The challenge isn't finding a carrier. It's finding the right one. Not all major insurers offer the same depth of employer-focused group coverage, and factors like your workforce's geographic spread, your company's size, and whether you need fully-insured or self-funded options all determine which carrier actually fits.

This guide evaluates the top ACA-compliant group health insurance carriers for employers, breaks down what ACA compliance actually requires, and explains how employers of all sizes — including those under 50 FTEs — can access enterprise-level group coverage.

Key Takeaways

- ACA-compliant group plans must satisfy three federal requirements: minimum essential coverage, minimum value (60% actuarial value), and current IRS affordability standards

- The leading national carriers for employer group coverage are UnitedHealthcare, BlueCross BlueShield, Aetna, Cigna, and Kaiser Permanente

- Carriers differ meaningfully in geographic reach, plan type variety, and built-in compliance tools

- Small employers under 50 FTEs aren't subject to the ACA mandate but can still access Fortune 500-level group plans through a PEO

- Choosing the right carrier comes down to employee locations, company size, and funding preference

What Makes a Group Health Plan ACA-Compliant for Employers?

ACA compliance for employer-sponsored group health coverage involves a set of overlapping requirements that Applicable Large Employers (ALEs) must satisfy each plan year — and falling short on any one of them can trigger significant penalty exposure.

The Three Core Requirements

1. Minimum Essential Coverage (MEC) The plan must qualify as MEC — meaning it covers basic health services and is offered to at least 95% of full-time employees and their dependents. Failing this threshold triggers the 4980H(a) penalty exposure.

2. Minimum Value According to IRS guidelines, a plan provides minimum value if it covers at least 60% of total allowed costs and includes substantial inpatient hospitalization and physician services. Plans below this threshold expose ALEs to 4980H(b) penalties.

3. Affordability The employee's self-only premium cannot exceed a set percentage of household income. The IRS adjusts this threshold annually:

| Plan Year | Affordability Threshold |

|---|---|

| 2024 | 8.39% |

| 2025 | 9.02% |

| 2026 | 9.96% |

Additional Large-Group Rules to Know

Beyond the three core requirements, large-group plans face additional federal rules that affect plan design and carrier selection:

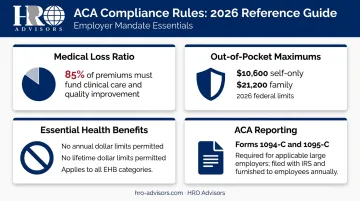

- Medical Loss Ratio (MLR): Large-group insurers must spend at least 85% of premiums on claims and quality improvement

- Out-of-pocket maximums: For 2026, limits are $10,600 (self-only) and $21,200 (other coverage)

- Essential Health Benefits (EHBs): Large-group and self-funded plans are not required to cover all 10 EHBs — but they cannot impose annual or lifetime dollar limits on any EHBs they do choose to cover

- ACA reporting: ALEs must file Forms 1094-C and 1095-C annually to document offers of coverage to full-time employees

Self-insured plans face fewer ACA market reforms than fully-insured plans, but they're not exempt. They must still satisfy minimum value, preventive care mandates, and EHB dollar limit rules — a distinction that matters when evaluating whether self-funding makes sense for your organization.

Best ACA-Compliant Group Health Insurance Carriers for Employers

Carriers below were selected based on their availability for employer-sponsored group coverage, plan type diversity, financial stability, and the quality of employer-facing compliance tools. Use the summaries and tables to match each carrier's strengths against your workforce size, geographic footprint, and compliance priorities.

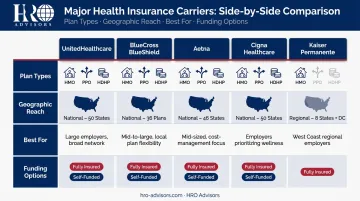

UnitedHealthcare

UnitedHealthcare is one of the largest commercial health insurers in the U.S. by total enrollment, serving over 235,000 employers with both fully-insured and self-funded group health plan options. For HR teams managing ACA compliance, UHC's dedicated employer portal provides compliance reporting tools that support 1095-B and 1094-B filings ; though for self-funded (ASO) plans, 1095-C preparation remains the employer's responsibility.

