age-rated premiums — older employees face meaningfully higher individual market premiums. If you don't vary allowances by age, older workers may find their out-of-pocket costs significantly higher than younger colleagues

- Subsidy interaction — employees who receive an affordable ICHRA offer lose access to ACA premium tax credits in the Marketplace, even if they decline the ICHRA. This requires careful communication, particularly for lower-wage employees who might otherwise qualify for substantial subsidies

ICHRA Affordability and the ACA: What Small Businesses Need to Know

An ICHRA is considered affordable under ACA rules when the employee's remaining cost for the lowest-cost Silver plan in their area does not exceed 9.96% of household income — the confirmed 2026 threshold per IRS Rev. Proc. 2025-25.

Businesses with fewer than 50 full-time equivalent employees are not subject to the ACA employer shared responsibility mandate. Affordability still matters, though. If your ICHRA is affordable, employees cannot access Marketplace premium tax credits. If it's unaffordable, they can choose between accepting the ICHRA or declining it to claim subsidies instead.

Key compliance obligations every employer must meet:

- Formal ERISA written plan document

- Summary Plan Description (SPD)

- Employee notice delivered at least 90 days before the plan year begins

- HIPAA-compliant claim substantiation — medical receipts are Protected Health Information (PHI)

- IRS reporting via Forms 1094-C/1095-C (for applicable large employers)

Self-administering claims substantiation creates real HIPAA exposure. Most small businesses work with a third-party ICHRA administrator specifically to handle PHI-compliant reimbursement processing and avoid that liability.

ICHRA vs. Your Other Options: Group Plans and QSEHRA

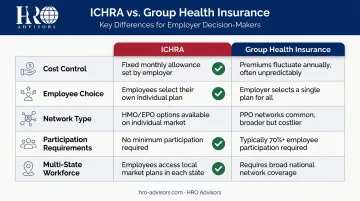

ICHRA vs. Traditional Group Health Insurance

| Factor | ICHRA | Group Health Insurance |

|---|---|---|

| Cost control | Fixed allowance — employer sets the ceiling | Premiums fluctuate at renewal |

| Employee choice | Employee selects their own plan | Employer chooses for everyone |

| Network breadth | HMO/EPO dominant | PPOs more common |

| Participation requirements | None | Typically 70%+ enrollment required |

| Multi-state workforce | Employees buy local market plans | Requires broad national network |

When group insurance still makes sense: Your team relies on specific specialists within established PPO networks, or your workforce is stable and values continuity with existing provider relationships.

ICHRA vs. QSEHRA

Both are HRA structures, but the differences matter depending on your workforce:

| Factor | ICHRA | QSEHRA |

|---|---|---|

| Employer size limit | No upper limit | Under 50 employees only |

| 2026 contribution caps | No federal cap | $6,450 self-only / $13,100 family |

| Employee class differentiation | 11 classes allowed | Same benefit for all eligible employees |

| Spouse's group plan reimbursement | Not permitted | Permitted |

Choose ICHRA if you want design flexibility, no contribution caps, and the ability to offer differentiated tiers by employee class. Choose QSEHRA if you prefer uniform contributions and need to accommodate employees on a spouse's employer plan — it's simpler to administer for smaller, more homogeneous teams.

Who Is Eligible for ICHRA?

Which Business Structures Can Offer ICHRA

Any employer with at least one W-2 employee can establish an ICHRA. There's no size ceiling. Entity type determines which participants can receive tax-free benefits:

- C corporations (including LLCs taxed as C corps): All W-2 employees, including owner-employees, qualify for tax-free reimbursements

- S corporations: Non-owner W-2 employees qualify; shareholders owning more than 2% cannot participate tax-free per IRS guidance

- Partnerships: Partners are not W-2 employees and cannot participate tax-free

- Sole proprietors: The owner cannot participate (not a W-2 employee), but any W-2 employees they hire can

What Employees Need to Enroll and Participate

Employees must:

- Enroll in a qualifying individual health plan providing minimum essential coverage before receiving reimbursements

- Submit proof of coverage along with expense receipts

- Receive a 60-day special enrollment period upon an ICHRA offer

- Opt out annually if the ICHRA is unaffordable and Marketplace subsidies would provide greater value

Medicare-eligible employees can use ICHRA allowances to reimburse Medicare Parts A, B, C, D, and Medigap premiums. This makes ICHRA practical for teams that include employees on Medicare alongside younger workers on individual plans.

