The decision to manage workers' comp in-house or outsource it isn't just an HR preference — it has direct financial consequences. In-house management gives you full control, but demands real expertise and bandwidth. Outsourcing transfers that burden to specialists, but only works if you choose the right partner.

This guide breaks down both approaches side-by-side, exposes the hidden costs that make in-house management more expensive than it appears, and gives you a practical framework for choosing the model that fits your business.

Key Takeaways

- In-house workers' comp works best for larger businesses with dedicated risk management staff and low claim frequency.

- Outsourcing to a PEO provides access to specialists, pooled insurance buying power, and proactive EMR management most internal teams can't match.

- EMR is a direct cost lever — a rising rate inflates premiums year over year, and reversing it requires expertise, not just effort.

- Small and mid-sized businesses in high-risk industries typically see the strongest ROI from outsourcing.

- The right choice comes down to four factors: company size, HR capacity, industry risk profile, and compliance cost tolerance.

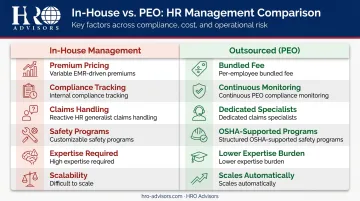

In-House vs. Outsourced Workers' Comp: Quick Comparison

| Factor | In-House Management | Outsourced (PEO) |

|---|---|---|

| Cost Structure | Fixed HR staff costs + variable EMR-driven premiums; audit surprises disrupt cash flow | Per-employee or bundled PEO fee; pay-as-you-go billing reduces audit exposure |

| Compliance Management | Internal team tracks state-specific changes across all jurisdictions | PEO monitors continuously; assumes co-employer compliance responsibility |

| Claims Handling | HR generalists coordinate with insurer — typically reactive | Dedicated claims specialists with return-to-work programs; avg. lost-time duration drops from 9–12 months to 8–12 weeks |

| Risk & Safety Programs | Customizable, but execution depends on internal bandwidth | Structured programs + OSHA support; correlates with 9.4% fewer injury claims and 26% avg. cost savings |

| Expertise Required | High — EMR mechanics, state regs, audit prep, claims adjudication | Lower — PEO specialists handle technical complexity |

| Scalability | Difficult without adding dedicated HR headcount | Scales automatically with your workforce |

Staff time, compliance training, audit management, and EMR-driven premium increases are costs that businesses consistently underestimate when first comparing the two models.

Outsourcing costs are typically structured as a per-employee fee or bundled into a PEO arrangement. According to NAPEO research, businesses using PEOs save an average of $66 per employee specifically on workers' comp, with 30% of new PEO clients reporting lower workers' comp costs and none reporting higher costs. Total PEO ROI averages 27.2% annually, not counting the administrative hours recaptured by your team.

What Is In-House Workers' Compensation Management?

With in-house management, your internal HR or operations team owns every aspect of workers' compensation. That means purchasing and renewing the policy, managing active claims, preparing for audits, and staying current on state and federal compliance requirements.

What That Actually Involves

The full scope is broader than most businesses realize when they first take it on:

- Policy procurement and renewal — sourcing coverage, managing relationships with carriers

- Injury reporting and documentation — ensuring timely, accurate filing (New York fines late injury reports $2,500 per incident)

- Claims adjudication coordination — working with insurers to manage active claims from filing through resolution

- EMR monitoring — tracking your experience modification rate and understanding what's driving it

- Audit preparation — assembling payroll records, journals, ledgers, and tax reports; auditors can examine records up to three years after a policy period ends

- Multi-state compliance — staying current on regulatory changes across every state where you have employees

Where In-House Management Works Well

In-house management genuinely excels in specific conditions:

- Large enterprises with dedicated risk management teams who specialize in this function

- Low-risk industries (technology, professional services, consulting) with minimal claim frequency

- Organizations with established compliance infrastructure and strong carrier relationships

- Businesses where direct control over every claims decision is operationally or legally important

Where It Breaks Down

The model runs into trouble when HR teams are managing workers' comp alongside five other priorities. Common failure patterns include:

- Reactive claims handling that drives up costs over time

- Limited visibility into EMR trends until premiums already spike

- Difficulty tracking multi-state regulatory changes consistently

- Audit surprises that create unexpected cash flow disruption

The root cause is rarely a lack of effort. Workers' comp management requires specialized expertise that most HR generalists simply aren't hired — or trained — to carry.

