Many employers assume the mandate went away when the individual penalty was eliminated in 2019. It didn't. The employer shared responsibility provision under IRC Section 4980H remains fully enforced, and the IRS continues to issue penalty notices to non-compliant applicable large employers (ALEs).

This guide covers everything ALEs need to know: how to determine if you qualify, what coverage must be offered, how penalties are calculated, and what annual reporting requires.

Key Takeaways

- Any business averaging 50+ full-time and FTE employees in the prior year is an ALE subject to the mandate

- ALEs must offer affordable, minimum-value coverage to 95%+ of full-time employees and their dependents

- Penalties under 4980H(a) reach $3,340 per employee (minus 30) annually in 2026

- Forms 1094-C and 1095-C must be filed electronically by March 31 each year

- The employer mandate was not repealed and is actively enforced in 2025 and 2026

What Is the ACA Employer Mandate?

The ACA employer mandate—formally called the "employer shared responsibility provision"—requires ALEs to offer affordable minimum essential health coverage with minimum value to at least 95% of their full-time employees and dependents. Fail to do so, and you may owe an Employer Shared Responsibility Payment (ESRP) to the IRS.

The penalty only triggers when at least one full-time employee receives a federal premium tax credit through the Health Insurance Marketplace. That condition offers some protection, but it's too narrow to treat as a reliable buffer against liability.

What the TCJA Did (and Didn't) Change

The Tax Cuts and Jobs Act reduced the individual shared responsibility payment to zero starting in 2019. The employer mandate was untouched. ALEs remain subject to the same rules and the IRS has continued assessing penalties.

ALEs vs. Small Employers

| Category | Employee Count | Subject to Mandate? |

|---|---|---|

| Applicable Large Employer (ALE) | 50+ full-time/FTE | Yes |

| Small employer | Under 50 full-time/FTE | No |

Small employers face no penalty for not offering coverage and are not required to file 1094-C/1095-C forms with the IRS.

Who Must Comply: Determining ALE Status

A business is an ALE for a calendar year if it employed an average of at least 50 full-time employees, including full-time equivalents, during the prior calendar year. This is measured against the prior year's workforce—not your current headcount.

Defining Full-Time Employees Under the ACA

A full-time employee averages 30 or more hours of service per week, or 130 or more hours per calendar month. This definition is specific to ACA purposes and may not align with how your HR team internally classifies employees. Careful hour tracking is essential, since misclassification creates compliance gaps that can trigger IRS penalties.

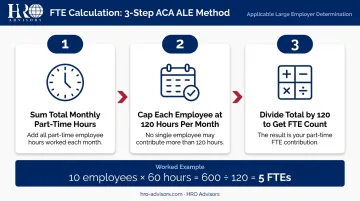

Calculating Full-Time Equivalent (FTE) Employees

Part-time employees don't count as full-time, but their hours still factor into ALE determination through the FTE calculation:

- Add the total monthly hours worked by all part-time employees (under 30 hours/week)

- Count no more than 120 hours per employee per month

- Divide the total by 120

Example: 10 part-time employees each working 60 hours/month = 600 ÷ 120 = 5 FTEs

Add those 5 FTEs to your full-time count when calculating your ALE status.

Special Employee Categories

Some worker types create confusion in ALE calculations:

- Seasonal workers — Generally excluded if the employer exceeds 50 employees for 120 days or fewer and those excess employees are seasonal

- Volunteer emergency workers — Hours excluded for bona fide volunteers at government entities or tax-exempt organizations, including volunteer firefighters

- Educational employees — Teachers count as full-time even when not working year-round; specific rules apply for employment break periods

- Work-study students — Hours performed under federal or state work-study programs are excluded

One additional factor that catches many employers off guard: controlled groups. Companies under common ownership are aggregated for ALE status determination under IRC Section 414, though each legal entity remains separately liable for its own penalties.

ACA Coverage Requirements: What Employers Must Offer

ALEs must offer qualifying coverage to at least 95% of their full-time employees and their dependents. For an employer with 1,000 full-time employees, that means offering coverage to at least 950 of them.

One clarification that catches employers off guard: spouses are not considered dependents under the ACA employer mandate. Dependents are an employee's children who haven't turned 26. Offering spousal coverage is optional under the mandate.