Its plan portfolio spans several structured network options including Choice, Choice Plus, Navigate, Charter, NexusACO, and Surest , covering the range from broad PPO-style access to tighter managed network designs and HDHP/HSA-compatible structures.

| UnitedHealthcare | |

|---|---|

| Plan Types | Open access, preferred-provider, HDHP/HSA-compatible, and high-deductible options; both fully insured and self-funded |

| Geographic Reach | Broad national availability; small-business digital store in most states with quote support for AK, HI, NV, and VT |

| Best For | Mid-to-large employers (50+ FTEs) needing multi-state coverage and ACA compliance reporting support |

BlueCross BlueShield (BCBS Network)

BCBS isn't a single national insurer : it's a federation of 33 independent, locally operated companies that operate under the Blue brand. That distinction matters for employers: you get local carrier expertise combined with national network access through the BlueCard PPO program, which connects members to over 2.2 million in-network providers across all 50 states.

For employers with employees spread across multiple states, this structure is hard to match. Each regional BCBS company provides state-specific ACA compliance support, while the BlueCard program ensures consistent in-network access regardless of where employees live or travel.

| BlueCross BlueShield | |

|---|---|

| Plan Types | PPO, EPO, HMO, POS, and HDHP; fully insured and administrative services for self-insured employers |

| Geographic Reach | All 50 states through the BCBS federation; BlueCard enables cross-carrier national network access |

| Best For | Employers with geographically distributed workforces needing consistent in-network coverage nationwide |

Aetna (CVS Health)

Now part of CVS Health, Aetna brings a distinct operational advantage: integration with over 900 MinuteClinic locations nationwide, where covered services may be available at no or low cost depending on plan design. That integration extends to pharmacy cost management , useful for employers focused on controlling total healthcare spend rather than just premium costs.

Aetna offers a national group health portfolio for employers ranging from small businesses to large enterprises, with fully-insured and administrative services options. Its employer tools support ACA compliance tracking and cost containment.

| Aetna (CVS Health) | |

|---|---|

| Plan Types | HMO, PPO, EPO, HDHP, and indemnity plans; fully insured and ASO structures |

| Geographic Reach | National portfolio for employer group plans; specific state availability for fully insured plans varies (verify directly) |

| Best For | Employers prioritizing pharmacy integration, MinuteClinic access, and streamlined ACA compliance documentation |

Cigna Healthcare / Evernorth

Cigna operates its employer medical plans under Cigna Healthcare, while Evernorth Health Services provides health services and pharmacy benefits for employers and health plans ( these are distinct entities under the same parent company).

Cigna's employer group plans include Open Access Plus and EPO structures, with particular depth in behavioral and mental health programs. Mental health parity compliance is a growing ACA-adjacent concern for employers, and Cigna's extensive behavioral health provider network addresses this directly. For employers with international workforces, Cigna Global offers dedicated international health plan options with 24/7 support.

| Cigna Healthcare | |

|---|---|

| Plan Types | Open Access Plus, EPO, HDHP/HSA, and other employer-sponsored plan structures; fully insured and self-funded |

| Geographic Reach | Available across most U.S. states for employer group plans; verify state footprint for small vs. large group markets |

| Best For | Mid-to-large employers prioritizing behavioral health coverage, mental health parity compliance, and global workforce needs |

Kaiser Permanente

Kaiser operates differently from every other carrier on this list. It's an integrated managed care organization, meaning it owns its care delivery network and combines insurance with healthcare delivery under one roof. Permanente Medical Groups deliver care; Kaiser's health plan finances it. That structure typically means lower administrative friction and more competitive premium pricing.

Kaiser's employer plans for large groups include HMO, Deductible HMO, and HDHP structures, all network-only with no out-of-network coverage except emergencies. Quality ratings are strong: Kaiser Foundation Health Plan, Inc. (Southern California) earned a 5.0 out of 5.0 from NCQA as of June 2026.

The trade-off is geography. Kaiser operates in 8 states and Washington, D.C. : California (North and South), Colorado, Georgia, Hawaii, Maryland/Virginia/DC, Oregon/SW Washington, and Washington state. Employers with employees outside these regions need a different primary carrier.

| Kaiser Permanente | |

|---|---|

| Plan Types | HMO, Deductible HMO, HDHP; integrated care model, network-only |

| Geographic Reach | 8 states and Washington, D.C. only; not viable for employers with employees outside Kaiser's service regions |

| Best For | Employers in Kaiser service areas seeking competitive premium group plans with high preventive care scores |

How to Choose the Right ACA-Compliant Carrier

What the Evaluation Should Cover

Carrier selection for employer-sponsored group coverage should go beyond brand recognition or the lowest quoted premium. The most critical evaluation criteria:

- Network adequacy — Are your employees' current doctors and preferred hospitals in-network? Out-of-network care inflates employee cost-sharing and creates dissatisfaction with benefits

- Plan type flexibility — Do you need HMO cost controls, PPO flexibility, or HDHP/HSA pairing?

