Miss a quarterly SUI filing or forget to register for withholding before your first payroll run, and you're looking at financial penalties that compound quickly. This guide focuses specifically on the state-level side of that picture.

What you'll find here: the tax types North Dakota employers must manage, current rates, registration steps, the forms involved, key deadlines, and how a PEO can take much of this off your plate entirely.

Key Takeaways

- North Dakota employers have two core state payroll tax obligations: income tax withholding and State Unemployment Insurance (SUI) — plus a mandatory workers' compensation requirement.

- North Dakota uses the federal Form W-4 for state withholding; no separate state form is required.

- SUI is filed quarterly through the UI EASY portal; income tax withholding is managed through ND TAP.

- Reciprocity agreements with Minnesota and Montana allow qualifying employees to be exempt from ND income tax withholding via Form NDW-R.

- A PEO takes over registration, quarterly filings, and ongoing compliance — a broker like HRO Advisors can match you with the right provider at no added cost.

North Dakota Payroll Tax Obligations at a Glance

Two state agencies oversee employer payroll taxes in North Dakota:

- North Dakota Office of State Tax Commissioner — administers state income tax withholding. Employers register and file through ND TAP.

- Job Service North Dakota — administers State Unemployment Insurance (SUI). Employers register and file through the UI EASY portal.

Who Triggers Liability

An employer becomes liable for North Dakota payroll taxes if either of these conditions is met:

- Paid $1,500 or more in wages during any calendar quarter, OR

- Had at least one employee working any part of a day during 20 or more weeks in a calendar year

Meeting either threshold triggers registration obligations — including new hire reporting.

New Hire Reporting

Employers must report all new hires to the state within 20 days of the employee's first day of work. Key requirements include:

- Form: Use federal Form W-4 or SFN 1018

- Electronic filing: Required for employers with 25 or more employees

- Penalties: $20 per occurrence for late or inaccurate reports; rises to $250 per occurrence if the failure involves a conspiracy not to report

State Income Tax Withholding

Who Is Subject to Withholding

Withholding applies to any employee performing services in North Dakota whose wages are subject to federal income tax withholding. North Dakota residents working in other states must also have ND income tax withheld — unless the employer is already required to withhold income tax for that other state.

2025 Withholding Rate Brackets

North Dakota uses a three-bracket progressive structure. These employer withholding tables apply to annualized wages for employees using 2020 or later W-4 forms:

| Filing Status | Annual Taxable Wages | Withholding |

|---|---|---|

| Single / MFS / HOH | $0 – $55,975 | $0 (0%) |

| Single / MFS / HOH | $55,975 – $252,325 | 1.95% of amount over $55,975 |

| Single / MFS / HOH | Over $252,325 | $3,828.83 + 2.50% over $252,325 |

| Married Filing Jointly | $0 – $55,488 | $0 (0%) |

| Married Filing Jointly | $55,488 – $164,038 | 1.95% of amount over $55,488 |

| Married Filing Jointly | Over $164,038 | $2,116.73 + 2.50% over $164,038 |

Source: 2025 North Dakota Income Tax Withholding Rates & Instructions

No separate North Dakota withholding certificate is required: employers use the federal Form W-4 for both federal and state calculations.

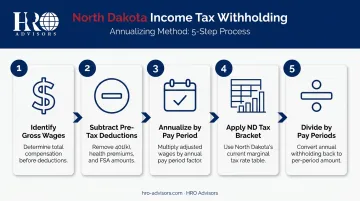

Calculating Withholding

Calculate withholding using the annualizing method:

- Identify gross wages for the pay period

- Subtract pre-tax deductions

- Multiply by the number of pay periods to annualize

- Apply the appropriate bracket from the table above based on filing status

- Divide the resulting annual withholding by pay periods to get the per-paycheck amount

For W-4 forms dated before 2020, use the allowance-based calculation tables. For 2020 and later W-4 forms, use income adjustments and dollar amounts as shown in the brackets above.

Supplemental Wages

For bonuses, commissions, and similar payments, North Dakota offers two options. Employers can apply a flat 1.50% rate directly to the supplemental wages, or use the aggregate method: combine supplemental and regular wages, calculate withholding on the total, then subtract the withholding already calculated on regular wages.

Reciprocity Agreements

North Dakota has reciprocity agreements with Minnesota and Montana. Residents of either state who work in North Dakota may claim exemption from ND income tax withholding by completing Form NDW-R and submitting it to their employer.

