A Certified Professional Employer Organization (CPEO) is a specific IRS designation established in 2014, not a self-awarded marketing title. This guide covers exactly what CPEO status means, how it differs from a standard PEO, what the IRS requires to earn it, and — critically — where its protections end.

Key Takeaways

- A CPEO is voluntarily certified by the IRS under IRC Section 3511, making the CPEO solely liable for federal employment taxes on covered wages

- With a non-certified PEO, both the client and the PEO can be held liable for unpaid payroll taxes — a significant financial exposure

- CPEO certification requires audited financials, background checks, a surety bond, and ongoing IRS compliance reviews

- Clients of CPEOs retain key federal tax credits, including the R&D credit, WOTC, and the small-employer health insurance credit

- CPEO status is rare — and a high-quality non-certified PEO with ESAC accreditation can offer comparable protections for many businesses

What Is a Certified PEO (CPEO)?

A CPEO is a Professional Employer Organization that has been voluntarily certified by the IRS under the program created by the Small Business Efficiency Act (SBEA), enacted as part of the Tax Increase Prevention Act of 2014. This was the first federal recognition of PEO services in U.S. history.

How the Co-Employment Model Works

PEOs operate on a co-employment structure:

- The business owner remains the "common law employer" — responsible for day-to-day management, hiring decisions, and business operations

- The PEO becomes the "employer of record" — handling payroll processing, tax filings, benefits administration, and HR compliance

- Both parties share employer responsibilities, but the division of those responsibilities depends heavily on whether the PEO is certified

What Certification Actually Means

CPEO certification is entirely voluntary. Not every PEO pursues it, and the IRS does not endorse CPEOs or recommend them over non-certified providers.

Earning the designation requires passing a rigorous series of financial, background, and compliance assessments. That signals accountability and operational transparency — but it does not mean the IRS endorses the provider.

The IRS maintains the CPEO Public Listings page as the only authoritative source for verifying whether a PEO is currently certified, previously certified, or has had its certification revoked.

According to NAPEO, more than 500 PEOs operate in the U.S., serving over 230,000 client businesses and approximately 4.5 million worksite employees. The CPEO designation remains relatively uncommon within that total — making it a meaningful differentiator when evaluating providers.

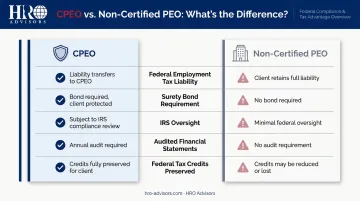

CPEO vs. Non-Certified PEO: Key Differences

When comparing CPEOs to non-certified PEOs, the critical distinction comes down to federal tax liability — not service quality.

The Sole Employer Rule Under IRC Section 3511

Under 26 USC § 3511, a CPEO is treated as the employer — and no other person is treated as employer — for covered worksite employees with respect to federal employment taxes on wages the CPEO remits. This is the legal foundation of CPEO status.

With a non-certified PEO, the IRS takes a different position: the common law employer is generally not relieved of employment tax obligations simply by using a PEO. That means if the PEO fails to remit payroll taxes, the IRS can pursue the client business for the unpaid amount — plus penalties and interest — even if the client already paid the PEO in full.

Comparison at a Glance

| Feature | CPEO | Non-Certified PEO |

|---|---|---|

| Federal employment tax liability | CPEO bears sole liability | Client and PEO may both be liable |

| Surety bond required | Yes (up to $1M) | No federal requirement |

| IRS oversight | Ongoing | None at federal level |

| Audited financial statements | Required annually | Not required by IRS |

| Federal tax credits preserved | Yes, per IRC § 3511(d) | Not guaranteed |

A Note on the Paychex Case

Paychex Business Solutions, LLC v. United States (2017) addressed wage-base treatment when switching PEOs mid-year. However, the IRS issued a nonacquiescence in AOD 2020-01 — meaning it does not accept that court's conclusions as settled law. Businesses switching PEOs mid-year, certified or not, should consult a tax advisor rather than rely on this case as established IRS policy.