Affordability Standard

Coverage is "affordable" if the employee's required contribution for self-only coverage doesn't exceed a set percentage of their household income. The percentages:

- 2024: 8.39%

- 2025: 9.02%

- 2026: 9.96%

Since employers rarely know employees' actual household incomes, the IRS provides three affordability safe harbors:

| Safe Harbor | How It Works |

|---|---|

| W-2 Wages | Employee contribution ≤ threshold % of Box 1 W-2 wages |

| Rate of Pay | Employee contribution ≤ threshold % of hourly rate × 130 hours (or monthly salary) |

| Federal Poverty Line (FPL) | Employee contribution ≤ threshold % of the prior year's federal poverty guideline ($15,650 for 2025; $15,960 for 2026) |

The FPL safe harbor is the most straightforward to administer—the same dollar amount applies to all employees regardless of compensation.

Minimum Value Standard

Affordability addresses cost; minimum value addresses coverage depth. A plan meets this standard if it pays for at least 60% of the total allowed cost of benefits it covers—this is the plan's actuarial value. Employers can use the HHS Minimum Value Calculator to confirm a plan qualifies before offering it.

Waiting Period Limit

Eligible employees cannot be required to wait more than 90 calendar days before coverage begins. All calendar days count—weekends, holidays, everything. Coverage must start by day 91; there's no grace period beyond that.

ACA Employer Mandate Penalties

Penalties under IRC Section 4980H come in two forms. An employer can only face one type at a time—never both simultaneously. Both are triggered only when at least one full-time employee receives a federal premium tax credit through the Marketplace.

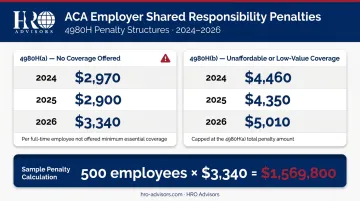

4980H(a): Failure to Offer Coverage

This penalty applies when an ALE fails to offer minimum essential coverage to at least 95% of its full-time employees and dependents.

Annual penalty: Adjusted per-employee rate × (total full-time employees − 30)

Penalty rates:

| Year | Annual Rate per Employee |

|---|---|

| 2024 | $2,970 |

| 2025 | $2,900 |

| 2026 | $3,340 |

Example: An employer with 500 full-time employees who offers no coverage in 2026: 500 − 30 = 470 employees × $3,340 = $1,569,800 annual penalty

4980H(b): Coverage Not Affordable or Lacking Minimum Value

This penalty applies when coverage is offered but is either unaffordable or fails to provide minimum value, causing an employee to receive a Marketplace tax credit.

The penalty is the lesser of:

- The per-employee 4980H(a) rate × (all full-time employees − 30), OR

- A higher per-employee rate × only the employees who actually received a tax credit

4980H(b) rates: $4,460 (2024) | $4,350 (2025) | $5,010 (2026)

The 4980H(b) amount is always capped at what the employer would owe under 4980H(a). Penalties are calculated monthly using one-twelfth of the annual rate.

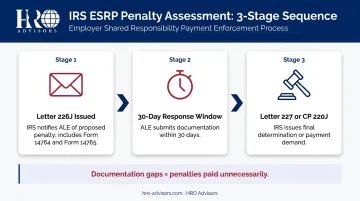

Penalty Assessment and Appeals Process

The IRS follows a defined process:

- Letter 226J — IRS notifies the ALE of a proposed ESRP. Includes Form 14764 (ESRP Response) and Form 14765 (Employee Premium Tax Credit List)

- 30-day response window — The ALE has 30 days from the letter date to respond with documentation

- Letter 227 / Notice CP 220J — After review, the IRS issues Letter 227; if a payment is owed, CP 220J serves as the formal demand

Each step in this process requires supporting documentation — offer records, employee counts, affordability calculations, and 1094/1095-C filings. Employers who receive Letter 226J without that paper trail typically pay penalties they could have disputed.

ACA Reporting Requirements for ALEs

ALEs must file two IRS forms annually:

- Form 1095-C — Provided to each full-time employee and filed with the IRS; captures the coverage offered, employee contribution, and months of coverage

- Form 1094-C — The transmittal/cover form summarizing all 1095-C submissions

Accuracy matters. Errors on these forms are the primary reason employers receive Letter 226J notices—the IRS cross-references 1095-C data against employee tax returns showing Marketplace premium tax credits.

