Partnering with a Professional Employer Organization (PEO) shifts much of that burden. Through a co-employment arrangement, a PEO can provide or administer workers' comp coverage, handle claims, and implement safety programs that reduce claim frequency over time.

This guide covers everything you need to know: what PEO workers' compensation is, how it works, the three main policy structures, the real benefits and genuine risks, and how to evaluate your options without spending weeks on research.

Key Takeaways

- Under the co-employment model, the PEO assumes workers' comp insurance and claims administration on your behalf.

- PEOs can reduce premiums through pooled group rates, pay-as-you-go billing, and proactive risk management.

- Three policy structures exist—master, multiple coordinated, and client-secured—each affecting your experience modifier differently.

- High-risk industries and businesses with strong existing claims histories should weigh the tradeoffs carefully before committing.

- HRO Advisors compares up to 8 PEO providers for your business at no cost.

What Is PEO Workers' Compensation?

PEO workers' compensation is a coverage arrangement where a Professional Employer Organization provides or administers workers' comp insurance for co-employed workers under a shared-employer model.

The Co-Employment Foundation

A PEO enters a co-employment agreement with your business, becoming the "employer of record" for tax and insurance purposes. You retain full control over daily operations, hiring decisions, and how employees perform their work—but the PEO assumes shared responsibility for payroll, HR administration, benefits, and workers' comp coverage.

This structure is what makes PEO workers' comp possible. Because the PEO is co-employer, it can place your employees under its own insurance policy or coordinate coverage on your behalf.

What Workers' Comp Actually Covers

Workers' compensation is a no-fault insurance system covering:

- Medical costs for work-related injuries or illness

- Lost wages during recovery

- Disability benefits (temporary or permanent)

- Rehabilitation and return-to-work services

- Death benefits for surviving dependents

No-fault means employees receive benefits regardless of who caused the incident—your business or the worker.

Why It's Legally Required

Most U.S. states require coverage once a business employs at least one worker. Thresholds vary by state, and the penalties for non-compliance are substantial:

Most U.S. states require coverage once a business employs at least one worker. Thresholds and penalties vary significantly:

- Florida: Construction employers must cover even a single employee

- Georgia / South Carolina: Coverage required at three to four employees

- Texas / South Dakota: Notable exceptions — coverage isn't mandated for most private employers

- New York: Uninsured employers with more than five employees face Class E felony charges and fines up to $50,000

- Illinois: Knowingly failing to carry coverage is a Class 4 felony with penalties up to $1,000 per day

PEO vs. Standalone Policy

With a standalone policy, your business is the named insured and purchases coverage directly from a commercial carrier. With a PEO arrangement, the structure works differently:

| Standalone Policy | PEO Workers' Comp | |

|---|---|---|

| Policyholder | Your business | The PEO |

| Premium billing | Paid directly to carrier | Bundled into payroll billing |

| Named insured | Your business | PEO (your business listed as additional insured) |

| Underwriting basis | Your company's claims history | PEO's pooled risk group |

How PEOs Handle Workers' Compensation Coverage

The Insurance Mechanics

The PEO either holds a master policy covering all co-employed workers across its client base, or coordinates individual policies per client. Either way, premiums are billed as part of the PEO's regular payroll invoice rather than as a separate annual payment.

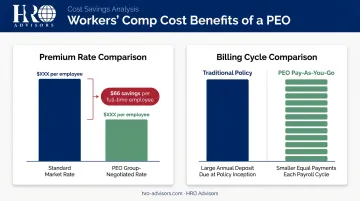

This bundling matters for cash flow. Traditional standalone policies often require upfront deposits of 25% to 100% of the total annual premium. Pay-as-you-go billing through a PEO adjusts premiums each payroll cycle based on actual wages—no large deposit, no year-end audit surprises.

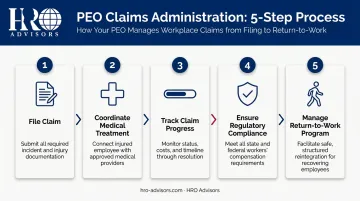

Claims Administration

When an injury occurs under a PEO arrangement, the PEO's internal claims team manages the entire process:

- Files the claim with the insurer immediately after the incident

- Coordinates medical treatment and directs employees to approved providers

- Tracks claim progress and communicates with all parties

- Ensures regulatory compliance with state reporting requirements

- Manages return-to-work programs to reduce lost-time costs

That end-to-end ownership means business owners stay focused on operations—not paperwork—while the PEO keeps claims from dragging on or escalating in cost.