IRS Requirements for CPEO Certification

The requirements to earn and maintain CPEO status are substantial. Here's what the IRS mandates:

Initial Eligibility Requirements

- Must be a business entity with at least one physical U.S. location where PEO functions are performed

- Must demonstrate a history of financial responsibility, organizational integrity, and compliance with federal, state, and local taxes

- Responsible individuals must be majority U.S. citizens or residents with knowledge of employment tax compliance

- Must submit fingerprinting and background checks for all responsible individuals

Financial and Documentation Requirements

- Audited annual financial statements prepared by a licensed CPA, confirming fairly presented financials and positive working capital

- Quarterly CPA attestations verifying ongoing federal employment tax compliance

- Surety bond of at least the greater of $50,000 or 5% of the prior year's federal employment tax liability under Section 3511, capped at $1 million

- $1,000 non-refundable application fee submitted through the IRS Online Registration System

Ongoing Maintenance Obligations

Certification isn't a one-time achievement. CPEOs must:

- Periodically verify they continue to meet all certification requirements

- Notify the IRS of any material changes that could affect certification accuracy

- Submit to independent financial reviews on an ongoing basis

- Provide written notice to each client within 10 days of any suspension or revocation

This 10-day client notification requirement exists specifically to protect businesses — but it also signals how quickly CPEO status can shift. Understanding these standards helps explain why CPEO certification carries real weight as a trust signal when evaluating PEO partners.

Key Benefits of Working With a Certified PEO

Federal Tax Liability Protection

Because a CPEO assumes sole liability for federal employment taxes on covered wages, clients are shielded from IRS collection — provided they've properly remitted funds to the CPEO. For small businesses, this eliminates one of the more serious compliance risks in the co-employment model.

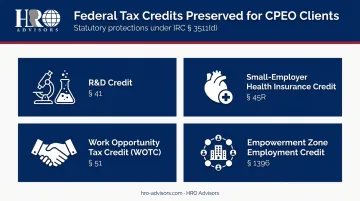

Tax Credit Preservation

Under IRC § 3511(d), clients of CPEOs retain the right to claim specified federal tax credits that could otherwise be complicated under co-employment. Preserved credits include:

- Section 41: Research and development credit

- Section 45R: Small-employer health insurance credit

- Section 51: Work Opportunity Tax Credit (WOTC)

- Section 1396: Empowerment zone employment credit

Access to Enterprise-Level Benefits

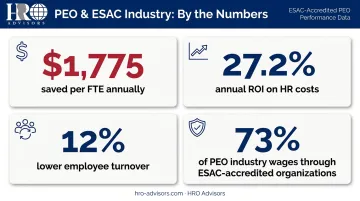

CPEOs pool multiple client businesses to negotiate group health insurance and benefits plans that smaller companies couldn't access independently. According to NAPEO research, businesses using PEOs save an average of $1,775 per full-time employee annually — including $654 in health benefits savings and $965 in internal HR personnel costs.

Reduced Administrative Burden

PEO clients use an average of 1.6 HR FTEs per 100 employees, compared to 2.6 for businesses without a PEO — a reduction in overhead that compounds quickly at scale. The same NAPEO research reports a 27.2% annual ROI based on cost savings alone, along with 12% lower employee turnover and a 50% lower likelihood of going out of business.

These figures reflect PEOs broadly. CPEOs add a layer of federal accountability on top of that baseline value.

Who Benefits Most from CPEO Status?

CPEO protections matter most for:

- Small to mid-sized businesses (roughly 5–500 employees) running complex, multi-state payroll

- Companies in regulated industries — healthcare, financial services, life sciences — where tax errors carry severe consequences

- R&D-intensive companies that need to preserve federal research credits under co-employment

- Businesses in states with minimal PEO licensing that want federal-level oversight as a backstop

If your business falls into more than one of these categories, CPEO status shifts from a nice-to-have into a meaningful risk management decision.

Limitations and Risks of CPEOs to Know

CPEO status is not a blanket guarantee. Several real limitations apply.

Certification Can Be Revoked — Fast

The IRS holds sole oversight authority over CPEOs. Revocation can result from material compliance failures or administrative issues, and the CPEO is only required to notify clients within 10 days of the effective date. Since transitioning to a new PEO typically takes 30–90 days, 10 days of notice leaves most businesses with very little time to regroup.