- Compliance tools — Does the carrier support ACA reporting for ALEs, including 1095-C documentation for self-funded plans?

- Geographic fit — Does the carrier's network cover every state where your employees live and work?

- Financial stability — Review the carrier's financial strength ratings before committing to a multi-year relationship

The Common Mistake Employers Make

Many employers default to the carrier with the lowest renewal premium — then discover mid-year that key specialists or hospital systems are out of network. Employees absorb higher out-of-pocket costs, and HR absorbs the complaints. Checking network adequacy before signing prevents both problems.

A Practical Route for Smaller Employers

Employers under 50 FTEs aren't subject to the ACA employer mandate, but that doesn't mean they're stuck with limited coverage options. According to NAPEO research, nearly two-thirds of PEO clients have 10–49 employees — and 26% of new PEO clients added health benefits after starting their PEO relationship.

Through a Professional Employer Organization, small employers pool their workforce with other businesses. That pooling unlocks group health plans from carriers like Aetna, BlueCross BlueShield, and UnitedHealthcare at rates that aren't typically available to companies their size.

HRO Advisors helps businesses compare up to 8 PEOs side-by-side at no cost. The service is free to employers, with HRO Advisors compensated by the selected provider.

Conclusion

The right ACA-compliant group health carrier depends on three things: where your employees are, what plan structures work for your workforce, and whether you have the compliance infrastructure to satisfy ACA reporting obligations as your company grows.

None of the five carriers covered here is universally the best choice. UHC and BCBS lead on national reach. Aetna brings pharmacy integration. Cigna addresses behavioral health depth. Kaiser wins on integrated care quality within its regions. The carrier that fits a 50-person tech company in California looks very different from what works for a 200-person manufacturer operating across six states.

That's why carrier selection isn't a one-time decision. Revisit your choice at every renewal cycle — workforce demographics shift, business locations change, and the ACA affordability threshold adjusts annually. A plan that was compliant and cost-effective in 2024 may need re-evaluation for 2026.

HRO Advisors helps employers match with PEOs that carry vetted, ACA-compliant group health plans from carriers like those covered in this guide. The consultation is free and comes with no obligation — contact HRO Advisors at 866-755-0288 or info@hro-advisors.com to compare options side by side.

Frequently Asked Questions

Which ACA-compliant group health insurance carriers are best for employers?

The leading national carriers for employer group coverage are UnitedHealthcare, BlueCross BlueShield, Aetna, Cigna Healthcare, and Kaiser Permanente. The best fit depends on your company size, geographic footprint, and whether you need a fully-insured or self-funded group plan structure.

Who is the largest ACA-compliant health insurance carrier for employers?

UnitedHealthcare is among the largest commercial health insurers by total enrollment, serving over 235,000 employers with group health plans across the U.S. KFF's large-group market data also ranks Kaiser Foundation Group prominently by large-group enrollment, so "largest" varies by market segment.

Can employees get ACA Marketplace coverage if their employer offers group health insurance?

Generally, no. If the employer-sponsored plan meets ACA minimum value and affordability standards, employees are not eligible for Marketplace premium tax credits. However, if the employer's plan fails either test — or is deemed unaffordable — the employee may qualify for Marketplace subsidies.

What is the ACA employer mandate and which businesses does it apply to?

The Employer Shared Responsibility Provision applies to Applicable Large Employers (ALEs), defined as businesses averaging 50 or more full-time equivalent employees in the prior calendar year. ALEs must offer affordable, minimum-value health coverage to at least 95% of full-time staff or face IRS penalties under Section 4980H.

What makes a group health insurance plan ACA-compliant for employers?

Three requirements apply: the plan must provide minimum essential coverage (MEC), cover at least 60% of average allowed costs (minimum value), and meet the IRS affordability threshold — 9.02% for 2025, 9.96% for 2026. Large-group plans also cannot impose annual or lifetime dollar limits on covered benefits.

How can small employers access top ACA-compliant group health insurance carriers?

Small employers under 50 FTEs can access enterprise-level group health plans from major national carriers by partnering with a PEO. PEOs pool employees across multiple businesses to negotiate group rates and coverage options that smaller companies typically can't access on their own. HRO Advisors matches employers with up to 8 PEOs at no cost.