Introduction

Many business owners assume workers' compensation covers everything when an employee gets hurt on the job. It doesn't.

Workers' comp handles the employee's medical bills and lost wages — but certain lawsuits can bypass it entirely, landing directly on the employer's doorstep. That's the gap employers liability (EL) coverage exists to fill.

The two coverages work together: workers' comp pays the injured worker, while employers liability protects the business if that worker — or someone connected to them — sues for negligence beyond what workers' comp provides.

This guide breaks down EL insurance — what it covers, what it doesn't, how it compares to workers' comp and EPLI, how limits work, and what it costs.

Key Takeaways

- Employers liability is Part Two of a standard workers' comp policy — not a separate product

- It responds when employee injury lawsuits fall outside workers' comp's legal protections

- Standard limits are 100/500/100; many high-risk businesses should carry more

- Businesses in North Dakota, Ohio, Washington, and Wyoming must buy stop-gap coverage separately

- A PEO can simplify access to workers' comp and EL coverage for small and mid-size businesses

What Is Employers Liability Coverage?

Employers liability insurance is formally defined as Part Two of the standard workers' compensation and employers liability policy (the NCCI-copyrighted WC 00 00 00 C form). It covers sums the employer is legally required to pay as damages for employee bodily injury — specifically when that liability falls outside the workers' comp system.

The Exclusive Remedy Doctrine (and Its Exceptions)

In most states, workers' comp operates as the exclusive remedy for on-the-job injuries. Employees receive statutory benefits; in exchange, they generally can't sue their employer in civil court. That protection, however, has holes. Legal commentary and state statutes identify specific scenarios where the exclusive remedy defense breaks down and employees — or related parties — can pursue a lawsuit:

- Intentional acts by the employer

- Dual-capacity situations where the employer is also a product manufacturer

- Third-party derivative claims that pull the employer back into litigation

- Certain injuries not covered under a state's workers' comp act

Each of these scenarios creates a direct litigation exposure that workers' comp won't touch — which is exactly where Part Two steps in.

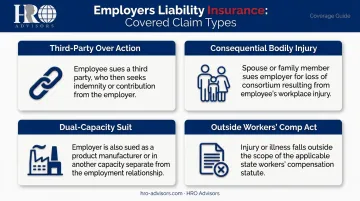

The Four Claim Types EL Insurance Addresses

IRMI identifies four distinct patterns where Part Two comes into play:

| Claim Type | What Happens |

|---|---|

| Third-Party Over Action | Employee sues a third party (equipment maker, contractor); that party seeks indemnity from the employer |

| Consequential Bodily Injury | Spouse or family member sues for loss of consortium tied to the employee's injury |

| Dual-Capacity Suit | Employer is also the product manufacturer; employee sues in that separate capacity |

| Outside Workers' Comp Act | Injury or illness falls outside what the state's workers' comp statute covers |

The Monopolistic States Exception

Four states — North Dakota, Ohio, Washington, and Wyoming — require employers to buy workers' comp through a state fund. State funds in these states do not include employers liability coverage. Businesses operating there must separately purchase stop-gap coverage from a private insurer to fill that gap.

What Employers Liability Insurance Covers — and What It Doesn't

When a covered EL lawsuit arises, the policy covers the employer's actual financial exposure, including legal defense costs the insurer is obligated to provide.

Covered costs typically include:

- Legal defense costs and attorney fees

- Court filing fees and litigation expenses

- Settlements negotiated before trial

- Court judgments after verdict

- Bond premiums and interest on judgments

Without this coverage, a single lawsuit can threaten a business's financial stability, even if the employer ultimately prevails.

Situations EL Insurance Does Cover

Common scenarios where Part Two coverage applies:

- A warehouse worker is injured and sues the equipment manufacturer. The manufacturer then files a third-party over action, claiming the employer's negligent maintenance contributed to the injury.

- A construction worker suffers a severe back injury. Their spouse files a loss of consortium claim for loss of companionship and household services — this is consequential bodily injury coverage in action.

- A factory employee is injured by a machine their employer also manufactures and sells. Because they sue in the employer's capacity as a product maker, it qualifies as a dual-capacity suit.

Situations EL Insurance Does NOT Cover

EL coverage has clearly defined exclusions. The NCCI policy form explicitly excludes:

- Bodily injury intentionally caused by the employer

- Criminal acts and violations of law

- Employment discrimination, harassment, and humiliation

- Wrongful termination and retaliation

- Punitive damages arising from illegal employment practices

Important: These excluded claims are covered by a different policy, Employment Practices Liability Insurance (EPLI). EL and EPLI are not interchangeable. Confusing the two creates dangerous coverage blind spots.