Employer obligations:

- Retain Form NDW-R on file

- Submit copies to the ND Office of State Tax Commissioner by March 31 each year

- Employees must renew the form annually; the deadline for employee submission to the employer is February 28

Withholding Exemptions

The following wages are exempt from North Dakota income tax withholding:

- Wages paid by farmers or ranchers for agricultural labor

- Wages excluded from federal withholding under IRC Section 3401 (such as certain domestic service)

- Wages paid to enrolled members of a federally recognized Indian Tribe who live and work on a North Dakota Indian reservation

State Unemployment Insurance (SUI)

SUI is an employer-paid tax — employees contribute nothing. It funds temporary benefits for workers who lose their jobs through no fault of their own. Most for-profit employers meeting the general liability thresholds must pay, though agricultural employers and certain nonprofits may qualify for different thresholds or exemptions.

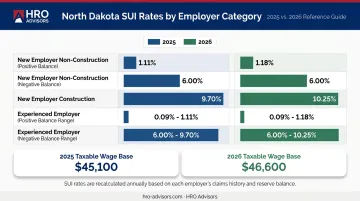

SUI Taxable Wage Base and Rates

SUI tax is calculated only on wages up to the annual taxable wage base per employee. The base increases each year:

| Year | Taxable Wage Base |

|---|---|

| 2025 | $45,100 |

| 2026 | $46,600 |

Current SUI rates, sourced from Job Service North Dakota's official rate schedules:

| Employer Type | 2025 Rate | 2026 Rate |

|---|---|---|

| New employer (non-construction, positive balance) | 1.03% | 1.00% |

| New employer (non-construction, negative balance) | 6.09% | 6.07% |

| New employer (construction) | 9.69% | 9.67% |

| Experienced employers (positive balance range) | 0.08% – 1.14% | 0.07% – 1.10% |

| Experienced employers (negative balance range) | 6.09% – 9.69% | 6.07% – 9.67% |

Experience ratings are recalculated annually. A lower unemployment claims history produces a lower rate over time.

Quarterly Filing Process and Deadlines

Once you know your rate, filing on time is what keeps it from rising. Employers submit a Contribution and Wage Report each quarter through the UI EASY portal, reporting wages paid and taxes owed.

| Quarter | Due Date |

|---|---|

| Q1 (Jan–Mar) | April 30 |

| Q2 (Apr–Jun) | July 31 |

| Q3 (Jul–Sep) | October 31 |

| Q4 (Oct–Dec) | January 31 |

Late filing penalty: 5% of contributions due per month, up to 20% or a $500 maximum, with a minimum of $25 for the first delinquency and $100 for subsequent ones in the same year. Each late filing is also recorded against your account history — which directly factors into your experience rate at the next annual recalculation.

Workers' Compensation Insurance

North Dakota is a monopolistic workers' compensation state. All employers — even those with a single employee — must purchase coverage exclusively from the state fund: Workforce Safety & Insurance (WSI). No private carriers are authorized to provide this coverage.

Coverage must be in place before the first employee begins work. It applies to full-time, part-time, seasonal, and occasional employees.

Representative WSI Base Rates (Effective July 1, 2025)

Rates are based on industry classification and claims history. Employers who maintain strong safety records may earn a lower experience modifier, which adjusts their premium up or down based on actual claims history relative to industry averages.

| Industry | Class Description | Base Rate (per $100 wages) |

|---|---|---|

| Office/Clerical | Clerical Office Employees | $0.13 |

| Retail | Stores – Retail | $0.73 |

| Services | Building Custodians & Janitorial | $1.91 |

| Manufacturing | Light Metal/Nonmetal Mfg. | $1.25 |

| Construction | Building Construction | $3.38 |

| Construction | Excavating | $2.01 |

Source: 2025 WSI Classification Manual

Registration and Ongoing Obligations

Employers apply through the WSI website before any employees start. Premiums are based on actual wages, and payroll reporting is completed quarterly through the myWSI online portal.

Filing Requirements, Registration, and Due Dates

Registering as a New Employer

- Income tax withholding account: Register through ND TAP before withholding obligations begin. Existing employers can find their Withholding Account Number on Form 306 or by contacting the Office of State Tax Commissioner.

- SUI account: Register with Job Service North Dakota through the UI EASY portal to receive an Employer Account Number (EAN). Registration must occur within 20 days of hiring workers or acquiring a business.