Risk Management Services

Beyond claims handling, most PEOs provide proactive services that lower claim frequency over time:

- Workplace safety audits and hazard identification

- OSHA compliance support and documentation

- Employee injury prevention training

- Return-to-work program development

- Claims fraud detection

Fewer claims means a better loss history, which keeps premiums lower over the long run. For industries like manufacturing and construction, where claim frequency is higher, these services can meaningfully reduce both incident rates and the insurance costs that follow.

Types of Workers' Comp Policies Offered Through PEOs

The policy structure your PEO uses has significant implications for premium calculation and—critically—what happens to your experience modification factor (mod) when you eventually leave. There are three main structures.

Master Policy

The PEO holds a single policy in its own name covering all co-employed workers across every client. Your business is added as an additional insured and benefits from pooled group rates negotiated across thousands of employees.

The catch: your payroll and loss data is pooled with other clients, which dissolves the one-to-one link between a policy and your specific claims history. NCCI notes this creates data reporting challenges that can affect how your mod is calculated if you leave the PEO.

Best for: Small businesses with limited or no prior claims history who want access to the lowest available group rates.

Multiple Coordinated Policy (MCP)

The PEO holds its own policy for its direct workers, and your company also has a separate policy issued under your own tax ID. The insurer coordinates coverage across both.

Your business retains its individual experience modifier under this structure. Claims history stays tied to your company — not the PEO's pool — which matters when you eventually buy coverage independently.

Best for: Businesses that want PEO support but also want to build or protect their own mod history for the future.

Client-Secured Coverage

Your business purchases and holds its own workers' comp policy independently. The PEO assists with administration and claims handling but does not provide the insurance.

This works well for businesses with established carrier relationships, specialized coverage needs, or operations in high-risk industries that require customized policy terms.

| Policy Type | Who Holds the Policy | Experience Mod | Best For |

|---|---|---|---|

| Master Policy | PEO | Pooled with other clients | Small businesses, clean claims history |

| MCP | Both PEO and client | Client retains own mod | Businesses protecting long-term mod history |

| Client-Secured | Client | Client owns fully | High-risk industries, established carriers |

Benefits of PEO Workers' Compensation for Small Businesses

Cost Savings Through Pooled Rates

PEOs aggregate thousands of employees across their entire client base—NAPEO reports PEOs collectively employ 4.5 million worksite workers—giving them purchasing power no individual small business can match. The result is group-negotiated premium rates well below standard market pricing.

NAPEO's ROI analysis identified $66 in workers' comp savings per full-time equivalent employee for PEO clients. Across a 50-person business, that's $3,300 annually from workers' comp alone, before accounting for broader HR cost reductions.

Pay-as-you-go billing adds another layer of financial benefit. Instead of a large annual deposit at policy inception, premiums adjust each payroll cycle based on actual wages—improving cash flow and eliminating the risk of a large audit bill at year-end.

Simplified Multi-State Compliance

Workers' comp requirements aren't uniform across states. Each state sets its own rules on coverage thresholds, job classification codes, audit procedures, and reporting requirements. California, New York, and Texas operate under entirely different rating bureaus—and eleven states maintain independent bureaus separate from NCCI altogether.

For businesses operating across multiple states, PEOs handle:

- Tracking regulatory differences across every active jurisdiction

- Correctly classifying employees by state-specific job codes

- Managing state-specific premium audits

- Providing proof-of-coverage documentation on demand

Reduced Administrative Burden

One-third of companies surveyed by the U.S. Chamber of Commerce spend at least 11 hours per week on HR administration. Workers' comp management—policy renewals, premium audits, claims filing, and compliance reporting—adds to that total.

Under a PEO arrangement, all of that transfers to the PEO's team. Business owners reclaim those hours for client work, hiring decisions, and revenue-generating activity instead of paperwork.

Risks and Limitations of PEO Workers' Comp

Experience Modifier Complications

Under a master policy, your payroll and loss data is commingled with other clients. When you leave the PEO, the rating organization removes your experience from the PEO's aggregate mod and recalculates a separate mod for your business — a process that depends on accurate data reporting throughout your time under the master policy.

The practical risk: if your data wasn't cleanly segregated, rebuilding an independent mod history takes time. NCCI's experience period draws on three years of payroll and loss data, which means newly independent businesses may face a gap period with limited mod history, potentially pushing them toward the assigned risk (higher-rate) market.

The Multiple Coordinated Policy structure avoids this problem entirely, since your company's mod is maintained independently throughout the PEO relationship.

Limited Carrier Flexibility and Service Fees

With a master policy arrangement, you accept the PEO's selected carrier and coverage terms — no independent market shopping, no negotiating specialized endorsements. If the PEO's carrier doesn't fit your industry well, your options are limited.

