Benefits administration outsourcing addresses this directly: it's the practice of contracting a third-party provider to manage some or all of these functions on your behalf. This guide covers what's included, the two primary outsourcing models, the real benefits and drawbacks, and how to evaluate the right partner.

The scale of adoption signals how widespread this need has become. According to ADP's Benefits Administration white paper, 80% of mid-sized employers and 91% of large employers say outsourcing at least some benefits administration provides genuine value — and 88% and 92% respectively report that their providers met or exceeded expectations.

Key Takeaways

- Outsourcing can be partial (COBRA, ACA compliance) or comprehensive (full benefits management via PEO or ASO)

- PEOs give small businesses access to Fortune 500-level health plans through group purchasing power

- NAPEO estimates $1,775 in annual savings per employee when using a PEO

- ACA non-compliance penalties reach $3,340–$5,010 per employee in 2026

- HRO Advisors compares up to 8 PEO providers side-by-side at no cost to your business

What Is Benefits Administration Outsourcing?

Definition and Scope

Benefits administration outsourcing is an arrangement where an employer contracts a third-party organization to manage some or all employee benefits functions — from enrollment and eligibility to compliance filings and employee communications. The employer retains legal accountability for the employment relationship, though this depends on the model chosen.

Outsourcing doesn't have to be all-or-nothing. Most employers start selectively:

- Highly outsourced functions (60–75% of mid-sized companies): COBRA, FSA administration, 401(k)

- Partially outsourced: Open enrollment support, ACA filing, carrier billing reconciliation

- Fully outsourced: Entire benefits administration handed to a PEO or comprehensive ASO

The right scope depends on your company's size, internal HR capacity, and how complex your benefits program has become.

What Services Are Typically Included?

A full-scope benefits administration outsourcing arrangement generally covers:

- Eligibility and enrollment management — adding/removing employees, life event changes

- Open enrollment support — employee communications, enrollment workflows, deadline management

- ACA compliance filing — 1094/1095 reporting, employer mandate tracking

- COBRA administration — required notices, election and payment processing, coverage terminations

- Carrier billing reconciliation — auditing invoices against enrollment data

- Dependent verification — audits that typically remove 3–7% of ineligible dependents, saving roughly $4,500 per year per removed individual

- Spending account administration — FSA, HSA, HRA management

- Employee benefits communications — benefit guides, targeted awareness campaigns

Two Common Outsourcing Models — TPA vs. PEO

Third-Party Administrator (TPA): A vendor that handles specific administrative tasks — claims processing, enrollment, compliance reporting — on behalf of the employer. The employer retains employer of record status and full control over plan design and vendor relationships. TPAs are suited for companies that want targeted help without changing their employment structure.

Professional Employer Organization (PEO): A co-employment arrangement where the PEO becomes the employer of record for HR and benefits purposes, bundling benefits administration with payroll, workers' comp, and HR compliance under one contract.

For small and mid-sized businesses, this model's biggest advantage is purchasing power. The PEO's pooled workforce gives every client access to plan options and pricing that a standalone employer of 50 or 100 people simply can't negotiate on their own.

Administrative Services Organization (ASO): A middle-ground model that lets businesses outsource specific HR functions without entering a co-employment arrangement. Companies keep full workforce control while reducing their administrative load — no co-employment required.

Which model fits depends on how much control you want to retain and how much you need to offload. A PEO broker can compare all three options side-by-side so you're not guessing.

Key Benefits of Outsourcing Benefits Administration

Reduced Administrative Burden

The most immediate payoff is time. Benefits administration involves constant data entry, eligibility verification, carrier reconciliation, and compliance tracking. These tasks aren't complex individually — they're just endless. Outsourcing removes them from your HR team's plate, freeing capacity for work that actually moves the business forward: retention programs, manager training, workforce planning.

It also cuts the error rate. Manual processing creates problems that are expensive to fix and can expose the company to compliance risk:

- Data mismatches between payroll and carrier systems

- Missed COBRA notices that trigger per-day penalties

- Enrollment gaps that leave employees without coverage

Access to Enterprise-Level Benefits and Negotiating Power

This is the benefit that surprises most business owners. A PEO pools employees from hundreds or thousands of client companies, presenting insurers with a workforce large enough to qualify for large-group pricing.

The practical result:

- Small businesses gain access to health plans typically reserved for corporations with thousands of employees

- Carriers like Aetna, Blue Cross Blue Shield, and UnitedHealthcare offer more competitive rates to PEOs than to individual small employers

- For companies with 10–49 employees, 52% of PEO users offer retirement plans versus just 23% of non-users, according to NAPEO's industry research

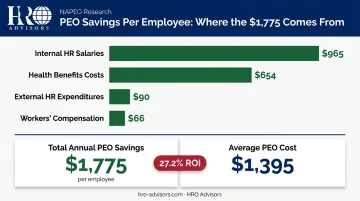

NAPEO's ROI study estimates $654 per employee per year in health benefits savings as one component of total PEO cost savings.