How Employers Liability Compares to Workers' Comp, EPLI, and General Liability

Workers' comp, EL, EPLI, and general liability all sound similar — but each fills a distinct gap. Understanding where one ends and another begins can save your business from a costly coverage blind spot.

Workers' Comp vs. Employers Liability

Workers' comp and EL coverage work together but serve entirely different purposes:

| Coverage Area | Workers' Compensation | Employers Liability |

|---|---|---|

| Medical costs | ✅ Yes | ❌ No |

| Lost wages | ✅ Yes | ❌ No |

| Disability benefits | ✅ Yes | ❌ No |

| Death benefits | ✅ Yes | ❌ No |

| Legal defense costs | ❌ No | ✅ Yes |

| Court judgments | ❌ No | ✅ Yes |

| Settlements | ❌ No | ✅ Yes |

| Who is protected | The injured employee | The employer's business |

Workers' comp is a no-fault, state-mandated system. EL steps in when the injured employee — or a connected party — bypasses that system through a lawsuit.

Employers Liability vs. EPLI

The distinction here trips up a lot of business owners:

- EL covers lawsuits from physical workplace injuries or illnesses — claims rooted in bodily harm

- EPLI covers employment-related legal claims: wrongful termination, discrimination, sexual harassment, retaliation, and breach of employment contract

Both policies cover legal defense costs, judgments, and settlements. They just respond to completely different types of claims. A business with only EL coverage and no EPLI has significant exposure.

Adding General Liability to the Picture

That EL-vs-EPLI distinction becomes clearer when you add general liability to the picture. GL covers bodily injury or property damage claims filed by third parties — customers, vendors, visitors — not employees.

EL fills the specific gap between workers' comp (covers employees, no-fault) and general liability (covers non-employees). Without it, employee negligence lawsuits that pierce the exclusive remedy doctrine leave your business fully exposed to defense costs and judgments with no policy to respond.

Understanding Policy Limits and Exclusions

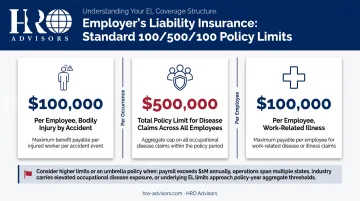

How the Standard 100/500/100 Limits Work

According to SFM, the basic EL limit is typically structured as $100,000 / $500,000 / $100,000. Here's what each number means:

- $100,000 — Maximum per employee for bodily injury by accident

- $500,000 — Total policy limit for disease-related claims across all employees

- $100,000 — Maximum per employee for work-related illness

A practical example: if three employees file EL claims in the same policy year following separate accidents, each claim is capped at $100,000 — but the policy limit also constrains total disease payouts across all employees at $500,000.

Common Exclusions to Know Before a Claim Occurs

Beyond employment practices claims, the NCCI form also excludes:

- Obligations already imposed by workers' comp, occupational disease, or disability laws

- Punitive damages from illegal employment practices

- Claims outside U.S. territory (in most standard forms)

- Contractually assumed liability not otherwise covered

Knowing where your policy stops is just as important as knowing what it covers — and that awareness shapes the limits conversation directly.

When to Increase Limits or Add an Umbrella Policy

The standard 100/500/100 limits may be insufficient for many businesses. NCCI's 2025 State of the Line data shows lost-time claim severity increased 6% in Accident Year 2024 — serious injury claim costs keep climbing, and default limits don't automatically adjust.

Higher EL limits — $500,000 or $1,000,000 — are available from most carriers. A commercial umbrella policy can add $1M to $15M on top. How much you need depends on:

- Industry risk level (construction and manufacturing carry higher exposure than consulting)

- Total employee headcount

- Company assets at risk in a judgment

What Determines Your Employers Liability Insurance Costs?

EL coverage is priced as part of the broader workers' comp program, so the same factors that drive comp costs drive EL costs.

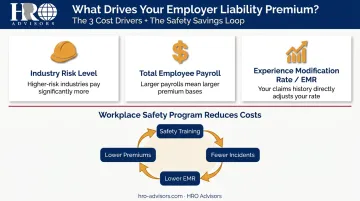

Three Primary Cost Drivers

1. Industry risk level Higher-risk classifications — construction, manufacturing, healthcare — carry more exposure and pay more than lower-risk classifications like professional services or technology firms. BLS data for 2024 provides industry-specific nonfatal injury incidence rates that reflect this risk spread.

