Getting this wrong is expensive. Missing a single notice deadline can trigger excise taxes of $100 per day per beneficiary — and those penalties compound fast.

This guide is written for HR managers, business owners, and operations leads at companies with 20 or more employees who need a clear, actionable understanding of their federal COBRA obligations. We cover employer eligibility, qualifying events, notice timelines, coverage duration, cost rules, and penalties.

Key Takeaways

- COBRA applies to private-sector employers with 20+ employees on more than 50% of typical business days in the prior calendar year

- Employers must notify the plan administrator within 30 days of a qualifying event; the plan administrator then has 14 days to send an election notice

- Qualified beneficiaries have 60 days to elect COBRA and can be charged up to 102% of total plan cost

- Non-compliance triggers IRS excise taxes of $100/day per beneficiary, plus exposure to DOL penalties and beneficiary lawsuits

- 43 states and Washington D.C. have mini-COBRA laws extending continuation coverage obligations to smaller employers

Which Employers Are Subject to COBRA

The 20-Employee Threshold

Federal COBRA applies to private-sector group health plans — and most state and local government plans — maintained by employers that had 20 or more employees on more than 50% of their typical business days in the prior calendar year.

Two categories are exempt: federal government plans and plans sponsored by churches or certain church-related organizations.

Counting toward that threshold works as follows:

- Full-time employees count as 1.0

- Part-time employees count as a fraction based on hours worked relative to full-time hours

- Example: An employee working 20 hours per week when full-time is 40 hours counts as 0.5

This means a company with 18 full-time employees and 8 part-timers each working half-time (4.0 full-time equivalents) still clears the 20-employee threshold.

What Qualifies as a "Group Health Plan"

COBRA covers any employer arrangement that provides medical care to employees and their families. Covered plan types include:

- Inpatient and outpatient hospital care

- Physician care and surgery

- Prescription drug coverage

- Dental and vision plans (each treated as a separate plan if offered separately)

Not covered: Life insurance and disability income coverage are excluded from COBRA entirely.

Plan Administrator Responsibility

Once coverage scope is established, administration is the next obligation. DOL guidance requires employers subject to COBRA to designate a plan administrator — either the employer itself or a third-party administrator — responsible for administering continuation coverage and sending required notices. Delegating administration to a TPA does not transfer legal compliance responsibility. That liability stays with the employer.

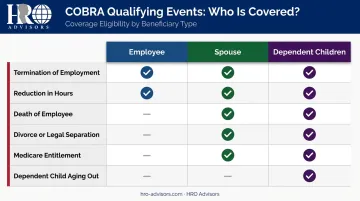

COBRA Qualifying Events and Covered Beneficiaries

A qualified beneficiary is any individual covered under the group health plan on the day before a qualifying event occurs. This includes the covered employee, their spouse or former spouse, and dependent children. Children born to or placed for adoption with a covered employee during a COBRA period also qualify as beneficiaries.

Qualifying Events by Beneficiary Type

| Qualifying Event | Employee | Spouse | Dependent Children |

|---|---|---|---|

| Termination (other than gross misconduct) | ✓ | ✓ | ✓ |

| Reduction in work hours causing loss of coverage | ✓ | ✓ | ✓ |

| Death of covered employee | — | ✓ | ✓ |

| Divorce or legal separation | — | ✓ | ✓ |

| Covered employee becomes entitled to Medicare | — | ✓ | ✓ |

| Dependent child loses eligibility (e.g., ages out) | — | — | ✓ |

Resignation, layoff, and retirement all count as qualifying events. Only termination for gross misconduct disqualifies an employee from COBRA.

When FMLA Leave Triggers COBRA (And When It Doesn't)

Taking FMLA leave is not itself a qualifying event and does not trigger COBRA. However, if an employee on FMLA leave fails to return to work when the leave period ends, that failure can create a qualifying event. Sending COBRA notices prematurely during FMLA — or missing the notice after a non-return — both create documented compliance exposure.

COBRA Notice Requirements and Deadlines

The Required Notices

General Notice (Initial Rights Notice): Must be provided to newly covered employees and their spouses within 90 days of coverage beginning. This notice can be included in the Summary Plan Description. The DOL's model General Notice is available for employers to use directly.