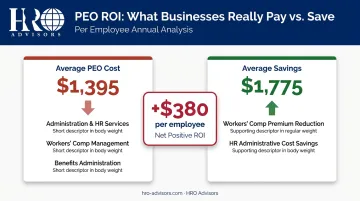

PEO service fees add another layer of cost to evaluate. The U.S. Chamber reports typical PEO pricing ranges from 2% to 12% of total payroll, or $40 to $150 per employee per month. Those fees must be weighed against premium savings to determine whether the arrangement produces a genuine net benefit.

NAPEO's analysis estimates average PEO cost at $1,395 per employee against average savings of $1,775—a positive ROI for most clients. But your specific result depends on your industry, payroll size, and current premium structure.

Industry and Size Suitability

PEO workers' comp isn't the right fit for every business:

- High-risk industries (roofing, tree care, certain construction trades) may face higher rates within PEO pools, or some PEOs may decline to cover them entirely

- Very small businesses with minimal payroll may not generate enough premium savings to offset service fees

- Businesses with strong existing mod histories (well below 1.0) may already be obtaining near-optimal rates independently and have little room for a PEO to improve on

If your business falls into one of these categories, client-secured coverage or a standalone policy may be more cost-effective.

How to Choose the Right PEO for Workers' Compensation

Not all PEOs approach workers' comp the same way. Rates, policy structures, claims service quality, and fee models vary significantly across providers. The questions below give you a solid starting framework before committing to any one option.

Key Questions to Ask Every PEO

- What policy type do you offer—master, MCP, or client-secured?

- Will I retain my own experience modifier throughout and after our relationship?

- Who handles claims—your internal team or a third-party administrator?

- What safety and return-to-work programs are included in the service?

- Can you provide a complete fee breakdown, including all per-employee charges?

- Are you ESAC-accredited or an IRS-certified PEO (CPEO)?

ESAC accreditation confirms a PEO's financial stability and regulatory compliance, and ESAC independently verifies that workers' comp insurance payments are being made on time. Approximately 73% of PEO industry wages are processed through ESAC-accredited organizations.

Evaluating Exit Terms

Any strong PEO partner should give you a clear picture of what happens when you leave: how your claims history is reported, how your experience modifier transfers, and what happens to open claims. Ambiguity on exit terms is a red flag.

The Case for Comparing Multiple Providers

Accepting the first PEO quote you receive is a costly mistake many businesses make. Given how much rates and service quality differ across providers, a side-by-side comparison often produces meaningfully better outcomes.

HRO Advisors compares 3 to 8 PEO providers simultaneously at no cost to your business. The process starts with a free consultation to collect your current HR costs, compliance requirements, and workforce profile. From there, a full analysis runs across more than 500 PEO providers, resulting in a side-by-side breakdown of the options best suited to your situation. The selected provider compensates HRO Advisors directly — with no cost markup to you.

For businesses in high-risk industries like construction or manufacturing, HRO Advisors specifically matches clients with PEOs that have safety infrastructure and workers' comp expertise for those environments. You can reach the team at 866-755-0288 or info@hro-advisors.com.

Frequently Asked Questions

What does PEO stand for in workers' compensation?

PEO stands for Professional Employer Organization. In a workers' comp context, it refers to a co-employment arrangement where the PEO provides or administers workers' compensation coverage on behalf of the client business, bundled with payroll and HR services.

Does a PEO handle workers' compensation?

Yes. Most PEOs either provide workers' comp directly under their own policy or coordinate coverage and manage the full claims administration process. This is typically included as part of a full HR and payroll service package.

Is a PEO the same as a PPO?

No—these are completely different things. A PEO (Professional Employer Organization) is an HR and employment services company. A PPO (Preferred Provider Organization) is a type of health insurance network.

Can I keep my own workers' comp policy when using a PEO?

Yes, under a client-secured coverage arrangement. Some PEOs allow your business to maintain its own policy while they handle administration and claims support. This option varies by provider and typically doesn't include the same group-rate benefits as a master policy.

What happens to my experience modifier when I leave a PEO?

The rating organization separates your payroll and loss data from the PEO's aggregate mod to calculate a standalone modifier. If your history wasn't cleanly tracked, rebuilding that mod takes time and can temporarily push your rates higher.

Is PEO workers' comp cheaper than a standalone policy?

It depends on your business size, industry, and claims history. PEOs offer real savings through pooled buying power, but service fees must be factored in. Businesses with favorable existing mods may not always come out ahead—running a side-by-side comparison before committing is the only way to know for sure.