Narrow Provider Pool

CPEO certification is relatively uncommon among the 500+ PEOs operating in the U.S. Limiting your search exclusively to certified providers narrows your options — and excludes many well-run, financially stable organizations that skip certification because the IRS requirements are costly to maintain.

Some of the most specialized, industry-focused providers operate without CPEO status and still deliver strong compliance outcomes, including those serving:

- Construction and real estate firms

- Hospitality and tourism businesses

- Nonprofit organizations

Scope Is Limited to Remuneration the CPEO Remits

The federal tax protections under IRC § 3511 apply only to wages remitted through the CPEO. Any compensation outside that structure isn't covered by those protections. Businesses with complex compensation arrangements should review their specific situation with a tax advisor before assuming full protection.

Beyond CPEO: Other Accreditations and How to Find the Right PEO Partner

ESAC Accreditation

The Employer Services Assurance Corporation (ESAC) is the official financial assurance and accreditation body for the PEO industry. ESAC-accredited PEOs must verify ongoing financial stability, ethical business conduct, regulatory compliance, and adherence to more than 40 operational standards.

What ESAC verifies on a quarterly basis:

- Timely and accurate payment of federal and state employment taxes

- Health and workers' compensation insurance premiums

- Retirement plan contributions

- Employee wages

ESAC states that nearly 73% of PEO industry wages are paid through ESAC-accredited organizations — a notable concentration given how few PEOs hold this status. It's a meaningful quality signal, particularly when evaluating non-certified providers.

Additional Quality Indicators

- SOC 1 Type 2 report — developed under AICPA standards, this examines a service organization's internal controls over financial reporting. It's relevant when evaluating a PEO's data handling and financial processes

- Workplace culture awards — recognitions like Great Place to Work can indicate that the PEO's internal team is engaged, which often correlates with better client service quality

- NAPEO membership — the National Association of Professional Employer Organizations sets industry standards and provides a professional framework that reputable PEOs typically participate in

Finding the Right PEO Without Doing It Alone

Evaluating PEOs — certified or not — means comparing pricing structures, service capabilities, contract terms, and compliance credentials across dozens of providers. Most business owners don't have the time or resources to do that analysis thoroughly on their own.

HRO Advisors offers a free PEO comparison service that matches businesses with up to 8 providers — drawn from a network of more than 500 — and clients report savings of up to 40% on HR costs. The process covers pricing, service capabilities, compliance features, and industry fit. HRO Advisors advisors negotiate directly with providers on the client's behalf, at no cost to the business.

Frequently Asked Questions

What is a Certified Professional Employer Organization?

A CPEO is a PEO that has been voluntarily certified by the IRS under the program established by the Small Business Efficiency Act of 2014. Certification requires meeting strict standards around financial stability, tax compliance, and organizational integrity — and gives client businesses added legal protections for federal employment taxes under IRC § 3511.

Is CPEO status a legitimate IRS designation?

Yes. CPEO status is a verifiable IRS designation, not a self-awarded marketing claim. Businesses can confirm any PEO's current certification status by checking the IRS CPEO Public Listings, which also identifies PEOs whose certification has been suspended or revoked.

How does a PEO make money?

Most PEOs charge either a percentage of total payroll or a flat per-employee-per-month (PEPM) fee. Some also earn margin on benefits by pooling clients into group plans and negotiating at wholesale rates — a structure that can still deliver net savings for the client.

What's the key difference between a CPEO and a regular PEO?

The core difference is federal tax liability. Under IRC § 3511, a CPEO is solely liable for clients' federal employment taxes on covered wages. With a non-certified PEO, both the client and the PEO may be held liable — creating real financial exposure for the business if the PEO fails to remit taxes properly.

How do I verify if a PEO is IRS-certified?

Check the IRS CPEO Public Listings directly. It's updated regularly and is the only authoritative source — no third-party directory can substitute for it.

Do I need a CPEO, or will a non-certified PEO work?

For most small businesses, a well-run non-certified PEO with ESAC accreditation and strong surety bonding can provide comparable financial protections. Restricting your search to CPEOs alone may cause you to overlook excellent providers with stronger industry-specific expertise or more competitive pricing. A structured comparison across both categories — guided by an independent broker — is usually the most effective approach.