What Is Outsourced Workers' Compensation Management?

Outsourcing workers' comp means partnering with a Professional Employer Organization (PEO) that assumes co-employer responsibility for your workforce. Under this model, the PEO takes over policy management, claims handling, compliance monitoring, safety program design, and audit management on your behalf.

How the PEO Model Works for Workers' Comp

The core mechanism is co-employment. According to NAPEO, a PEO and client company share and allocate employer responsibilities for worksite employees. For workers' comp specifically, this means your employees are covered under the PEO's master policy — giving small and mid-sized businesses access to insurance rates and risk pools that typically belong to much larger employers.

That pooled buying power matters. A 10-person manufacturing company shopping individually for workers' comp coverage faces rates based on its own limited claims history. The same company under a PEO's master policy benefits from a far larger, more diversified risk pool.

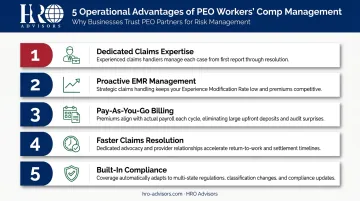

Five Operational Advantages

- Dedicated claims expertise — specialized professionals handle cases, not HR generalists juggling multiple functions

- Proactive EMR management — PEOs actively work to keep your modification rate in check before premiums escalate

- Pay-as-you-go billing — premiums align to actual payroll cycles rather than upfront estimates, reducing audit exposure

- Faster claims resolution — structured return-to-work programs reduce lost-time durations and lower total claim costs

- Built-in compliance — PEO monitors regulatory changes across all operating states

Not All PEOs Are Equal

Businesses should evaluate PEOs specifically on their claims management model, safety program depth, industry experience, and pricing transparency — these vary considerably across providers.

HRO Advisors is a free PEO broker that compares up to 8 PEOs side-by-side across these dimensions. You get a personalized assessment of workers' comp coverage, safety programs, and compliance features for your specific industry and risk profile — with direct negotiation handled on your behalf at no cost.

Where Outsourcing Delivers the Clearest ROI

Outsourcing makes the most financial sense for:

- Small to mid-sized businesses without a dedicated HR or risk management function

- High-risk industries — construction, manufacturing, healthcare, senior living — where injury frequency and claim costs are elevated

- Multi-state operations navigating varying state workers' comp regulations simultaneously

- Fast-growing companies that need scalable HR infrastructure without proportionally scaling headcount

BLS 2024 data shows nursing and residential care facilities recording 5.5 injuries per 100 full-time workers, hospitals at 5.1, and manufacturing at 2.7. The National Safety Council put total work injury costs at $181.4 billion in 2024 — with a single medically consulted injury averaging $48,000. In these environments, reactive claims management isn't just inefficient; it's expensive by default.

In-House vs. Outsourced Workers' Comp: Which Approach Fits Your Business?

Neither model is universally better. The right choice comes down to four variables:

- Company size and HR capacity

- Industry risk profile and claim frequency

- Internal compliance expertise

- Cost tolerance for premium volatility or compliance errors

The EMR Factor

Your Experience Modification Rate is the single most important cost lever in workers' comp management. As NCCI explains, the experience rating modification factor is multiplied directly by your manual premium to determine what you actually pay. A rate above 1.0 inflates premiums; below 1.0 reduces them.

That math makes EMR a strategic priority — not just an accounting detail. Businesses with claim spikes or a rising EMR face a harder question: does your internal team have the bandwidth and expertise to reverse that trend?

A PEO with proactive claims and safety management can often achieve EMR improvement faster than an internal team in reactive mode — because they're doing this work across hundreds of client companies simultaneously.