Significant Cost Savings on HR Operations

NAPEO's ROI study puts total PEO savings at $1,775 per employee annually, against an average PEO cost of $1,395 per worksite employee — a 27.2% ROI from cost savings alone.

The savings break down across four categories:

| Category | Annual Savings per Employee |

|---|---|

| Internal HR salaries | $965 |

| Health benefits costs | $654 |

| External HR expenditures | $90 |

| Workers' compensation | $66 |

| Total | $1,775 |

HRO Advisors' clients report savings of up to 40% on overall HR costs — a figure driven by competitive negotiation across their network of 500+ PEO providers, not just the cost of the PEO itself.

Compliance Expertise and Reduced Legal Risk

Benefits regulations are both complex and unforgiving. The penalties for getting it wrong:

- ACA employer shared responsibility (2026): $3,340 per full-time employee under 4980H(a); $5,010 per employee under 4980H(b)

- COBRA violations: $100 per day per qualified beneficiary, with a minimum $2,500 after examination notice

- ERISA: The DOL's Employee Benefits Security Administration recovered $1.4 billion in FY2025, including 62 indictments and 45 criminal convictions

Outsourcing partners — especially PEOs — maintain dedicated compliance teams that monitor regulatory changes, manage ACA filings, send required COBRA notices on time, and assume shared compliance liability. That shared liability means regulatory exposure shifts away from your company and toward a team built specifically to manage it.

Scalability as the Business Grows

Hiring in a new state means new payroll tax registrations, different workers' comp requirements, and potentially new benefits compliance obligations. Building internal HR capacity to handle each growth phase is expensive and slow.

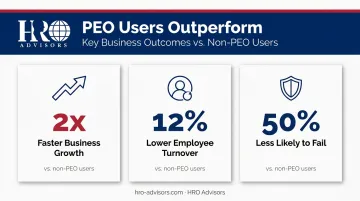

A PEO or ASO absorbs that complexity automatically. NAPEO data shows that businesses using PEOs grow 2x faster, experience 12% lower employee turnover, and are 50% less likely to go out of business than comparable non-users.

Potential Drawbacks to Consider

No outsourcing model is without tradeoffs. Three risks deserve honest attention:

Reduced direct control. Delegating benefits communications, vendor relationships, and plan changes to an external party means some decisions happen at a distance. Business leaders accustomed to hands-on involvement can find this frustrating when plan details need to change quickly. Look for a provider with transparent reporting dashboards and a dedicated account contact who owns your relationship end-to-end.

Impersonal employee experience. Some providers route employees through generic call centers staffed by agents unfamiliar with your plan design. A denied claim or missed COBRA notice handled poorly erodes trust fast. SHRM notes that PEO drawbacks include high staff turnover on provider teams and communication bottlenecks.

Before signing, ask specifically how employee issues are handled and escalated — and get the answer in writing.

Transition challenges. Moving from in-house administration — or switching between providers — involves data migration, employee communication, and a real learning curve. Plan transitions well outside of open enrollment season when possible, and confirm the prospective provider has a structured onboarding process with clear milestones and data validation checkpoints.

How to Choose the Right Benefits Administration Outsourcing Partner

Evaluate Industry Experience and Size Fit

Not every provider serves every industry effectively. A PEO experienced with manufacturing will understand OSHA obligations and multi-shift workforce dynamics. One that specializes in healthcare will be fluent in HIPAA. Always ask for client references in your specific sector.

Size matters too. NAPEO's 2025 data shows that 50% of PEO clients have 10–49 employees and 14% PEO penetration among employers with 20–499 employees — confirming this market is designed for smaller, growing businesses, not enterprise HR departments.

Assess Technology and Integration Capabilities

The provider's platform needs to work with what you already have. Confirm:

- Integration with your existing payroll and HRIS systems

- Employee self-service enrollment portal (mobile-accessible)

- Real-time reporting dashboards for HR and finance leadership

- Automated carrier data feeds to reduce manual reconciliation

Review Compliance Track Record and SLA Commitments

Ask for specifics, not generalities. Key questions to ask every provider:

- How do you monitor and communicate regulatory changes?

- What is your error-correction process when enrollment mistakes occur?

- What SLA terms govern enrollment accuracy and response times?