Filing Deadlines (2025 Tax Year)

- Employee copies: March 2, 2026

- Paper filing with IRS: March 2, 2026

- Electronic filing with IRS: March 31, 2026

Employers filing 10 or more information returns in aggregate must file electronically. Verify deadlines annually—they can shift.

State-Level Reporting

Several states have enacted their own ACA-equivalent reporting requirements with separate deadlines:

| State | Forms Required | Key Deadlines |

|---|---|---|

| California | Federal 1094-C/1095-C filed with FTB | Furnish by Jan 31; FTB filing by March 31 |

| New Jersey | NJ-1095 or federal 1095-B/1095-C | Furnish by March 2; transmit by March 31 |

| Massachusetts | Form MA 1099-HC | Issue to individuals by January 31 |

Marketplace Notices and Appeals

When an employee enrolls in a Marketplace plan with advance premium tax credits, the employer receives a notice. This doesn't automatically mean a penalty is owed. If coverage was properly offered, you have 90 days from the notice date to file an appeal.

Document every offer of coverage. The Marketplace appeal process does not determine IRC Section 4980H liability — that remains with the IRS — but a successful appeal can stop an incorrect penalty from moving forward.

How to Stay Compliant With the ACA Employer Mandate

ACA compliance isn't a once-a-year task. It requires ongoing attention throughout the year.

Core ongoing responsibilities for ALEs:

- Track employee hours monthly, especially for variable-hour, part-time, and seasonal workers

- Update affordability calculations each year when IRS thresholds change

- Verify that at least one plan option meets both minimum value and affordability standards

- Maintain documentation of all coverage offers and employee responses

- Assign a compliance owner responsible for annual milestones and deadlines

Businesses with mixed workforces—full-time, part-time, seasonal, and variable-hour employees—face the most complex tracking challenges. Industries like hospitality, retail, and manufacturing deal with this constantly.

That complexity is why many ALEs turn to a Professional Employer Organization (PEO) to handle ACA eligibility tracking, benefits administration, and annual IRS reporting. HRO Advisors helps businesses find the right PEO fit through a free comparison process: gathering your compliance requirements, comparing up to eight providers side-by-side, and negotiating terms on your behalf. Clients typically report HR cost savings of up to 40%, and there's no cost to the business since HRO Advisors is compensated by the selected provider.

ACA requirements change annually. Build a compliance calendar around these key milestones:

- January: Review updated IRS affordability thresholds for the new plan year

- Q3–Q4: Prepare for open enrollment and confirm plan options still meet minimum value standards

- Q1: Complete and file 1094-C and 1095-C forms before the IRS deadline

Frequently Asked Questions

What are the Affordable Care Act employer requirements?

ALEs—businesses with 50 or more full-time and FTE employees—must offer affordable minimum essential coverage with minimum value to at least 95% of full-time employees and their dependents. They must also file Forms 1094-C and 1095-C annually with the IRS and furnish 1095-C copies to employees.

What are the Affordable Care Act employer requirements in 2026?

The core mandate rules remain unchanged for 2026. ALEs must still meet the 9.96% affordability threshold and minimum value standards. Penalty amounts increase to $3,340 under 4980H(a) and $5,010 under 4980H(b) — always verify current figures directly with the IRS.

Is the Affordable Care Act employer mandate still in effect?

Yes. The employer shared responsibility provision was not repealed or modified by the Tax Cuts and Jobs Act. Only the individual mandate penalty was reduced to zero in 2019. The IRS continues to assess and collect ESRP penalties from non-compliant ALEs.

How do I calculate whether my business qualifies as an ALE?

For each month of the prior year, add full-time employees (30+ hours/week) to your FTE count (total part-time hours ÷ 120). Average those 12 monthly totals. If the result is 50 or more, your business is an ALE for the current year.

What are the penalties for not complying with the ACA employer mandate?

The 4980H(a) penalty (no coverage offered) is $2,900 per employee minus 30 in 2025, rising to $3,340 in 2026. The 4980H(b) penalty (unaffordable or low-value coverage) is $4,350 per affected employee in 2025 and $5,010 in 2026, capped at the 4980H(a) amount.

Do employers have to cover part-time employees under the ACA?

No. Part-time employees working under 30 hours per week are not required to be offered coverage under the employer mandate. However, their hours count toward your FTE calculation, which determines whether your business crosses the 50-employee ALE threshold.