Key Takeaways

- Small businesses with 1–50 FTEs qualify for the small group health insurance market but aren't federally required to offer coverage

- PPOs are the most common plan type at small firms, covering 44% of enrolled workers in 2025

- Small-firm single coverage averages $9,211 annually ($768/month); family coverage averages $26,054 ($2,171/month)

- Businesses with under 25 FTEs can qualify for a tax credit worth up to 50% of premium contributions

- PEO partnerships give small businesses access to large-group health plan pricing not available on the open market

What Is Small Business Group Health Insurance?

Small business group health insurance is a health plan an employer purchases to cover employees — and often their dependents — where premium costs are shared between the employer and employees. Unlike individual coverage, the risk is spread across all enrolled members, which affects pricing and plan design.

Who qualifies as a "small group"? Under the ACA, a small employer is defined as a business with 1–50 full-time equivalent employees (FTEs). Four states — California, Colorado, New York, and Vermont — expanded their small group threshold to 1–100 employees, so your state's definition may differ from the federal baseline.

Three rules govern how this market works:

- Businesses under 50 FTEs are not subject to the ACA employer mandate — meaning no federal penalty for not offering coverage

- The SHOP Marketplace (the federal small business exchange) is available to employers with 1–50 FTEs in most states

- Coverage must be offered to all employees working 30 or more hours per week, along with their dependents

Small group coverage doesn't automatically mean higher premiums than large group plans. KFF's 2025 Employer Health Benefits Survey shows small-firm single premiums ($9,211) are nearly identical to large-firm premiums ($9,361). The real gap shows up in deductibles ($2,631 average for small firms vs. $1,670 for large firms) and the employee share of family premiums (36% vs. 23%).

Types of Small Business Group Health Insurance Plans

Four main plan structures dominate the small group market. Each makes different trade-offs between cost, network flexibility, and how employees access care.

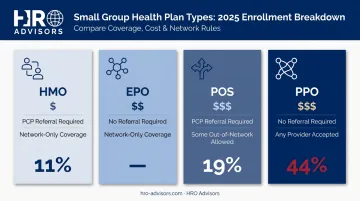

PPO Plans (Preferred Provider Organization)

PPOs let employees see any provider — in-network at lower cost, out-of-network at higher cost — without needing a referral. No gatekeeper, no required primary care physician (PCP).

That flexibility comes at a price: PPOs carry higher premiums than most alternatives. Still, they're the most popular option. According to KFF's 2025 data, 44% of covered workers at small firms are enrolled in PPOs — far ahead of any other plan type.

HMO Plans (Health Maintenance Organization)

HMOs require employees to select a PCP who coordinates all care, including referrals to specialists. Coverage is generally limited to the plan's provider network (emergencies excepted).

The trade-off is lower premiums and out-of-pocket costs. For budget-conscious small employers, HMOs are worth serious consideration — especially if the workforce is concentrated in one geographic area with a strong HMO network nearby. Only 11% of small-firm workers were in HMOs in 2025, but for cost-sensitive employers, they often represent the best value.

EPO and POS Plans

These two plan types occupy the middle ground:

- EPO (Exclusive Provider Organization): Network-only coverage like an HMO, but no referral required to see a specialist. Good for employees who want some independence without the PPO price tag.

- POS (Point of Service): A hybrid requiring a PCP referral for specialists but allowing some out-of-network access. POS plans accounted for 19% of small-firm enrollment in 2025.

Both are worth evaluating when your workforce is concentrated in an area with strong specialist networks, or when you want to balance cost and flexibility.

Beyond plan structure, some small employers also explore group purchasing arrangements as a way to access better pricing.

Association Health Plans (AHPs)

AHPs allow small businesses in the same industry or region to pool together and purchase coverage as a larger group. The appeal is straightforward: larger pools can mean better pricing and more favorable terms.

AHPs are legally constrained, however. The DOL's 2018 rule expanding AHP access was largely struck down in 2019, and the DOL formally rescinded the rule effective July 1, 2024. AHPs still exist under pre-2018 frameworks, but they're more limited in scope. If you're considering an AHP, verify it complies with current federal and state law before enrolling.