Situational Recommendations

Choose in-house management if:

- Your business employs 100+ people with a dedicated HR or risk management team

- You operate in a low-risk industry with minimal claim history

- You have established compliance systems and a strong carrier relationship

- Direct control over every claims decision is a priority

Choose outsourced management (PEO) if:

- Your HR team is stretched thin across multiple functions

- Your industry carries elevated injury risk (construction, manufacturing, healthcare)

- You operate across multiple states with varying regulations

- Your EMR has been trending upward without a clear corrective strategy

- You want to stabilize or reduce workers' comp premiums without adding internal headcount

The True Cost of In-House Management

In-house management appears cheaper on the surface because there's no PEO fee. The full cost, however, includes staff hours spent on claims coordination and audit preparation, compliance training, premium volatility from EMR changes, and potential legal exposure from noncompliance.

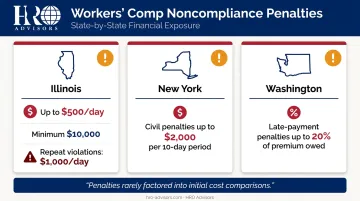

State penalties alone show what's at stake:

- Illinois: Up to $500/day (minimum $10,000) for knowingly failing to provide coverage; repeat violations reach $1,000/day

- New York: Civil penalties up to $2,000 per 10-day period for noncompliance exceeding 10 days

- Washington: Late-payment penalties up to 20% of premium owed

These exposures rarely factor into the initial cost comparison — but they're the ones that tend to surface at the worst possible time.

Conclusion

In-house workers' comp management suits businesses with the infrastructure and expertise to handle it proactively — dedicated risk staff, low claim environments, and established compliance systems. For businesses where workers' comp complexity exceeds internal capacity, outsourcing through a PEO is the stronger choice. The decision is ultimately about capacity and expertise, not preference.

For businesses unsure where they fall, HRO Advisors offers a free comparison with no obligation. Their advisors collect your current HR costs and compliance requirements, then compare up to 8 PEOs side-by-side and negotiate rates on your behalf — at no cost to you.

Reach them at 866-755-0288, email info@hro-advisors.com, or start with their free PEO comparison tool.

Frequently Asked Questions

What is outsourcing in insurance?

Outsourcing in insurance refers to delegating insurance-related management tasks — such as workers' comp policy administration, claims handling, and compliance — to a third-party provider like a PEO. The PEO uses its scale and pooled employee base to negotiate better rates and manage risk more efficiently than most businesses can independently.

Can a hernia be covered under workers' compensation?

A hernia can be covered under workers' comp if it results directly from a work-related activity such as heavy lifting. Coverage depends on state law and requires the employee to demonstrate a clear connection between the injury and specific job duties. States like Oklahoma and North Carolina have specific statutory proof requirements for this.

What is the Experience Modification Rate (EMR) and why does it matter?

The EMR is a multiplier applied to your workers' comp premium based on your claims history relative to industry peers, as calculated by NCCI. A rate above 1.0 increases your premium; below 1.0 reduces it. Because it compounds annually, even a modest EMR increase compounds into significant premium growth over time.

What does a PEO do for workers' compensation?

A PEO co-employs your workforce and places your employees under its master workers' comp policy, giving your business access to rates negotiated across a much larger risk pool. The PEO also manages claims, handles compliance and audits, and runs safety programs on your behalf.

Can small businesses afford to outsource workers' compensation management?

PEO arrangements are often more cost-effective for small businesses than in-house management once all hidden costs are factored in. NAPEO research found 30% of new PEO clients reported lower workers' comp costs — and none reported higher. PEO brokers like HRO Advisors offer free comparison services that show the true cost differential before you commit.

How do I know if my company is ready to outsource workers' compensation?

Watch for these signals:

- Your HR team manages claims reactively, not proactively

- Your EMR has risen over the past two to three years without a corrective plan

- You've faced audit surprises or compliance penalties

- You operate in a high-risk industry without a dedicated risk management function