Form 306 — Income Tax Withholding Return

Form 306 remits North Dakota income tax withholding to the state. Key rules:

- Quarterly filing required if prior-year withholding was $1,000 or more (electronic filing mandatory)

- Annual filing allowed if prior-year withholding was under $1,000, due January 31

- Must be filed even during periods with no wages paid to keep the account active

- Paper filing is only permitted if the employer is not required to file electronically or has an approved waiver

Annual Filings

By January 31 each year, employers must submit:

- W-2s for all employees

- 1099s (where applicable)

- Form 307 — the North Dakota Annual Reconciliation, a transmittal document summarizing all W-2s and 1099s filed for the year

Submit all filings through ND TAP or compatible accounting software.

Payment Options and Penalty Summary

ND TAP supports two payment methods:

- ACH Debit: the state withdraws directly from your account

- ACH Credit: you initiate the transfer through your bank

| Obligation | Penalty |

|---|---|

| Late/unpaid Form 306 (withholding) | 5% of tax due (or $5 minimum) per month, up to 25%; plus 1% monthly interest on unpaid balances |

| Late SUI Contribution and Wage Report | 5% per month, up to 20% or $500 max |

Maintain payroll and accounting records for at least five years from the contribution due date to support audits and amendments.

How a PEO Can Simplify North Dakota Payroll Compliance

What a PEO Takes Off Your Plate

Under a co-employment arrangement, a PEO registers and maintains state withholding and SUI accounts on the employer's behalf, then handles the ongoing work:

- Calculates and remits income tax withholding each pay period

- Files Form 306 quarterly and Form 307 annually through ND TAP

- Submits the quarterly SUI Contribution and Wage Report via UI EASY

- Manages workers' compensation obligations through WSI

- Tracks rate changes, wage base updates, and filing deadlines

For small and mid-sized businesses without dedicated payroll staff, that's a real reduction in compliance risk.

The Business Case

According to NAPEO research, businesses using PEOs grow twice as fast, experience 12% lower employee turnover, and are 50% less likely to go out of business. The average PEO client sees a 27.2% annual ROI from cost savings alone.

Beyond compliance, PEOs give small businesses access to enterprise-level benefits packages — health plans, retirement options, and other programs that are difficult to offer independently. For North Dakota employers competing for workers in a tight labor market, those benefits packages can be the difference between attracting strong candidates and losing them to larger competitors.

How HRO Advisors Helps

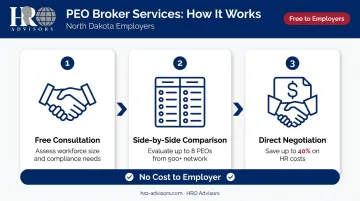

The ROI numbers are compelling — but finding the right PEO requires comparing dozens of variables across providers. That's where HRO Advisors comes in. As a free PEO broker service, they handle the search and selection process for North Dakota employers through three steps:

- Free consultation — understand your workforce size, compliance needs, and current costs

- Side-by-side comparison — evaluate up to 8 PEO providers drawn from a network of 500+

- Direct negotiation — HRO Advisors negotiates with providers on your behalf, with clients often saving up to 40% on HR costs

The service costs nothing to the employer. HRO Advisors is paid by the provider you select, and that arrangement doesn't increase your cost. Their process is built to lower it.

For a no-obligation consultation, contact HRO Advisors at 866-755-0288 or email info@hro-advisors.com.

Frequently Asked Questions

Does payroll software handle tax compliance?

Payroll software automates calculations and can submit filings, but the legal responsibility for accuracy stays with the employer. A PEO goes further — under co-employment, it takes on compliance obligations directly, including registering state accounts and remitting taxes on your behalf.

Do I have to file a North Dakota state tax return as an employer?

Yes. Employers must remit withheld income taxes via Form 306 and file quarterly SUI Contribution and Wage Reports — both obligations apply regardless of whether employees file their own state returns.

What is ND Form 307?

Form 307 is North Dakota's Annual Reconciliation — a transmittal document that summarizes all W-2s and 1099s filed for the tax year. It is due January 31 and must be submitted electronically through ND TAP or compatible accounting software.

What is the SUI wage base in North Dakota?

The 2025 taxable wage base is $45,100; for 2026, it increases to $46,600. SUI tax is only calculated on wages up to this limit per employee per year. Job Service North Dakota updates the wage base annually.

Does North Dakota have a state withholding form?

No. North Dakota uses the federal Form W-4 for state income tax withholding calculations. The only exception is Form NDW-R, which qualifying Minnesota and Montana residents use to claim a reciprocity exemption from ND withholding.

What are North Dakota's reciprocity agreements for payroll taxes?

North Dakota has reciprocity agreements with Minnesota and Montana. Employers who receive a Form NDW-R from an eligible resident must file copies with the Office of State Tax Commissioner by March 31 each year.