How Much Does Small Business Group Health Insurance Cost?

What Drives Your Premium

Five factors determine what small businesses pay for group coverage:

- Employee age — The most influential variable. ACA rules allow insurers to charge older enrollees up to 3 times the rate charged to younger ones

- Geographic location — Healthcare costs vary considerably by region; rural markets often differ significantly from urban ones

- Plan type — PPOs cost more than HMOs; higher metal tiers (Gold, Platinum) carry higher premiums but lower cost-sharing

- Tobacco use — Insurers can charge tobacco users up to 50% more than non-users

- Group size — Smaller pools carry more pricing volatility

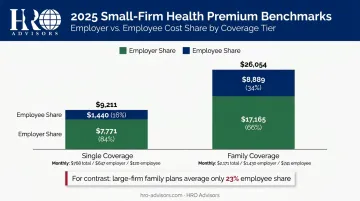

2025 Cost Benchmarks

Based on KFF's 2025 Employer Health Benefits Survey (small firms defined as 10–199 workers):

| Coverage | Total Annual Premium | Employer Pays | Employee Pays | Monthly Total |

|---|---|---|---|---|

| Single | $9,211 | $7,771 (84%) | $1,440 (16%) | ~$768 |

| Family | $26,054 | $17,165 (66%) | $8,889 (34%) | ~$2,171 |

Note that small-firm workers carry a significantly higher share of family premiums — 36% — compared to 23% at large firms. For employees weighing whether to add dependents, that 13-point difference is often the deciding factor.

The PEO Advantage on Cost

Through the co-employment model, a Professional Employer Organization (PEO) pools your employees into its much larger workforce — giving small businesses access to group health plan pricing that's otherwise reserved for companies with hundreds or thousands of employees.

That means coverage through major carriers like Aetna, Blue Cross Blue Shield, and UnitedHealthcare at rates most small firms can't negotiate independently. HRO Advisors offers a free comparison service that evaluates up to 8 PEOs side-by-side, so you can assess plan quality and actual costs before making any commitment.

Eligibility Requirements and Participation Rules

Federal Eligibility Basics

To access the small group market, your business generally needs:

- 1–50 FTEs (the federal threshold; some states go to 100)

- At least one non-owner employee enrolled — business owners alone don't constitute a group

- Coverage offered to all employees working 30+ hours per week

Minimum Participation Requirements

Most carriers won't issue a group policy without a minimum percentage of eligible employees enrolled. For SHOP Marketplace plans, CMS sets this at 70% in most states. Outside SHOP, carriers set their own thresholds — typically 70–75%.

Employees who decline coverage because they're already covered elsewhere — on a spouse's plan, for example — typically don't count against your participation threshold.

SHOP also offers a special enrollment window from November 15 to December 15 each year where businesses can enroll even if they haven't met the participation requirement.

Waiting Periods and Special Enrollment

- Employers can impose a waiting period of up to 90 days before a new hire's coverage begins

- Employees can join the plan mid-year during a special enrollment period triggered by qualifying life events: marriage, birth of a child, loss of other coverage, etc.

Essential Health Benefits

All ACA-compliant small group plans must cover 10 mandated benefit categories:

- Ambulatory patient services

- Emergency services

- Hospitalization

- Maternity and newborn care

- Mental health and substance use disorder services

- Prescription drugs

- Rehabilitative and habilitative services

- Laboratory services

- Preventive and wellness services

- Pediatric services (including oral and vision care)

Insurers cannot deny coverage or impose exclusions based on pre-existing conditions.

Tax Benefits and ACA Compliance

Who the Employer Mandate Actually Covers

Businesses with fewer than 50 FTEs are not subject to the ACA employer mandate. Only Applicable Large Employers (ALEs) — those averaging 50+ full-time employees — face penalties for failing to offer affordable minimum essential coverage. For 2026, those penalties reach $3,340 per full-time employee under Section 4980H(a), or $5,010 per employee who receives a premium tax credit under Section 4980H(b).

If you're under 50 FTEs, the mandate doesn't apply — but the tax advantages of offering coverage can still make a meaningful difference to your bottom line.