ESAC accreditation and IRS Certified PEO (CPEO) status are worth confirming as independent quality markers for any PEO you're evaluating.

Examine the Service Model: Dedicated Support vs. Call Center

A dedicated account team that knows your benefits structure produces measurably better outcomes than a generic help desk. Clarify upfront:

- Who is your named point of contact?

- How are employee issues escalated?

- What's the response time guarantee for urgent matters (mid-enrollment errors, COBRA deadline issues)?

Use a PEO Broker to Compare Multiple Providers

For companies evaluating the PEO model, the comparison process itself can be time-consuming. HRO Advisors simplifies this by running side-by-side comparisons across 3–8 PEO providers drawn from a network of 500+, covering pricing, benefits quality, compliance features, and service fit — at no cost and with no obligation to the client.

Their compensation comes from the selected provider, not the business. That structure doesn't add to the client's cost; it's specifically designed to reduce it through direct negotiation. For businesses without weeks to spend evaluating provider contracts, this means reaching a confident decision faster, with more data behind it.

Is Benefits Administration Outsourcing Right for Your Business?

Three Questions That Signal Readiness

Before evaluating providers, answer these honestly:

Is your HR team spending more time on benefits administration than strategic work? If enrollment management, carrier reconciliation, and compliance tracking consume the majority of HR bandwidth, that's a structural problem outsourcing solves directly.

Are you struggling to keep up with changing compliance requirements? ACA indexing changes, COBRA notice deadlines, ERISA disclosure requirements — if your team is reactive rather than proactive on these, the risk exposure is real.

Are your employees limited by the benefits options you can currently offer? If you're losing talent to competitors with richer health plans and retirement options, access to PEO group purchasing changes that equation.

Two or more "yes" answers signal a clear fit. All three, and outsourcing isn't just a convenience — it's a cost and risk management decision worth prioritizing now.

Which Businesses Benefit Most

- 10–500 employee companies without dedicated benefits administration staff

- Fast-growing businesses adding headcount or expanding to new states

- Highly regulated industries: professional services, healthcare, financial services, life sciences, construction

- Companies with lean HR teams managing complex multi-state workforces

Even larger organizations frequently outsource specific functions — COBRA administration and ACA filing are the most commonly outsourced tasks among mid-sized and large employers — without transitioning to a full PEO model.

Key Questions to Ask Any Prospective Provider

Bring these into every vendor conversation:

- Compliance monitoring: How do you track regulatory changes (ACA, COBRA, ERISA), and what's your process when a rule changes mid-year? Who contacts us, and how quickly?

- Data security: What certifications do you hold (SOC 2, HIPAA BAA)? How is employee benefits data stored, transmitted, and protected?

- SLA terms: What accuracy guarantees and response time commitments are written into the contract?

- System integrations: Does your platform integrate with [your specific payroll/HRIS system], and how is data validated during implementation?

- Transition support: What does implementation look like, and what dedicated support is available during the first 90 days?

Frequently Asked Questions

What is administrative outsourcing?

Administrative outsourcing is the practice of contracting a third-party provider to handle specific business functions — such as HR, payroll, or benefits management — that would otherwise be managed in-house. The goal is typically to improve efficiency, reduce costs, and access specialized expertise without building it internally.

Why do companies outsource benefits administration?

Three primary drivers: reducing the administrative burden on internal HR teams, ensuring compliance with complex and frequently changing regulations (ACA, COBRA, ERISA), and accessing better benefits options and cost savings through the provider's group purchasing power.

What does a benefits administrator do?

A benefits administrator handles the operational side of an employer's benefits programs: employee enrollment, eligibility verification, compliance filings, carrier billing reconciliation, and employee communications. This function is filled either by an internal HR team member or a third-party provider.

How much does it cost to outsource benefits administration?

For PEO arrangements, NAPEO's benchmark puts average cost at approximately $1,395 per worksite employee annually, with estimated savings of $1,775 per employee — a net positive for most companies. Standalone TPA pricing varies by service scope. In most cases, reduced staffing costs and better benefits rates more than offset the outsourcing fee.

What is the difference between a PEO and a benefits administrator?

A benefits administrator (or TPA) handles specific administrative tasks while the employer retains employer of record status. A PEO goes further — co-employing workers and bundling benefits administration with payroll, HR compliance, and workers' comp under one arrangement, which also shifts some employer liability to the PEO.

Is outsourcing benefits administration right for small businesses?

Outsourcing is particularly well-suited for small businesses, which often lack the internal HR capacity or negotiating power to manage complex benefits programs. PEOs give small employers access to Fortune 500-level health plans through group purchasing — benefits that would be unaffordable or unavailable when purchased directly.