How to Set Up an ICHRA for Your Small Business in 2026

Step 1 — Design Your Plan Structure

Core decisions to make before anything else:

- Start date — ICHRA can launch any time of year, not just January 1

- Employee classes — which classes will receive ICHRA, which (if any) will remain on a group plan

- Monthly allowance amounts — by class, with optional age and family size variations

- Reimbursement scope — premiums only, or premiums plus qualified medical expenses

Before finalizing allowances, research average individual market Silver plan premiums in every geographic area where your employees live. Allowances set without benchmarking local costs often leave employees underserved or make the ICHRA technically unaffordable under ACA rules.

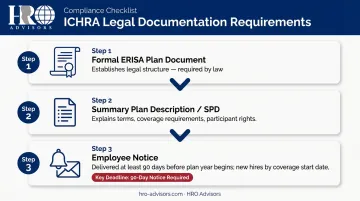

Step 2 — Create Required Legal Documentation

Three documents are required before the plan can operate:

- Formal ERISA plan document — required by law; establishes the plan's legal structure

- Summary Plan Description (SPD) — explains plan terms, coverage requirements, and participant rights

- Employee notice — must be delivered at least 90 days before the plan year begins for existing employees; no later than the date coverage could begin for new hires

The employee notice must include: allowance amount, coverage requirements, exclusion of non-qualifying plans, opt-out rights, consequences for premium tax credit eligibility, substantiation requirements, and SEP availability.

Failure to deliver proper documentation creates IRS penalty exposure and ERISA liability. Getting documentation right from day one is non-negotiable — which is why many small businesses work with a benefits advisor or ICHRA administrator who handles this as part of their setup process. HRO Advisors can connect you with providers that bundle ICHRA administration alongside broader HR support, so compliance obligations don't fall entirely on your internal team.

Step 3 — Communicate, Launch, and Administer

Employee communication priorities at launch:

- Explain what an ICHRA is and how the allowance works in plain language

- Walk through how to use the 60-day special enrollment period to find a qualifying plan

- Clarify exactly how to submit reimbursement requests and what documentation is required

- Do not direct employees toward a specific plan — federal rules prohibit this

For ongoing administration, a third-party ICHRA administrator handles claim substantiation, reimbursement processing, HIPAA-compliant recordkeeping, and IRS reporting. For most small businesses, the administrator fee runs $5–$15 per employee per month — a fraction of what in-house management would cost, and it keeps medical claim data properly walled off from general HR functions as HIPAA requires.

Frequently Asked Questions

Can a small business offer ICHRA and a group health plan at the same time?

Yes — but not to the same class of employees. Employers can offer ICHRA to part-time workers while maintaining a group plan for full-time staff, for example. When mixing the two, minimum class-size rules apply: generally 10 employees for employers with fewer than 100 workers.

What happens to an employee's ICHRA allowance if they leave the company?

Reimbursements stop when employment ends. The employee keeps their individual health insurance plan, since they purchased it directly and it isn't tied to the employer. They'll need to cover the premiums themselves going forward.

Do employees lose their ACA premium tax credits if their employer offers an ICHRA?

If the ICHRA is considered affordable under the 9.96% threshold, yes — the employee cannot access Marketplace subsidies even if they decline the ICHRA. If the ICHRA is unaffordable, they can choose between accepting it or declining it to claim subsidies instead.

How much should a small business contribute to an ICHRA in 2026?

There are no IRS-mandated minimums or maximums. Research the cost of a Silver plan in each location where employees live, then set allowances that cover a meaningful portion of that benchmark premium. Adjust upward for older employees using the 3:1 age ratio.

Is ICHRA better than QSEHRA for small businesses under 50 employees?

ICHRA is the stronger choice for employers wanting design flexibility, no contribution caps, and differentiated tiers by employee class. QSEHRA is the simpler choice if uniform contributions and compatibility with spousal group coverage are priorities.

What are the main compliance requirements for offering an ICHRA?

Formal ERISA plan documents, an SPD, and employee notices 90 days before the plan year are required. Ongoing administration also requires HIPAA-compliant claim substantiation, which most small businesses handle through a third-party administrator to avoid privacy and compliance risk.