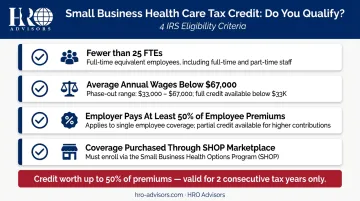

The Small Business Health Care Tax Credit

Qualifying employers can claim a credit worth up to 50% of premium contributions (35% for tax-exempt employers). Eligibility requires all of the following:

- Fewer than 25 FTEs

- Average annual wages below $67,000 (the credit phases in above $33,000 and disappears entirely at $67,000)

- Employer contributes at least 50% of employees' individual premiums

- Coverage purchased through the SHOP Marketplace

The credit applies for two consecutive tax years only, so if you're eligible now, act before that window closes.

Additional Tax Advantages

Beyond the tax credit, two more deductions apply to most small businesses offering group coverage:

- Premium deductibility — Employer contributions toward health premiums are generally deductible as a business expense under IRS Publication 535

- Pre-tax employee contributions — Under a Section 125 cafeteria plan, employees pay their share of premiums with pre-tax dollars, reducing their taxable income and lowering your payroll tax liability simultaneously

How to Find the Right Group Health Plan

Your Purchasing Options

Small businesses can buy group health coverage through three main channels:

- Direct from a carrier — Straightforward but limits you to one carrier's offerings

- Licensed insurance broker — Access to multiple carriers with professional guidance

- SHOP Marketplace — The federal small business exchange; required if you want the Small Business Health Care Tax Credit

The PEO Route

Partnering with a PEO gives small businesses access to something standalone group policies rarely offer: large-group buying power. Rather than purchasing your own small group policy, your employees join the PEO's master health plan — opening up broader carrier options and built-in ACA, ERISA, and COBRA compliance support.

HRO Advisors provides a free PEO comparison service that evaluates up to 8 providers side-by-side across plan quality, pricing, compliance, and workforce fit. HRO Advisors is compensated by the selected provider, so there's no cost to you.

Four Practical Shopping Tips

- Confirm the carrier is licensed in your state — insurance is state-regulated, and authorization varies by market

- Check that employees' preferred doctors and local hospitals are in-network before committing to a plan

- Look beyond the monthly premium: deductibles, copays, and out-of-pocket maximums shape the real cost of coverage

- Ask about prior-year rate increases so you can anticipate what renewal looks like in year two and beyond

Frequently Asked Questions

How much does small business group health insurance cost?

According to KFF's 2025 Employer Health Benefits Survey, small-firm coverage averages roughly $768/month for single coverage and $2,171/month for family coverage in total premiums. Employers typically cover at least 84% of single premiums and about 66% of family premiums, though actual costs vary by business size, location, and plan type.

What is a small group in health insurance?

A small group is generally a business with 1–50 full-time equivalent employees under federal ACA guidelines. California, Colorado, New York, and Vermont use a 1–100 threshold instead. Your state's definition determines which market rules and plan options apply when you shop for coverage.

Can small businesses join together for group health insurance?

Yes — through Association Health Plans (AHPs), small businesses in the same industry or region can pool together to purchase coverage as a larger group. However, AHP regulations tightened significantly after 2019 court rulings and a 2024 federal rule rescission. Confirm any AHP complies with current federal and state requirements before enrolling.

What is the best health insurance for small business owners?

It depends on your budget and workforce. PPOs offer the most provider flexibility, while HMOs cost less with more predictable out-of-pocket expenses. PEO-sponsored health plans are worth considering too — they can unlock large-group rates unavailable in the standard small group market.

Are small businesses required to offer group health insurance?

Businesses with fewer than 50 FTEs are not legally required by the ACA to offer health insurance. Businesses with 50+ FTEs face penalties if they don't offer affordable minimum essential coverage. Even without a legal obligation, offering coverage remains one of the most effective tools for attracting and retaining employees.

What tax benefits do small businesses get for offering health insurance?

Employer premium contributions are generally tax-deductible as a business expense. Businesses with under 25 FTEs that meet wage and contribution thresholds can also claim the Small Business Health Care Tax Credit — worth up to 50% of premium contributions for plans purchased through the SHOP Marketplace.