2. Total employee payroll Payroll is the base exposure measure for workers' comp and EL pricing. More employees doing more work means more potential for claims.

3. Experience Modification Rate (EMR) NCCI's experience rating system compares an employer's actual losses against expected losses for similar businesses. A low EMR signals strong safety performance and translates directly into lower premiums — it functions like a credit score for workplace safety.

State Legal Climate

Businesses in states with higher litigation activity or plaintiff-friendly legal environments typically pay more for liability coverage. This isn't a fixed cost driver, but it's a real one — raise this with a broker when comparing coverage options.

The Long-Term Value of Workplace Safety Programs

What you can control is claim frequency. Proactive safety programs reduce incidents, which improves EMR over time, which lowers premiums — a compounding benefit that grows with consistency. Core program elements include:

- Regular employee safety training

- Scheduled equipment inspections

- Documented incident reporting protocols

OSHA's Safety Pays program puts hard numbers to this relationship, illustrating how injury prevention directly improves business profitability. Fewer claims is both a safety outcome and a financial strategy.

How to Obtain Employers Liability Coverage

The Most Common Path: Part of Your Workers' Comp Policy

For most employers, EL coverage isn't a separate purchase. It's automatically included as Part Two of a standard workers' comp policy bought through a private insurer. When you purchase workers' comp, you generally get EL alongside it.

The exception: businesses in North Dakota, Ohio, Washington, and Wyoming must purchase stop-gap coverage separately from a private carrier, since their state funds only provide workers' comp benefits.

Standalone EL policies also exist in the market for businesses that need coverage outside a workers' comp program.

What to Evaluate When Choosing Coverage

- Match limits to your risk profile — Standard 100/500/100 may be adequate for a low-risk consulting firm; a manufacturing company with 200 employees likely needs higher limits

- Review exclusions carefully — Understand exactly what your policy won't cover before a claim happens

- Consider an umbrella policy — For businesses with significant assets or elevated exposure, umbrella coverage above the standard EL limits is worth the added premium

- Factor in state requirements — Especially if you operate across multiple states, including any of the four monopolistic states

How a PEO Can Help

For small and mid-size businesses, a practical option for accessing competitive workers' comp and EL coverage is through a Professional Employer Organization (PEO). PEOs co-employ your workforce under a master policy, pooling risk across many businesses and unlocking coverage terms a small company typically can't access alone. NAPEO confirms that PEOs provide professional loss control and claims management as part of their co-employment model.

That said, coverage structures, safety programs, and claims handling vary significantly between PEO providers — which makes side-by-side comparison important before committing.

HRO Advisors helps businesses compare 3 to 8 PEO providers at no cost. Their process covers a free consultation, cost and coverage analysis across 500+ PEOs, and direct negotiation with providers — typically completed in under two weeks. HRO Advisors is compensated by the provider you select, not by you. For businesses in high-risk industries like manufacturing or construction, where workers' comp and EL costs are a real budget line, access to better-negotiated rates can add up quickly.

Frequently Asked Questions

What is employer liability coverage?

Employers liability insurance is Part Two of a standard workers' comp policy. It protects the employer when an employee files a lawsuit over a work-related injury or illness that falls outside workers' comp's exclusive remedy — covering legal defense costs, settlements, and court judgments.

How much employer's liability coverage do I need?

The standard starting point is 100/500/100 limits, but the right amount depends on your industry, employee count, and total business assets. Many businesses in construction, manufacturing, or healthcare increase limits to $500,000 or $1,000,000, or add a commercial umbrella policy for additional protection.

Is employers liability insurance required by law?

A standalone EL policy isn't legally required in most states — it's automatically included with a standard workers' comp policy. However, businesses in North Dakota, Ohio, Washington, and Wyoming must purchase stop-gap coverage separately from a private insurer, since their state funds don't include EL.

What is the difference between employers liability and EPLI?

EL insurance covers lawsuits tied to physical workplace injuries or illnesses. EPLI covers employment-related legal claims — wrongful termination, discrimination, harassment, and retaliation. They respond to entirely different risks and neither substitutes for the other.

Can a PEO help my business manage employers liability coverage?

Yes. PEOs typically include workers' comp and EL coverage under their master policies, alongside loss control services and claims management support. HRO Advisors compares 3 to 8 PEO options for your business at no cost, helping you find the right risk management fit for your industry and workforce size.