Election Notice: After a qualifying event is reported, the plan administrator must send an election notice to each qualified beneficiary. Each notice must include:

- The qualifying event and coverage loss date

- Available coverage options and premium costs

- Election deadline and payment procedures

The DOL's model Election Notice satisfies all federal disclosure requirements.

Who Notifies Whom — and When

Notice responsibilities split between employers and beneficiaries depending on the qualifying event:

Employer notifies the plan administrator within 30 days for:

- Employee termination or reduction in hours

- Employee death

- Employee becoming entitled to Medicare

- Employer bankruptcy (in certain cases)

Employee or beneficiary notifies the plan administrator (minimum 60-day window) for:

- Divorce or legal separation

- A dependent child losing eligibility under plan rules

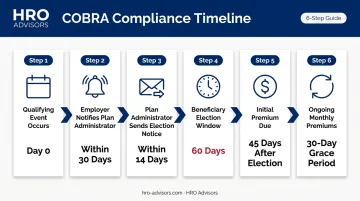

The Full COBRA Timeline

Follow this sequence for every qualifying event:

- Day 0 — Qualifying event occurs

- Within 30 days — Employer notifies plan administrator

- Within 14 days of that notification — Plan administrator sends election notice to beneficiaries (or within 44 days from the qualifying event if the employer is also the plan administrator)

- 60 days from the later of coverage loss or election notice receipt — Beneficiary election window closes

- 45 days after election — Initial premium payment due

- Ongoing — Subsequent monthly premiums with a 30-day grace period

Missing any step in this sequence can trigger IRS excise tax penalties of $100 per beneficiary per day — and expose the employer to liability for any medical claims the beneficiary incurs during the gap.

How Long COBRA Coverage Lasts and What It Costs

Coverage Duration Rules

| Qualifying Event | Standard Duration |

|---|---|

| Job loss or reduction in hours | 18 months |

| Divorce, employee death, Medicare entitlement, or loss of dependent status | 36 months |

Two extensions can lengthen the standard 18-month period:

- Disability extension: If the Social Security Administration determines a qualified beneficiary was disabled before the 60th day of COBRA coverage and the disability continues through the initial 18 months, coverage can extend 11 additional months (29 months total)

- Second qualifying event: If a second qualifying event occurs during the initial 18-month period, affected beneficiaries may extend coverage to 36 months total

Premium Cost Rules

Employers are not required to subsidize COBRA — beneficiaries typically bear the full cost. What plans may charge:

- Standard periods: Up to 102% of the total plan cost (employee + employer contributions + 2% administrative fee)

- Disability extension period: Up to 150% of the total plan cost

Payment timeline rules:

- Beneficiaries have 45 days after electing COBRA to make the initial premium payment

- Subsequent monthly payments must include a grace period of at least 30 days

- Plans may terminate coverage if full payment isn't received by the end of any grace period

Penalties for Failing to Comply with COBRA

IRS Excise Tax

Under IRC Section 4980B, employers who fail to meet COBRA requirements face an excise tax of $100 per day per qualified beneficiary during the non-compliance period. For families, this caps at $200 per day.

A single missed election notice for a family of three over a six-week period can represent thousands in potential excise tax exposure, before any other enforcement action.

Additional thresholds under Section 4980B:

- Minimum tax after IRS examination: $2,500 (or $15,000 for more than de minimis failures)

- Cap for non-willful failures: the lesser of 10% of prior-year group health plan expenditures or $500,000

ERISA Civil Penalties and Litigation

The DOL can assess penalties of up to $110 per day for notice failures under ERISA Section 502(c)(1). Beyond regulatory penalties, employees have the right to sue in federal court, and courts regularly side with employees when employers fail to provide timely, accurate COBRA information.

COBRA election notice class actions have increased sharply. One notable example: Hicks v. Lockheed Martin Corp. settled for $1.25 million over deficient COBRA election notices. Defendants in similar cases include Citigroup, JPMorgan Chase, Target, and PepsiCo.

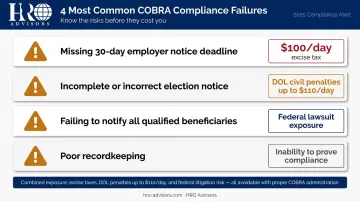

Most Common Compliance Failures

These penalties don't arise from deliberate evasion — they typically trace back to procedural gaps that employers overlook. The most common:

- Missing the 30-day employer notice deadline after a qualifying event

- Sending an incomplete or incorrect election notice (conflicting deadlines, missing payment addresses, language not understandable to average participants)

- Failing to send notices to all qualified beneficiaries, particularly spouses at separate addresses

- Poor recordkeeping that makes it impossible to prove notices were ever sent

Making COBRA Administration More Manageable

COBRA administration is operationally demanding. Employers must simultaneously track multiple qualifying events, manage overlapping deadlines, maintain proof of notice delivery, and keep pace with state-level mini-COBRA variations. For multi-state employers, those state-specific rules add another layer of complexity.

Outsourcing COBRA Administration

The numbers reflect how employers respond to that burden: according to IFEBP survey data, 79% of companies outsource COBRA administration, making it one of the most commonly delegated benefits functions. The same survey found 31% of companies cite legal compliance as a top benefits-department concern.

Third-party administrators and PEOs can handle notice generation, election tracking, and premium collection. What they cannot do is transfer legal liability — the DOL is clear: the employer remains legally responsible regardless of who administers the process. That makes choosing an experienced, reliable partner and maintaining oversight of key deadlines essential — not optional.

HRO Advisors can help you find PEO partners that handle COBRA administration — notice generation, deadline tracking, and premium collection — alongside your other HR obligations. The free consultation process maps your compliance requirements, then compares up to eight PEO providers side-by-side to match your company's size, industry, and regulatory exposure.

State Mini-COBRA Laws

Outsourcing COBRA administration doesn't eliminate the need to know which rules apply to you — especially if you operate across state lines. Federal COBRA doesn't cover employers with fewer than 20 employees, but many states do. According to SHRM, 43 states and Washington D.C. have mini-COBRA laws with their own thresholds, coverage periods, and qualifying event rules.

A few examples:

| State | Applies To | Duration |

|---|---|---|

| California (Cal-COBRA) | Employers with 2–19 employees | Up to 36 months |

| New York | State continuation coverage | Up to 36 months |

| North Carolina | Separate state continuation | 18 months |

| Texas | When federal COBRA doesn't apply | Up to 9 months |

Multi-state employers — and small employers under 20 headcount — should verify their obligations through each state's insurance department or an HR compliance expert.

Frequently Asked Questions

What are the requirements for an employer to offer COBRA?

COBRA applies to private-sector employers and most state and local government employers with 20 or more employees on more than 50% of typical business days in the prior calendar year. Federal and church plan employers are exempt. Qualifying employers must offer continuation coverage to eligible employees and dependents following a qualifying event.

Does COBRA cost my employer money?

COBRA doesn't require employers to subsidize coverage — qualified beneficiaries pay up to 102% of the full plan cost. Indirect costs do exist: administrative time, TPA fees, and serious financial exposure if compliance requirements aren't met — including IRS excise taxes, DOL penalties, and employee lawsuits.

What is the 60-day rule for COBRA?

The 60-day rule covers two separate obligations:

- Election window: Qualified beneficiaries have at least 60 days from coverage loss (or notice receipt, whichever is later) to elect COBRA.

- Self-reporting window: Employees or dependents must notify the plan administrator within 60 days of events like divorce or a dependent aging out.

What happens if an employer misses a COBRA deadline?

Missed deadlines can trigger an IRS excise tax of $100 per day per affected beneficiary (capped at $200/day per family), DOL civil penalties up to $110 per day for notice failures, and federal lawsuits from employees seeking coverage reimbursement and attorney's fees.

Are employers with fewer than 20 employees required to offer COBRA?

Federal COBRA does not apply below the 20-employee threshold. However, 43 states and Washington D.C. have mini-COBRA laws extending continuation coverage to small employers. Check your state's specific rules before assuming you have no obligation.

Can employers outsource COBRA administration?

Yes — and most do. Employers frequently use TPAs or PEOs to manage notices, elections, and premium collections. Legal compliance responsibility remains with the employer regardless, so selecting an experienced, accountable partner and monitoring key deadlines is non-negotiable.